The pitfalls of mining for income

Summary: Income investors should be attempting to limit risk, focusing on total return. Additionally, the nature of mining and resources companies is that they are capital intense, which flies in the face of the steady cash flows needed to pay steady predictable dividends. |

Key take-out: Yield seekers should be wary of the risk and volatility in commodity prices. |

Key beneficiaries: General investors. Category: Strategy.. |

Resources shares: are they ever a good income investment?

The short answer is no. But let's entertain the thought for a moment as many in the market are talking about the dividend yield of BHP, not to mention WPL and a few others. I'll admit, before I joined the team at Eureka I had recommended WPL in the past as an income play. But this was under a strict set of criteria and a close watchful eye. Even then it was a nervous call, and one that probably pushed it in terms of acceptable risk for most income investors. And therein lies the point.

Income investors should be attempting to limit risk, focusing on total return. Additionally, the nature of mining and resources companies is that they are capital intense, which flies in the face of the steady cash flows needed to pay steady predictable dividends.

I asked George Boubouras of Contango Asset Management, who runs an income-focused LIC, whether he views resources stocks as a wise choice for income investors, and he summed things up quite succinctly, suggesting that: “In short it is not wise and investors need to understand the context. The resource sector is not a traditional sector to expect to receive consistent dividends through a normal cycle.”

So, in our approach to income investing we recognise that companies must balance the thirst for investment with the lure of high dividend payments. Indeed all investors need to understand this tension when choosing stocks to buy - just as we do when we make selections for the Income First model portfolio.

If this balance is not found, the sustainability and optimisation of dividends will fall into question. This balance is incredibly difficult for a mining business, and even more difficult for us as investors to forecast.

While there may be some circumstances in which resources companies may suit a particular income strategy (such as dividend stripping). But investors must remember that the capital needs to be at risk for 45 days, plus the trading days, in order to take advantage of franking credits (the 45 day rule applies differently to some investors, so do seek professional tax advice on this point if needed).

Boubouras adds that when considering resources, “the investor has had to accept much higher volatility. When WPL was trading below $28 their risk tolerance would have been tested. WPL is a good example of the trade-off when seeking dividends from the resource/energy sector - that is you receive a dividend but must accept higher volatility.”

Sure, some resources businesses may have the balance sheet capacity to borrow at low cost and pay dividends through the lower point of the cycle, but I doubt we'd elect a term deposit with this much risk of capital loss (even if the bank offered us 9 per cent). In that light I'd contend that the risk involved in resources companies is by its nature difficult to reconcile with the objectives of an income focused investor.

Dividends cannot fully replace capital losses

But BHP is yielding more than 7 per cent! Yes, but why? Investors need to remember that dividend yield is a function of both price and dividends per share. So a good yield can come about through dividend growth, or a weak share price. If it is the latter, then there is the often insurmountable task of analysing whether the share price fall is warranted, and will continue. Additionally, is the forecast dividend likely to eventuate and what are the risks involved? Unfortunately for BHP, this may mean trying to forecast the iron ore price, something no-one I have encountered has done with success in the last few years.

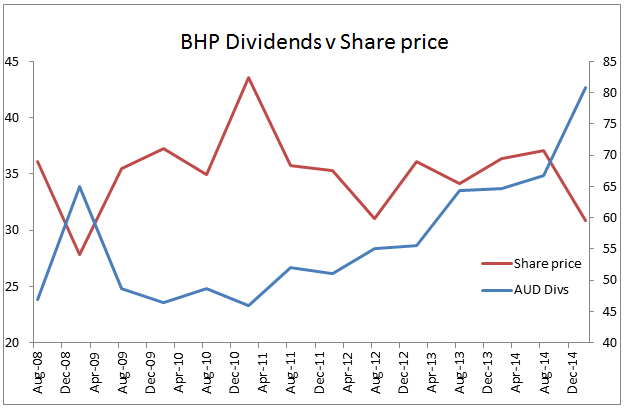

To a degree, there appears to be an inverse correlation between BHP's share price and the dividends paid. The chart below shows that as dividends have risen, the share price seems to have declined and vice versa. There could be a logical explanation for this, related to currency and macroeconomic conclusions. For example if the Australian dollar is lower, BHP's US dollar dividend will be higher when converted. In addition if the Australian dollar is reflective of weaker commodity prices then the BHP share price is likely to be lower. This seems a long straw to me, but I'll let you make your own judgment.

The conclusion that I draw is that income investors appear to be giving up capital for income in the case of BHP over recent years. Perhaps when the market sees BHP paying out cash and cutting investment into the future, the share price falls?

There is simply too much risk and volatility in commodity prices

The highest yielding mining stock on the market is Grange Resources (GRR) at 25 per cent yield when including trailing dividends. The problem is that this yield probably won't continue into the future, and the share price has performed poorly in recent times. Income investors often hold dual objectives of capital protection and steady predictable income generation. Unfortunately, meeting both goals is a tough ask given the nature of commodity price-driven stocks.

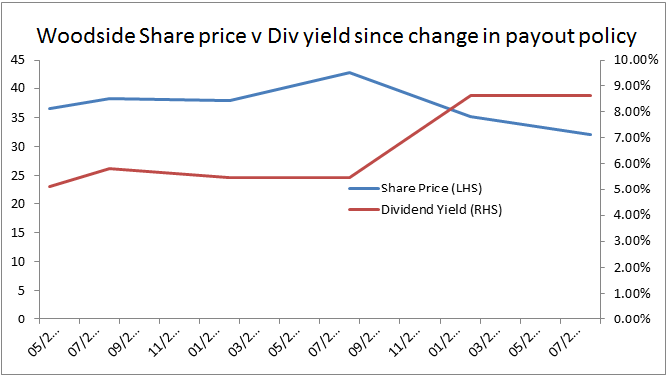

Another great example of this is Woodside Petroleum (WPL). WPL announced in April 2013 that it would pay 80 per cent of underlying net profit out to shareholders as dividends, placing the company on a forecast dividend yield of over 10 per cent. This was mouth-watering to income investors, as the company was generating huge amounts of free cash flow and had recently pulled back from capital investments at Browse. So the yield appeared sustainable. But oil prices were around $US100, and we all know what happened next.

Given that oil prices have fallen from around $US100 towards $US40, WPL has performed well.

Largely this has been a result of a strong balance sheet position in the business. In fact, WPL was net cash until it purchased its stake in Wheatstone from Apache, and is now again on the hunt for an acquisition in its approach for Oil Search.

How is this all relevant? Since announcing its payout ratio policy change, the dividend yield has jumped to around 9 per cent plus franking credits on a trailing basis. On a forecast basis (assuming the final dividend in CY16 is similar to the interim), the yield is more like 6.5 per cent, but that is using a more current share price around $29. More to the point, since this payout lift WPL has paid $A6.64 in dividends, but the share price is down $A8.

Boubouras contends that the current yield from WPL is not the norm, suggesting that WPL: “did unwind a very aggressive capex program of a magnitude never to be seen any time soon. The recent prospect of WPL looking at OSH assets however clearly demonstrates the much higher price volatility for a traditional dividend seeking investor.” So, while yes there has also been a payout of above normal dividends and franking credits, it is clear that the capital risk in this has been eroding the income produced.

Risk and dividend traps

A dividend trap is a stock that pays an extremely high yield but is unable to sustain it in the future. The result of this is usually that the stock price falls by more than the benefit gained from taking the income, or that the dividend is cut in the future. Or more simply, the total return is negative, as with my WPL and BHP examples above. Stock market investors should always be considering the quality and prospects of the businesses in which they are investing. For income investors, dividends might be a prerequisite, but they are only half the picture.

The key point is that income investors are generally looking for different things to most other investors. There is a desire for low risk, recurring income and the strong free cash flow that lends itself to dividend payments. This is why banks, supermarkets, and telecoms companies with defensive and diversified earnings are so attractive. Mining and energy businesses are, by their nature, lumpy. They require significant up-front capital investment, and are capital intensive businesses in ongoing operations, with low predictability in cash flows. I'm not saying that a resources business will never be a good investment when the yield is high, and in fact both WPL and BHP may be worth a look at current prices. However, given the strong dividend yields available on the market in banks, insurers, consumer staples, industrials and myriad of other sectors on the ASX, there is no reason for an income investor to chase extreme yields from mining and energy stocks given the risk to capital preservation.

Income investors in general need to focus on the sustainability of a dividend yield and the balance within the business paying out the cash. At Eureka we are focused on dividend paying stocks that are able to grow those dividends. To focus on this, we look for companies that are producing sufficient cash flow to pay shareholders and invest in the future. Unfortunately these qualities are scarce in the resources sector.