Why are market economists so bullish?

The Reserve Bank of Australia has maintained its neutral stance on policy but there remains considerable uncertainty surrounding the economic outlook. The property sector remains strong but beyond that there are a number of cracks that could prove difficult to fill.

The RBA monthly board minutes are often a mixed bag. They occasionally provide additional insight into the central bank's thinking but more often than not they simply communicate a dated view of the economy.

The minutes this month were mostly of the latter variety. There has been a notable shift in market sentiment since the RBA met on October 7 and markets are pricing in an 38 per cent chance that the RBA will cut rates by June next year (at the same time 26 of the 27 economists surveyed by Bloomberg believe that the next rate move is up).

It is not uncommon for the market and market economists to be in disagreement. I can remember times while working at the RBA when sentiment from both sources was completely at odds with internal discussions.

But it does warrant some further discussion. Why are market economists so bullish?

The main reason for believing that rates should rise -- either now or next year -- is that the housing market continues to be quite strong. Conventional thinking is that rates need to rise to either ease pressure in the property market or ensure that the market doesn't become overheated.

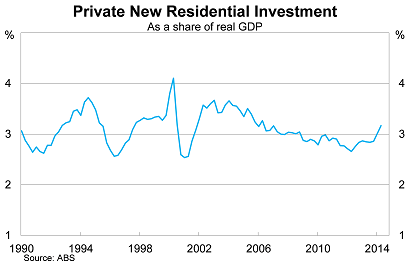

At the same time, booming prices -- combined with low interest rates -- continue to support residential investment. For some economists, this is sufficient to believe that the Australian economy is rebalancing and well-placed to absorb the collapse in mining investment.

This is faulty thinking for two reasons. First, the RBA has already indicated that they are prepared to reduce pressure in the property market via macroprudential policies (Another RBA warning on housing, October 10); and second, residential investment accounted for just 3.2 per cent of real GDP in the June quarter.

The first reason makes it clear that the RBA will not allow monetary policy to be held hostage by the property market. The second suggests that analysts should avoid concentrating too much on just the housing sector.

The property sector is incredibly important to bank and household balance sheets, but from the perspective of monetary policy it is just one piece of a broader puzzle. Rates may rise in 2015 but housing will be only one factor. Exports, household spending and business investment are set to play a much larger role in whether the RBA cut or hike rates next year or the year after.

A closer look at those other factors reveals that a rate rise next year remains highly unlikely.

Consider household spending for example. Retail trade growth has eased considerably since the beginning of the year and increasingly reflects population growth rather than higher wages. With immigration showing signs of moderating and real wages declining, household spending is set to come under considerable pressure over the next year.

What about exports? Net exports declined in the June quarter but are widely expected to bounce back over the remainder of the year. Export volumes are expected to be strong but owing to a much lower terms of trade, the income we receive from those exports isn't going as far as it once did.

Furthermore, the Chinese economy continues to moderate and infrastructure investment has clearly begun a period of consolidation. This will weigh on the demand for Australian iron ore and coal exports.

Finally, there remains considerable uncertainty surrounding the collapse in mining investment. The RBA noted in its August Statement on Monetary Policy that “there is no guarantee that the rebalancing of spending will be a smooth process”, and that it may prove highly disruptive to the Australian economy, resulting in either “excess demand for, or supply of, particular labour skills or types of capital”.

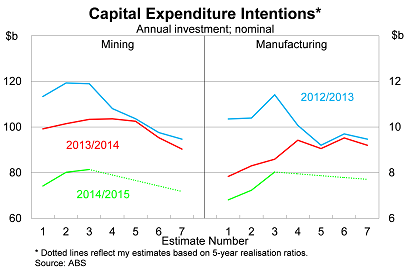

Non-mining investment intentions have improved somewhat and are likely to rise over the 2014-15 financial year. But that won't be sufficient to offset the decline in mining investment, which is set to decline by around 20 per cent in nominal terms (A weakening investment outlook for businesses, August 28).

In the presence of such uncertainty, readers should be apprehensive about cash rate expectations from both financial markets and market economists. Rarely has forecasting interest rates been more difficult. A slight change in assumption for mining investment or commodity prices may lead to a very different path for the cash rate over the next few years.

During such uncertain times, it is important to focus on the most important factors driving the Australian economy. The property sector simply isn't one of those factors, but household spending and the mining sector certainly is.