The squeeze on first home buyers continues

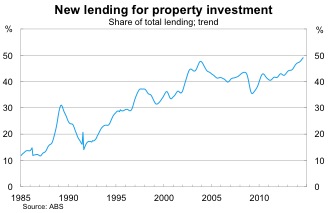

Speculative activity continues to dominate Australia's residential property sector and now accounts for roughly half of new mortgage activity. Given these results, the Reserve Bank of Australia (RBA) is right to be concerned about the increase of imbalances within the sector (Another RBA warning on housing, October 10)

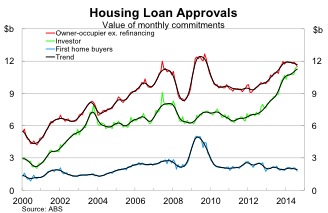

The value of loan approvals to owner-occupiers, excluding refinancing, fell by 2.3 per cent in August – missing expectations – to be 6 per cent higher over the year. The fall was driven by a combination of softer volumes and a decline in the average loan size.

Refinancing of existing home loans remains popular, with the number of applications rising in August. But the total value of refinancing activity eased, reflecting a sharp fall in the average loan size. Refinancing activity should remain elevated in the short-term, supported by historically low mortgage rates and high existing debt burdens.

Lending activity among owner-occupiers has clearly peaked and on a trend basis has declined for six consecutive months. The same cannot be said for investor activity; the pace of growth might have moderated a little but the upward trend remains strong.

On a seasonally-adjusted basis, investor activity was largely unchanged in August but is up 27.6 per cent over the year. According to the less volatile trend estimates, it won't be long before investor activity accounts for more than half of new mortgage lending.

So why is this dynamic taking place? One reason is that Australia's tax system favours speculative activity and when rates are low investors have a tendency to go a little crazy. That certainly accounts for the long-term upward trend in investor activity.

Another reason is that the supply of owner-occupiers looking to either downsize, upsize or shift neighbourhoods is more easily exhausted that investor demand – particularly when rates are low.

Remember that owner-occupiers can be separated into two distinct groups: existing home owners and potential home buyers. The first group is renewed periodically when potential buyers become first home buyers (FHB). Obviously the pool of existing home owners can also decline over time as some home owners pass away or move into aged care facilities.

No such distinction exists for investor demand. Investors can purchase as many properties as they want and the only limit is determined by market sentiment and capacity to pay. Investor demand – as with owner-occupier demand – can become exhausted but it is not as easy to predict.

Right now demand from FHBs remains weak. The value of loan approvals to FHBs fell by 12 per cent in August and is almost 9 per cent lower over the year. FHB activity, as a share of total owner-occupier lending, is now at its lowest level in at least in 23 years.

At this stage I should point out that the ABS is investigating the quality and collection of FHB data. Banks are supposed to report monthly on the total number of homes purchased by first home buyers; strictly speaking it should not be tied to whether a home owner takes advantage of the first home owner grant. There are concerns that some lenders are finding it difficult to identify first home buyers.

As it stand though it would be surprising if the investigation revealed that FHB activity was actually strong, particularly given the anecdotal evidence and other economic indicators that point to soft demand among younger households.

At the state level, the fall in activity during August was largely driven by New South Wales and Victoria. The other states reported more moderate results – both up and down – although there was a considerable surge in the Northern Territory. On a trend basis, demand from owner-occupiers has stagnated in every state besides Queensland.

Image: Callam 10 oct arvo 3.jpg

Investor demand continues to boom but it appears as though owner-occupier demand peaked earlier this year. With FHB poorly positioned to leverage up and fill the gap, expect the demand from owner-occupiers to fall rapidly over the next year.

Investor demand is less predictable but if the RBA and the Australian Prudential Regulation Authority introduce measures to curb investor borrowing then demand in that sector will ease as well. As a result, expect house price growth to moderate over the remainder of this year and potentially decline in the first half of 2015.