The average Australian's savings: how do you compare?

Here are Australia's savings rates by age, wealth and income. How do you stack up?

- {{x.value}}

{{ twilioFailed ? 'SMS Code Failed to Send…' : 'Enter verification code' }}

{{ completedStep1 ? 'Authentication & Security' : content.trialHeading.replace('{0}', user.FirstName) }}

{{ content.upgradeHeading.replace('{0}', user.FirstName) }}

The email address you entered is registered with InvestSMART

Please login to continue

We have sent you an email with the details of your registration.

Looks you are already a member. Please enter your password to proceed

{{ upgradeCTAText }}

Updating information

Please wait ...

Your membership to InvestSMART Group recently failed to renew.

Please make sure your payment details are up to date to continue your membership.

Having trouble renewing?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

You've recently updated your payment details.

It may take a few minutes to update your subscription details, during this time you will not be able to view locked content.

If you are still having trouble viewing content after 10 minutes, try logging out of your account and logging back in.

Still having trouble viewing content?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

Please click on the ACTIVATE button to activate your Intelligent Investor 15-day free trial

Please click on the ACTIVATE button to finalise your membership

Unsuccessful registration

Registration for this event is available only to Eureka Report members. View our membership page for more information.

Registration for this event is available only to Intelligent Investor members. View our membership page for more information.

- You are already registered for this event.

- This event is already full.

- Please select a quantity for at least one ticket.

- {{ i }}

Forgotten password

Please enter your email address below to request a new password

- Indepth analysis of ASX listed shares

- BUY, Hold and Sell Recommendations

- Ideas Lab

- Special Reports

- Alan Kohler’s Weekend Briefing

- Interviews with CEO’s & top influencers

- Money Cafe and Talking Finance

- Super Advice and Q&A with Ask Alan

The average Australian is putting $427 under their mattress each month, according to a recent survey by Suncorp (ASX: SUN).

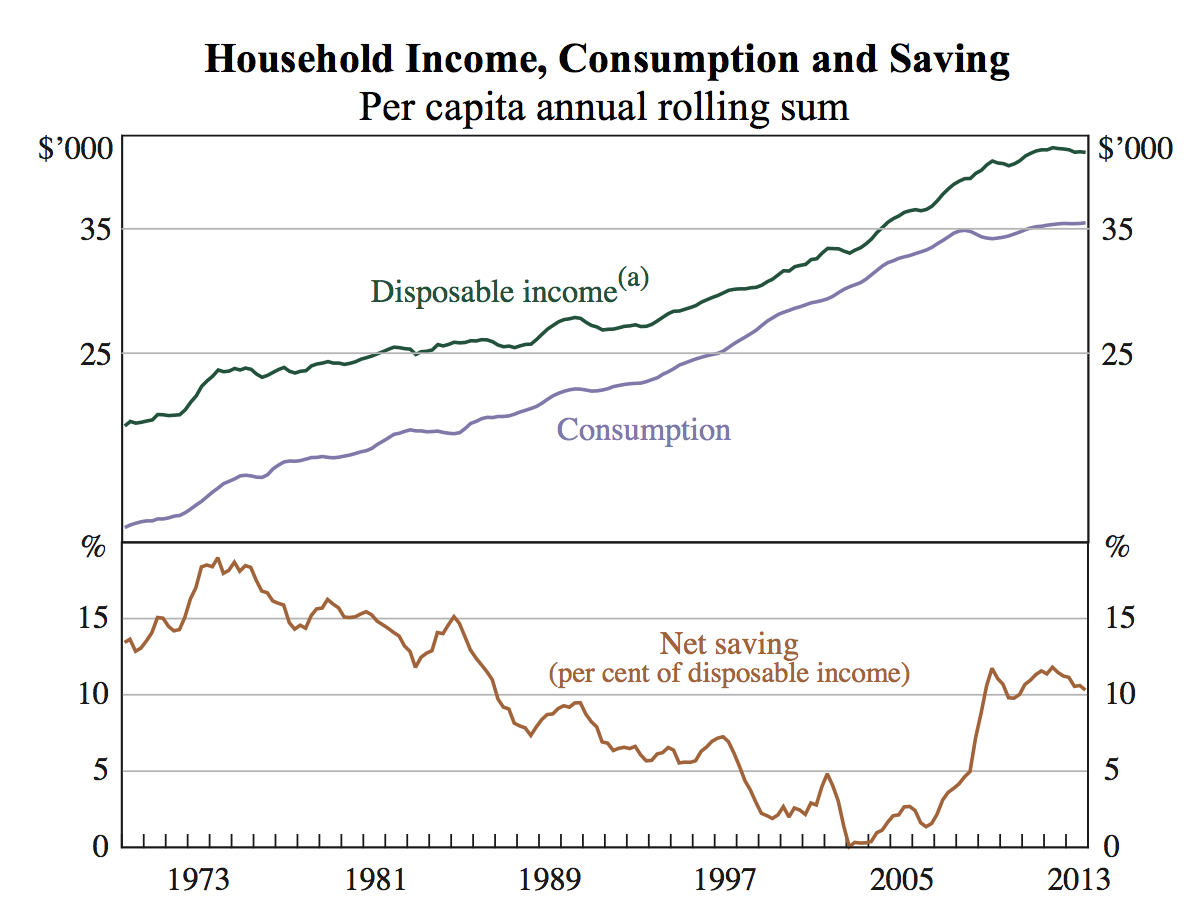

The good news is that Australians are saving more now than at any point since the 1980s.

The good news is that Australians are saving more now than at any point since the 1980s.

Between the 1970s and early 2000s there was a gradual decline in the rate of saving due to falling interest rates, greater availability of credit and stable economic conditions. By 2003, Australians weren't saving enough for a freddo frog.

The financial crisis whacked some sense back into us and there has been a strong resurgence in savings rates since then, with the national average now hovering around 12% of disposable income.

But of course that's only half the story. Savings rates differ widely depending on age, wealth and income.

Age.png)

Refreshingly, Suncorp found that youngsters aged 25 to 34 were above average savers, putting away $533 a month.

A 2014 discussion paper by the Reserve Bank went into more detail, and also found that there was a dip in savings for those aged 35 to 45.

That's understandable due to significantly higher living costs around that time as middle-aged households are often paying off a mortgage and have children to support.

However, as the RBA notes, 'the behaviour is also consistent with a myopic model of household behaviour. For example, Thaler and Shefrin (1981) argue that hyperbolic discounting can explain why younger households tend not to save enough for retirement, while Carroll and Samwick (1997) argue that younger households place more weight on saving for large purchases and emergencies to smooth near-term consumption rather than saving for longer-term (retirement) consumption'.

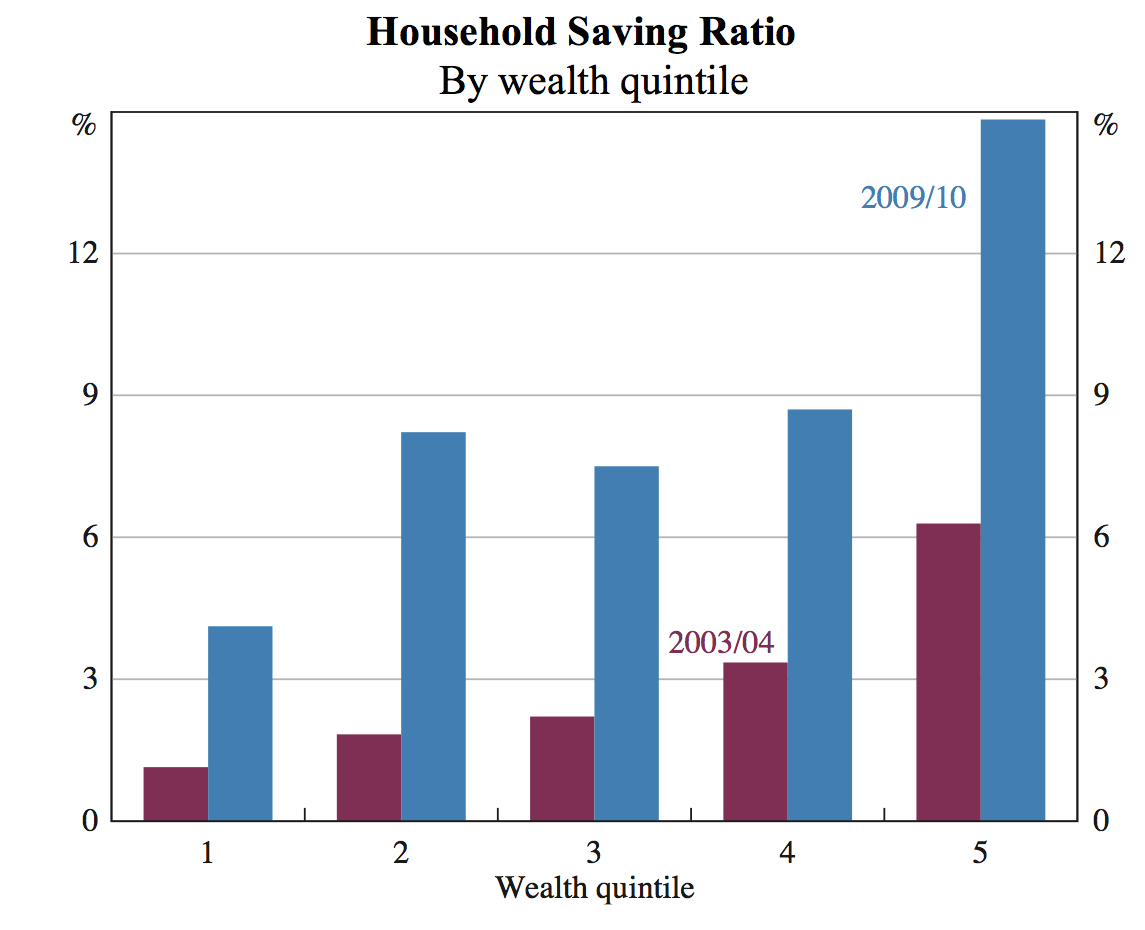

Net worth

It's probably not too surprising to learn that wealth and income significantly affect our ability and propensity to save.

The richest 20% of households save nearly 15% of their disposable income, double the median.

Interestingly though, the effect of owning a home outright depends on age. For the young, it's associated with higher rates of saving and probably has a lot to do with personality, rather than a pure 'wealth effect'.

Older households, on the other hand, show a decreased tendency to save if they own their own home. That's probably down to feeling a greater amount of financial security, which reduces the desire to save for emergencies.

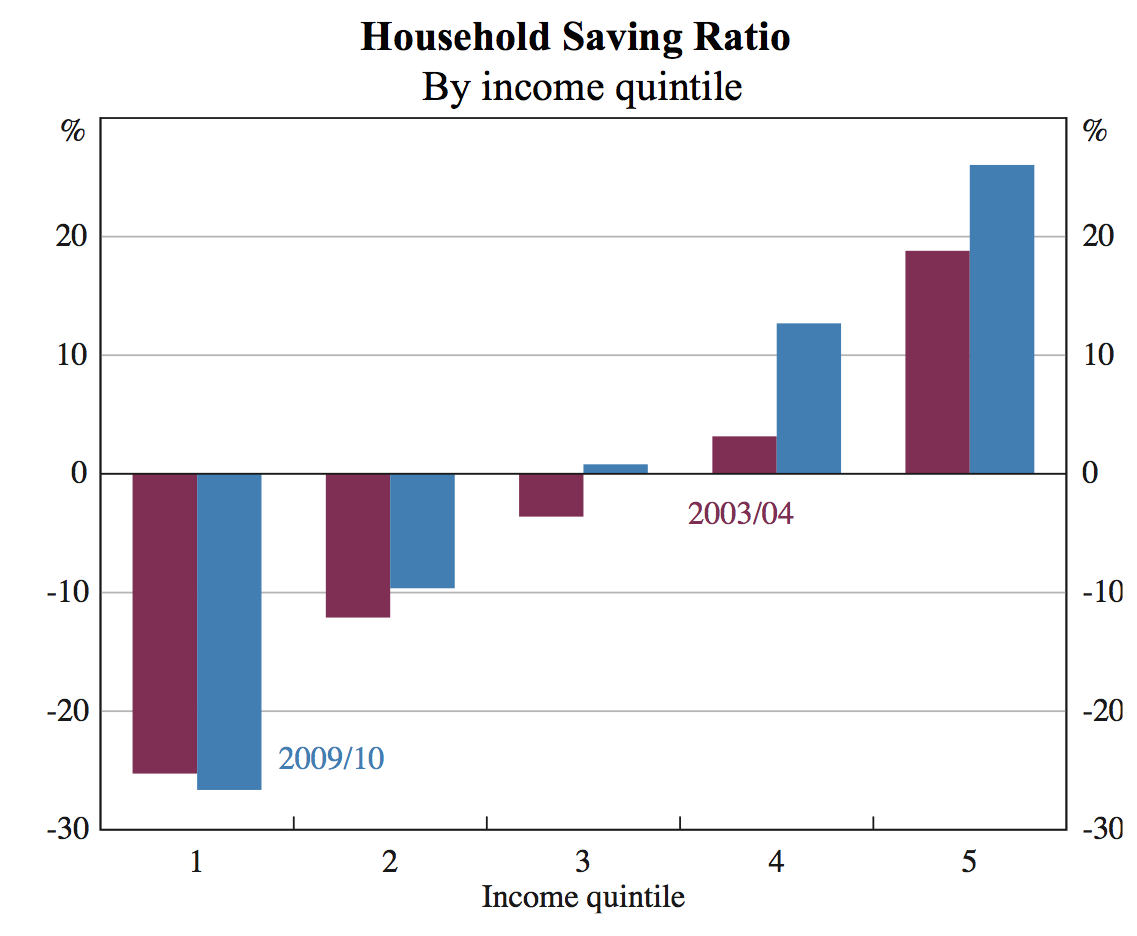

Income

The savings gap between rich and poor is even more extreme when separated by income: the top 20% of households save 25% of their income, compared to negative 26% for the lowest income earners.

As the RBA notes, that's actually somewhat counter-intuitive. 'Economic orthodoxy would suggest that a household's permanent or long-run level of income should not affect their saving ratio, since households with relatively high levels of permanent income would also have relatively high levels of consumption. Aggregate time series data on national saving supports this proposition: as countries grow richer, household incomes trend higher but saving ratios do not'. In practice, though, higher income does correlate with a higher rate of saving.

How you compare to others isn't the best way to judge your accomplishments, but knowing where you stand relative to the herd can still be empowering. Whether you should cut out that second morning coffee or take an overdue holiday to spend time with the kids is up to you.

To get more insights, stock research and BUY recommendations, take a 15 day free trial of Intelligent Investor now.