Does TPI have the seeds of success?

- {{x.value}}

{{ twilioFailed ? 'SMS Code Failed to Send…' : 'Enter verification code' }}

{{ completedStep1 ? 'Authentication & Security' : content.trialHeading.replace('{0}', user.FirstName) }}

{{ content.upgradeHeading.replace('{0}', user.FirstName) }}

The email address you entered is registered with InvestSMART

Please login to continue

We have sent you an email with the details of your registration.

Looks you are already a member. Please enter your password to proceed

{{ upgradeCTAText }}

Updating information

Please wait ...

Your membership to InvestSMART Group recently failed to renew.

Please make sure your payment details are up to date to continue your membership.

Having trouble renewing?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

You've recently updated your payment details.

It may take a few minutes to update your subscription details, during this time you will not be able to view locked content.

If you are still having trouble viewing content after 10 minutes, try logging out of your account and logging back in.

Still having trouble viewing content?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

Please click on the ACTIVATE button to activate your Intelligent Investor 15-day free trial

Please click on the ACTIVATE button to finalise your membership

Unsuccessful registration

Registration for this event is available only to Eureka Report members. View our membership page for more information.

Registration for this event is available only to Intelligent Investor members. View our membership page for more information.

- You are already registered for this event.

- This event is already full.

- Please select a quantity for at least one ticket.

- {{ i }}

Forgotten password

Please enter your email address below to request a new password

- Indepth analysis of ASX listed shares

- BUY, Hold and Sell Recommendations

- Ideas Lab

- Special Reports

- Alan Kohler’s Weekend Briefing

- Interviews with CEO’s & top influencers

- Money Cafe and Talking Finance

- Super Advice and Q&A with Ask Alan

In medieval China, opium was a big deal. Its cultivation and trade was a major economic activity – and a risky one, resulting in not one, but two 'Opium Wars'.

The narcotic is highly addictive and, by the early 20th century, a quarter of the male population in China are thought to have been regular users of the drug. As awareness has grown of the damage caused by the drug's misuse, however, it has become increasingly regulated.

Today, the opium industry plays only a minor role in global trade, but a no less vital one. The opium poppy (Papaver somniferum) produces around 80 different drugs and medications, most of which are used as pain relievers, including morphine and codeine.

Key Points

-

Diversifying suppliers of poppy straw

-

Lowest-cost processing facility

-

Cash flow and supply-demand risks

The legal narcotics industry has been quietly snowballing, with global consumption of opiates increasing by a few percent a year over the past decade. An ageing population and rising incomes in developing countries should ensure demand for pain relievers continues to grow.

No ordinary crop

When considering agricultural companies, it's important to separate the goats from the sheep. Historically, we've avoided the sector altogether but here we want to introduce you to a company that may be worth a closer look: TPI Enterprises.

TPI is one of only eight licensed processors worldwide of narcotic raw material (NRM) – morphine, codeine and other base ingredients that are refined by pharmaceutical companies into drugs such as Panadeine.

Two competitors – Sun Pharma and Tasmanian Alkaloids – also have operations in Australia and, together with TPI, account for just under half of the world's NRM supply. The other major producers are state-owned enterprises in India and Turkey.

Like most agricultural goods, the trouble with NRM is that it's a ‘commodity product' – it's basically all the same, so customers focus on price. Alhough supply contracts typically span 3–5 years, there just isn't much brand loyalty when it comes to NRM, which makes it difficult for TPI to charge more than the competition.

If you're stuck selling a commodity product, the way to make a decent return is to be the lowest-cost operator. This isn't lost on TPI's management which, over the past few years, has invested heavily in its processing plants and supply chain to increase efficiency.

Diversifying suppliers

Before 2014, the Australian opium poppy industry was restricted to Tasmania and there were significant regulatory barriers to new farmers entering the market. That meant that the NRM producers had to give in to farmers' demands and pay top-dollar to secure their crop. The farmers had the upper hand and the profitability of NRM processors was abysmal.

TPI's management had had enough. It petitioned other state governments to allow the growth of opium poppies and was mostly successful, with several states now supporting the industry. In 2017, TPI expects to source poppy straw – from which NRM is extracted – from New South Wales, Victoria, South Australia, Northern Territory and Tasmania.

What's more, in 2016 management fought for – and won – a licence to import poppy straw from Hungary, Turkey and Portugal. TPI now has plans to process 1,000 tonnes of imported straw, which may yield around 20 tonnes of NRM (20% or so of production capacity, as we'll see in a moment).

We think management's plan to diversify its suppliers is an excellent move. For one thing, it breaks the grip that Tasmanian growers had on the industry. With more farmers to choose from, TPI has a stronger position when negotiating prices for poppy straw.

Having multiple growing regions also means production is less likely to be interrupted by bad weather, while staggered harvesting and delivery times evens out the company's capital expenditure across the year. Nonetheless, weather is always a risk for agricultural producers, so shareholders should be prepared for lumpy profits.

Low-cost producer

The second pillar of management's strategy to be the lowest-cost producer is manufacturing efficiency.

TPI has developed a proprietary water-based process to extract the active ingredients from poppy straw, while the rest of the industry still uses traditional solvent-based techniques. TPI's technology has several advantages.

TPI has developed a proprietary water-based process to extract the active ingredients from poppy straw, while the rest of the industry still uses traditional solvent-based techniques. TPI's technology has several advantages.

For one thing, it's more environmentally friendly and doesn't require waste treatment facilities, or the capture of solvent emissions before they reach the atmosphere, because it is largely a closed system using recycled water.

Then, in 2016, the company moved its operations from Tasmania to Melbourne to reduce costs and improve access to mainland farmers. This caused a temporary disruption to manufacturing, but the new facility requires fewer staff to operate, reducing labour costs to just a third that of competing facilities of a similar scale. Throw in the absence of costly solvents and waste treatment, and the new plant has the lowest operating expenses in the industry.

What's more, the cost to build the new 100-tonne facility was only around $20m, compared to $100m or more were it a traditional solvent-based plant.

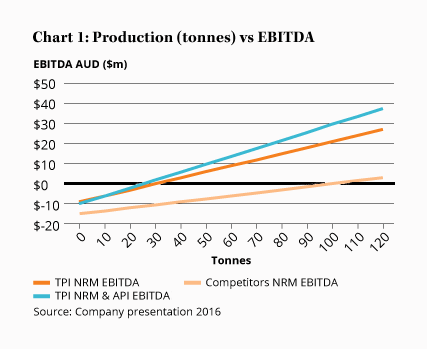

All this means that the new plant needs to process only 30 tonnes or so of NRM to break even, whereas TPI's competitors need to make 100 tonnes before they turn a profit (see Chart 1). The breakeven point is even less if TPI further refines its NRM into active pharmaceutical ingredients (API), such as codeine phosphate.

With lower operating costs, TPI can offer better pricing to customers and, indeed, the company signed two large supply contracts late last year including a $30m deal to provide a large pharmaceutical company with NRM for five years.

More interesting, perhaps, is Monday's announcement that TPI has agreed to process up to 2,000 tonnes of poppy straw for one of its largest competitors. Management said this is a milestone as it shows NRM processing can be outsourced to TPI at a lower cost than a rival's in-house processing. Given the significant fixed costs of NRM production, the more poppy straw TPI can process, the better.

Management said the 2,000 tonnes of outsourced processing – in addition to the Australian harvest and imported material – provides TPI with enough poppy straw to produce roughly 100 tonnes of NRM in 2017 if there is sufficient demand, which would give the company an 8% market share.

Still no cash flow

Unfortunately, it's that ‘if there is sufficient demand' clause that makes the future hazy. The latest estimate by the International Narcotics Control Board (a key regulator) is that production of NRM will exceed demand in 2017 by almost 40%, so we doubt TPI will get anywhere near that level of production.

Management's goal – which is not the same as official guidance – is to produce at least 55 tonnes of NRM in 2017, 100 tonnes by 2019 and 200 tonnes by 2021.

In the meantime, costs are still piling up for the Melbourne plant as it ramps up production and the company doesn't expect to have more cash coming in than going out until 2019. TPI made a loss after tax of $14m for the year to December and had net debt of $26m, including a $20m loan from major shareholder Washington H. Soul Pattinson.

With its debt facilities maxed out, TPI was forced to raise $44m last month to fund its working capital needs and operating expenses. It also intends to repay a large chunk of the Soul Patts debt, which needs renewing in March 2018. The cash injection from shareholders puts the balance sheet in order, but it's a reminder that the company isn't out of the woods.

Bottom line

TPI is the lowest-cost manufacturer in an intensely regulated oligopoly and we expect it to be profitable in the next couple of years as its main production facility ramps up capacity. The move to mainland Australia and recently awarded import licence diversify away many of the most pressing risks – including poor weather and a lack of affordable poppy straw – but there are other concerns to consider, including the weak cash flow, regulatory risks, and a supply-demand imbalance for NRM in 2017.

If TPI does achieve its goal for 100 tonnes of NRM by 2019, it would imply earnings before interest, tax, depreciation and amortisation (EBITDA) of around $20m, compared to negative $8m in 2016. However, with an enterprise value around eight times 2019 EBITDA, TPI doesn't strike us as being particularly undervalued given the risks.

We'll keep an eye on the stock as it could make for an interesting future opportunity, but for now we'll be watching from the sidelines.