Large cap funds pedal fast but get nowhere

Everyone loves Australian equities. For savers they are an essential accessory, like a belt on baggy pants. Even though the local sharemarket has not recovered its pre-financial crisis high — is a very long way off it, in fact — portfolios around the country are still packed with Aussie stocks because they pay terrific dividends (relative to offshore companies) and franking tax credits make that income even more attractive.

Australian companies may be a popular asset class but the job of picking individual stocks is notoriously hard. Some investors labour over research and reports to make their own buy and sell decisions. Others may believe there is no hope of outsmarting every other buyer and seller, and so they use exchange-traded funds which grant them ownership of a small slice of the market.

And then there are those who pass the job to professional fund managers.

THE BIG END OF TOWN

Professional investors work hard all day, but at the end of it they have to measure their performance against a benchmark to show that they have done a good job. If a fund manager comes back at the end of a year and has made 8%, and he charges a 1.5% fee, the investor has made 6.5%.

The effects of compounding mean a small difference in fees will make a very big difference in return on capital over the long term. It is very important that fees are as low as possible. It’s not such a problem if the fund manager displays consistent ability to beat its benchmark.

Australian equities large cap managed funds are having trouble proving their worth to investors, and investment research company Morningstar estimates between 2011 and last June funds flowed out of Australian equities large cap funds to the tune of between $3 billion and $12 billion a year.

It’s impossible to say exactly where that money is being reinvested, but there has been a corresponding increase in flow of funds to exchange-traded funds.

LOOKING FOR VALUE

Dwindling interest in Australian large cap managers could be down to poor performance of the local market over the past five years, but some investors may be reacting to something else: the managers are not providing any value.

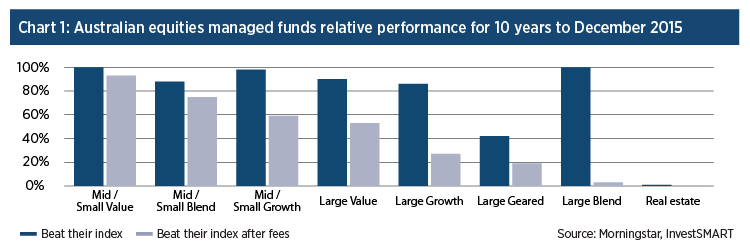

The first chart shows the percentage of funds by Australian equities investment strategy that have beaten their benchmark, and the percentage that outperformed after accounting for fees.

All Australian equities large cap blend funds beat their benchmark, but only 3% outperformed once fees had been included.

(For blend funds the investment strategy combines picking some stocks for their growth potential and others for their relative good value.)

“Outperforming the benchmark and peers on a risk-adjusted basis after fees is the ultimate justification, but it’s clearly impossible for every manager to do so,” said Morningstar senior analyst manager research Tim Wong in the Australian Equities Large-Cap Sector Wrap in January.

The results show how tough it is for growth and value strategy managers to prove their worth. Investors in nearly half the value funds would have done better with an ETF, and the same goes for almost three-quarters of the growth funds.

THE LONG RUN

The results only include funds with 10 years worth of performance data. It’s important to look at annualised long-term returns when assessing a manager for its skill so that short bursts of recent outperformance don’t skew the result. Also, managers sometimes have a tendency to change investment strategy and long-term performance is a better indicator of their abilities across different market conditions.

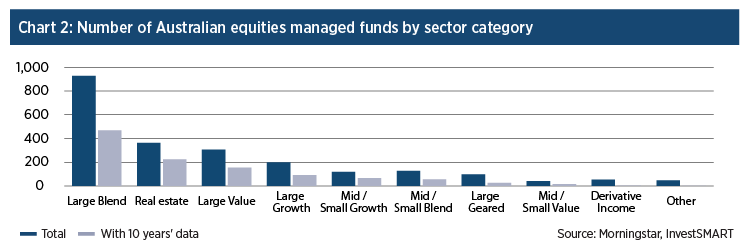

Narrowing our focus to funds with 10 years of data restricts the sample, however. Chart two shows the number of Australian equities managed funds by investment strategy category, as reported in December 2015. For many categories fewer than half the funds have been around long enough to accrue a decade of performance numbers.

OVERLY OVERLAPPED

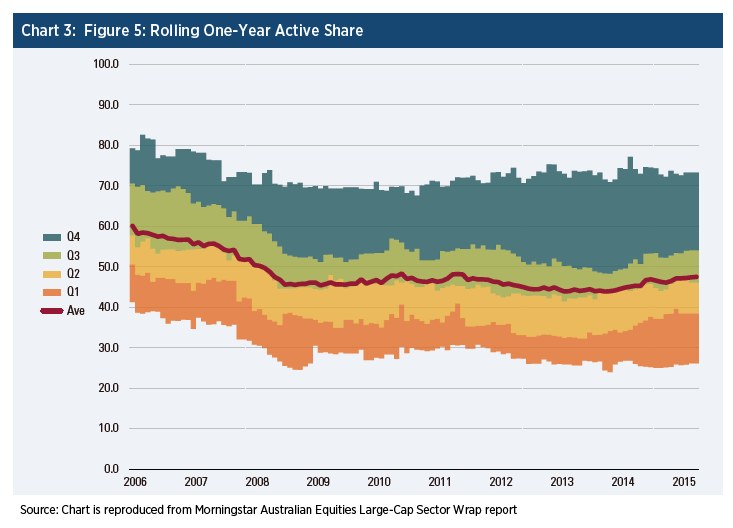

Morningstar’s Australian Equities Large-Cap Sector Wrap included the third chart, with shows the ratio of investment portfolio that is “active” for all large cap Australian equities funds. The “active” component of the portfolio is where the manager hopes to make gains in relation to an index.

As the GFC unfolded from 2007, managers sought safety by aligning their portfolios more closely with the benchmark, and so the proportion of portfolios that was “active” became lower. It didn’t pay to stand out from the crowd. The trend has continued.

“Active share for large cap managers has been dwindling,” says Tom Whitelaw, Morningstar director of manager research ratings, in the report. “This means they are doing less to beat the benchmark.”

Where about 60% of the average Australian large cap fund portfolio differed from the benchmark at the start of 2006, the ratio dropped to about 45% by mid-2008.

“When markets were going up and absolute returns were easy to come by, it seemed much easier to be active,” Whitelaw says. “The market’s 2007 sell-off then coincided with a sharp reduction in active share. That’s the survival instinct kicking in; you don’t get fired for losing money so long as everyone else is doing just as badly.”

WHERE FEES MEET RETURNS

The temptation which began in 2007 for large cap managers to seek safety in the benchmark has been hard to break free from. But the results for investors are obvious: after fees, only 3% of large cap managers beat the benchmark on 10-year annualised returns. As the managers were steering the funds towards becoming closer replicas of the benchmark, investors have responded by withdrawing their money. As the same time, ETFs which offer to track the benchmark for a much lower fee have attracted funds.

“Managers with active share scores of below 40 will find it extremely hard to outperform the index and their peer groups after fees have been taken into account,” Whitelaw says. “In most instances, investors would be better off choosing cheaper passive or exchange-traded funds or choosing a more benchmark-agnostic manager if they believe the index is for the beating.”

CLAWING BACK ALPHA

Large cap funds are still a long way off their pre-GFC levels of “active” management. If portfolio managers move to stem the flow of withdrawals, they may be tempted to take much higher risk in an attempt to beat the index.

That might pay off here and there, but the only thing that will lift long-term performance is consistent outperformance. The chance of that is very small.

It may be a very long time before Australian large cap funds prove their worth. In the meantime, the exodus to ETFs for benchmark exposure can be expected to continue.

Frequently Asked Questions about this Article…

Australian equities are popular because they offer attractive dividends and franking tax credits, making them a valuable asset class for investors seeking income.

Picking individual Australian stocks is challenging due to the difficulty in consistently outsmarting other market participants, leading many investors to rely on professional fund managers or exchange-traded funds (ETFs).

Fees significantly impact returns, as even a small difference in fees can lead to a large difference in long-term capital returns. It's crucial for fees to be as low as possible unless the fund manager consistently beats the benchmark.

Investors are moving away from Australian large cap managed funds due to their inability to consistently outperform benchmarks after fees, leading to a preference for lower-cost ETFs.

Active share measures the portion of a fund's portfolio that differs from the benchmark. A lower active share indicates less active management, which can make it difficult for funds to outperform the index after fees.

Since the Global Financial Crisis, large cap managers have aligned their portfolios more closely with benchmarks, reducing active share and making it harder to achieve outperformance.

Long-term performance trends show that only a small percentage of large cap funds outperform their benchmarks after fees, leading to increased interest in ETFs for benchmark exposure.

To improve performance, large cap fund managers might take higher risks to beat the index, but consistent long-term outperformance remains challenging, prompting many investors to choose ETFs instead.