How your behavioural traits can lead to substandard returns

| Summary: As market-index returns beating general investor results highlight, an investor's worst enemy is likely to be themselves. |

Key take-out: A successful investor must at times swim against the current of their inherent biological nature and remain exposed. |

Key beneficiaries: General investors. Category: Investment strategy. |

For many of us, the ability to retire comfortably and to see out the rest of days without financial stress or strain rates highly on the list of concerns.

This is particularly heightened as the exit from the workforce approaches, during periods of higher market volatility and as the legislative landscape continuously shifts, blurring the visual of the road ahead. The future is by its very nature an unknown and there will inevitably be a multitude of factors – both financial and non-financial – that cannot be pre-empted.

Experience has shown us however that investors who keep focus on the bigger picture and on controlling the controllables stand a greater chance of living out their best potential.

Here are the cornerstones:

Putting goals first

Goal setting not only reminds us why we are investing in the first place but creates the very framework for our investment life. As stated by Lewis Carroll, “If you don't know where you are going, any road will get you there”.

To get the most out of the exercise it is important to first develop a clear vision of the ideal future you would like to create. There are, of course, no boundaries or limitations on what might form your “why” – be it family related, travel, philanthropy, lifestyle and the list goes on. Together with the well-documented link between writing goals down and success, specificity is also an important factor.

Studies by American psychologist Edwin A. Locke have shown an improvement in the success rate where the goals are more specific in nature and ambitious, as compared to those which are general or seemingly easy to achieve.

Once the destination is defined with clearly articulated objectives at the core, then the pathway to best arrive there can be mapped out. This can be a daunting exercise given the potential multitude of moving parts. An advisor or financial coach can assist in working through what is achievable, breaking the vision into actionable steps and importantly tracking progress periodically.

Get the behaviour advantage

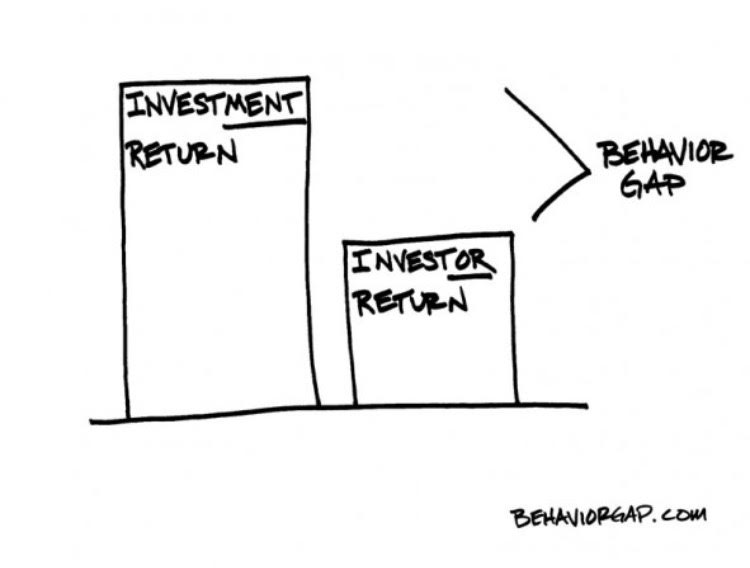

As human beings, we are subject to a range of cognitive or psychological behaviours which can go a long way to explaining why our financial decision making can at times be less than rational. As famously stated by Benjamin Graham, “The investor's chief problem and even his worst enemy is likely to be himself.”

A study by US company Dalbar shows that in the 20-year period ended December 2014, the S&P 500 market index delivered a return of 9.85 per cent per annum. The average investor, however, achieved a return of only 5.19 per cent p.a. (source Dalbar - Quantitative Analysis of Investor Behaviour 2015). That's right – almost half.

The astounding differential is measured by assessing, in the US context, the various flows in and out of managed funds, therefore the impact of emotion-based decision making, chasing winners and market mistiming. Had the investor simply stayed the course and applied a discipline and consistent exposure a substantially better result would have been achieved making a marked difference over time.

The difficulty here is that a successful investor must at times swim against the current of their inherent biological nature and remain invested through difficult times. Perhaps, just as anti-predator adaptations in the animal kingdom act as the first line of defence, we are predisposed to react in a manner which often contradicts good long-term investment. Understanding and arresting these tendencies can have a significant impact and mean a very real and tangible advantage.

A handle on outgoings

Many of us have a ‘ball park' grasp on what we spend but the ability to undertake this seemingly simple exercise seems to escape most of us. The basic reality is that having a solid handle on your outgoings is absolutely critical to gaining control of your financial future. The compounding impact of even seemingly small variances can make a marked difference to the picture as time goes by.

What you spend is a key variable in any meaningful modelling exercise. In analysing your budget, it pays to spend some time to dig a little deeper in order to understand what represents base living costs and what represents discretionary expenditure. This gives you control of a critical lever.

Thankfully, with the expansion of new technology, the need to have a qualification in spreadsheet creation can be replaced with any one of the savvy budget management apps on the market. These apps can, for example, track and categorise expenditure and apply the data against a target. Many options are free and are great steps to getting, and staying, on the road to financial fitness.

Consistency is key

Reducing or limiting the uncertainty about the future can be managed by taking a consistent approach to asset allocation. That is, your exposures to growth assets (like shares and property) and to defensive assets (like cash and bonds). Consistency can allow you to apply some reasonable assumptions about not only the volatility you might experience but also the corresponding reward.

An ever-changing asset mix not only plays on the natural instinct to ‘do something' when we likely should not, but detracts from the ability to draw conclusions about your portfolio's potential. This makes planning and the ability to make informed decisions about your future direction hard.

While it might be okay for a more speculative investor, for those looking to achieve a greater sense of certainty, limiting the range of possible outcomes will be most empowering.

It can be difficult to maintain a sense of clarity over the future. This is especially pertinent today as the sands of the superannuation environment continue to shift beneath our feet.

There are, however, things that an investor can do to maximise their confidence in their forward trajectory. Those who keep focus on the long-term objectives, control the controllables and remain disciplined in the face of testing times, no matter the prevailing commentary, are more likely to have a positive experience.

Carol Tawfik is a Certified Financial Planner and adviser with Affinity Private.