The Week in Review: February 16, 2018

Share markets settled down as another mixed bag of Australian economic data dropped.

Investment markets and key developments over the past week

- Share markets rebounded over the last week as share investors became a bit more relaxed about the prospect of higher inflation and interest rates and the unwinding of short volatility trades ran its course. However, the rebound has been concentrated in the US share market (which is up 7 per cent from its recent low) with Europe, Japan and Australia lagging. The Australian share market never fell as much on the way down but a resumption of the falling US dollar is likely playing a role in the relative outperformance of US shares as it boosts US profits and constrains profits in Europe, Japan, Australia, etc. Bond yields continued to rise over the last week, except in Japan, and commodity prices and the Australian dollar rose helped by renewed US dollar weakness and as investor confidence returned.

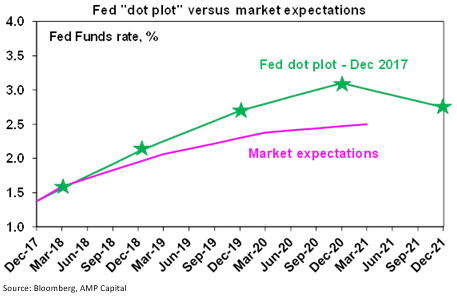

- While share markets have settled down to varying degrees, the strength of the US economy with fiscal policy providing an additional boost is likely to ensure that inflation will be a growing issue this year globally and we remain of view that market expectations regarding Fed rate hikes are too complacent. The next chart shows that US money market rate hike expectations are still well below what the Fed has signalled and so a further shifting up in market interest rate expectations is likely and this will drive a further rise in bond yields.

- Strong earnings growth and the absence of a recession on the horizon as even US monetary policy is still easy should allow share markets to trend higher this year, but rising US inflation, interest rates and bond yields will make for ongoing bouts of volatility and a more volatile and constrained ride than we became used to last year.

- President Trump's proposed 2019 Budget – with $US200bn in infrastructure funding over ten years (including an asset recycling plan), but a 2 per cent cut to domestic spending - is of little relevance. Congress decides the budget not the president and at present its focussed on the deal just passed to increase spending by $300bn over the next two years. That deal already included some increase in infrastructure spending but only for two years and half what Trump is looking for. So yes, there will increased infrastructure spending in the US in the years ahead but nowhere near as much as Trump has promised. Meanwhile, Senate efforts to find a solution for Dreamers looks to have floundered for now keeping alive the prospect of another Government shutdown next month. We remain of the view that if there is one it will be short given the political damage it could cause the Democrats.

Major global economic events and implications

- Confusing US economic data – but forget stagflation worries. A stronger than expected rise in CPI inflation with January core inflation up 0.3 per cent month on month or 1.8 per cent year on year and running at an annualised 2.6 per cent over the last six months and a rising trend in producer price inflation reinforces our expectations for rising US inflation this year. However, last year also saw a stronger than expected rise in inflation in January which then slowed again and some of the components that rose strongly look a bit noisy so it would be premature to get even more bearish on inflation. More importantly, the surprise fall in January retail sales looks likely to be an aberration that may owe to poor weather with strong consumer confidence, strong jobs growth, tax cuts and rising wages growth all likely to support strong retail sales going forward. Meanwhile other activity related indicators were strong. Industrial production slipped in January but small business optimism, regional manufacturing surveys and home builder conditions are all strong and their components point to strong orders and employment and rising inflationary pressures.

- Consistent with ongoing strength in the US economy, the December quarter US earnings reporting season continues to impress. Of the 388 S&P 500 companies to have reported so far 80 per cent have beaten earnings expectations and 78 per cent have beaten on sales. Earnings growth for the quarter is tracking up 15 per cent year on year and revenue is up 8 per cent yoy.

- Japanese December quarter GDP growth of just 0.1 per cent quarter on quarter was less than expected but consumer spending was solid and leading indicators point to continued growth ahead. Bank of Japan Governor Kuroda's nomination for another term along with comments by PM Abe and his advisers indicate that the BoJ is unlikely to ease up on its monetary policy stimulus any time soon. Particularly with the Yen rising sharply.

Australian economic events and implications

- As has long been the case in recent years Australian data was mixed. On the one hand business condition and confidence rose in January according to the NAB survey and employment rose solidly. But against this consumer confidence slipped a bit in February and the quality of the jobs report was poor with a sharp fall in full time jobs and slowing hours worked. On the jobs front, job vacancies and job ads point to continued strength but employment has overshot the strength in jobs leading indicators and so may undershoot for a while and more significantly after a good rebound in full time jobs last year we may be reverting back to lower quality part time jobs as the main driver of employment.

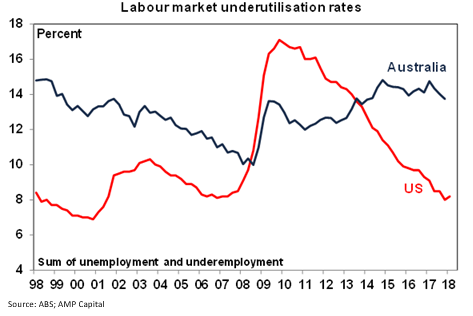

- For those trying to understand why the RBA is lagging behind the Fed in raising rates (apart from the fact that the Fed cut far more than the RBA did in the first place), the chart below is a good place to start. Basically, labour market underutilisation (or unemployment plus underemployment) is far higher in Australia than in the US. This means it will take longer for wages growth to pick up in Australia and for the RBA to hike rates.

- On the interest rate front, RBA Governor Lowe's Parliamentary testimony basically repeated the Bank's message of the last few weeks which is that the next move on rates will most likely be up, the economy is moving in the right direction, we have seen more positive economic news in recent months, but uncertainty remains around the consumer and progress in reducing unemployment and having inflation return to target is likely to be gradual. As such the RBA “does not see a strong case for a near-term adjustment of monetary policy”. We agree and don't see a rate hike until late this year at the earliest.

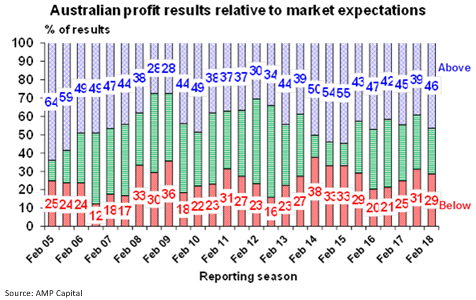

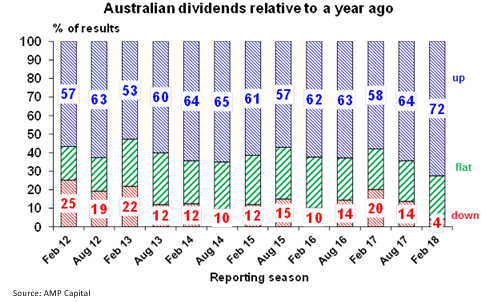

- It's still early days in the December half profit reporting season with only a third of companies having reported, but so far it remains reasonably good. 46 per cent of results have exceeded expectations against a norm of 44 per cent, 74 per cent have seen profits rise from a year ago and 72 per cent have increased dividends from a year ago. However, only about 49 per cent have seen their share price outperform on results day and there is still a way to go yet with results often tailing off a bit as more report.

Dr Shane Oliver is the Chief Economist at AMP Capital.

Share this article and show your support