The ECB can't save Europe alone

The European Central Bank is losing its perennial battle against deflation, with annual inflation easing further in September. But the ECB cannot fix this problem on its own: it needs Germany to rise to the challenge and shift their priorities from battling imaginary inflation towards supporting employment and the broader recovery.

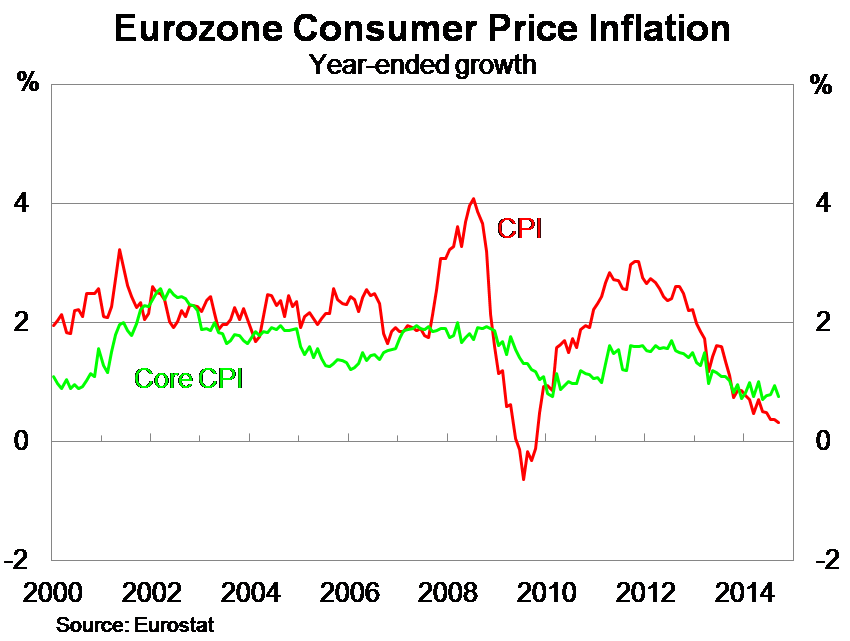

Inflation in the eurozone rose by just 0.3 per cent over the year to September and remains well below the ECB's target for annual inflation of around 2 per cent. The core measure -- which removes volatile items such as food, energy, alcohol and tobacco -- rose by 0.8 over the year to September.

On a headline basis, deflation is an immediate concern but the relative strength of the core measure does offer some modest upside for inflation in the coming months.

As a result, the real interest rate -- that is the interest rate adjusted for annual inflation -- in the eurozone continues to rise. Remarkably, the real interest rate is higher than it is in Australia and much higher than in either the United Kingdom or the United States.

Low inflation is effectively making it more expensive to borrow, while simultaneously reducing the impetus for businesses and households to spend. It's no surprise that the eurozone recovery -- and I use that phrase lightly -- has struggled to gain any traction.

Nevertheless, the ECB has been active in recent months, introducing new and innovative measures to boost lending activity and aggregate demand. It remains too soon to judge these programs but ECB president Mario Draghi is the first to admit that he and the ECB needs some help.

“It would be helpful for the overall stance of policy if fiscal policy could play a greater role alongside monetary policy,” Draghi said in August. “I believe there is scope for this while taking into account our specific initial conditions and legal constraints.”

Without help on the fiscal front -- which at this stage appears unlikely -- the eurozone risks a triple-dip recession. Recent data from Germany suggests that the eurozone's one pillar of strength has already rolled over, with domestic demand insufficient and a hard-headed (and bone-headed) German government preferring to fight imagined inflationary pressures rather than promoting investment and employment.

On balance, the outlook for inflation in the eurozone is mixed. I noted earlier in the article that the core measure of inflation points to some upside risk for inflation. To some extent, the recent weakness reflects declining prices for a range of volatile goods such as food and fuel. Earlier in the week I noted the same phenomenon in the UK (Volatility masks Britain's real inflation, October 15).

That will eventually reverse and push headline inflation higher. But given food and energy are necessities, higher prices will be cold comfort to households and businesses who continue to suffer at the hands of austerity and a dysfunctional financial system.

Domestic sources of inflation should remain subdued and I expect wage growth to slide further due to inadequate domestic demand and the delayed effect of the crisis on wage negotiations. A similar situation has been observed in both the UK and US.

As with those two countries, the eurozone also has a productivity problem.

With the unemployment rate at 11.5 per cent in September there remains insufficient demand for labour throughout the region. Wage pressures and inflation arise when the demand for labour exceeds the available supply of workers. It'll be five years -- potentially much more -- until the unemployment rate declines to a level that causes wages to surge.

It's worth remembering that these data ignore the millions of Europeans who have given up on finding a job after years of unemployment and the millions more who would love to work additional hours. The labour market in the eurozone is far weaker than the statistics suggest.

The exchange rate is one area that may boost inflation as the euro depreciates further on the back of economic weakness and the end of the Federal Reserve's asset purchasing program. But the effect is likely to be modest since a high share of euro trade occurs among euro members.

The eurozone is once again on the precipice of crisis and this time it will be awfully tough for Mario Draghi and the ECB to pull the region back from the brink. There may be some upside risk for inflation in the near-term but a triple-dip recession appears likely and the German economy has become increasingly fragile.

To get the recovery back on track the ECB needs help, particularly from the major governments within the region. It is time that Germany stopped worrying about inflation and recognised that without further stimulus, the eurozone's crisis will persist for years to come.