Woolworths: Competition cuts in - Pt 1

Recommendation

- {{x.value}}

{{ twilioFailed ? 'SMS Code Failed to Send…' : 'Enter verification code' }}

{{ completedStep1 ? 'Authentication & Security' : content.trialHeading.replace('{0}', user.FirstName) }}

{{ content.upgradeHeading.replace('{0}', user.FirstName) }}

The email address you entered is registered with InvestSMART

Please login to continue

We have sent you an email with the details of your registration.

Looks you are already a member. Please enter your password to proceed

{{ upgradeCTAText }}

Updating information

Please wait ...

Your membership to InvestSMART Group recently failed to renew.

Please make sure your payment details are up to date to continue your membership.

Having trouble renewing?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

You've recently updated your payment details.

It may take a few minutes to update your subscription details, during this time you will not be able to view locked content.

If you are still having trouble viewing content after 10 minutes, try logging out of your account and logging back in.

Still having trouble viewing content?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

Please click on the ACTIVATE button to activate your Intelligent Investor 15-day free trial

Please click on the ACTIVATE button to finalise your membership

Unsuccessful registration

Registration for this event is available only to Eureka Report members. View our membership page for more information.

Registration for this event is available only to Intelligent Investor members. View our membership page for more information.

- You are already registered for this event.

- This event is already full.

- Please select a quantity for at least one ticket.

- {{ i }}

Forgotten password

Please enter your email address below to request a new password

- Indepth analysis of ASX listed shares

- BUY, Hold and Sell Recommendations

- Ideas Lab

- Special Reports

- Alan Kohler’s Weekend Briefing

- Interviews with CEO’s & top influencers

- Money Cafe and Talking Finance

- Super Advice and Q&A with Ask Alan

Very occasionally, one number tells the story. In Woolworths' case, it was the relentless rise in margins. Over the ten years to 2015, Woolworths allowed the operating margin in its Australian food, liquor and petrol business to expand from 4.1% to 7.4%.

Woolworths' operating margin, which was more like 8% if petrol was excluded, became the highest of any grocery retailer in the world. Shareholders and analysts alike – yes, our hands are up – became enamoured of Woolworths' success.

As everyone now realises, it was a monstrous mistake. Woolworths' margin expansion was evidence that it was taking its market position for granted. Retailing is ultra-competitive, and the first law of capitalism is that outsized margins eventually attract competition.

Key Points

-

Woolworths will face greater competition

-

Margin recovery not required for good outcome

-

Some risk of capital raising

The margins that Woolworths reported in 2015 are now gone forever. In the 2016 financial year Woolworths' food, liquor and petrol operating margin will fall to around 5% as management takes steps to win back customers' trust. But will it be enough?

International competition has well and truly arrived. German discounter Aldi in particular is now entrenched in Australia's eastern states, with almost 400 stores. Many of them are located near a Woolworths or Coles, making it easy for customers to pick and choose. Shoppers aren't loyal; more than three-quarters visit at least two supermarkets over the course of a month.

Really cheap, cheap

Aldi's cheap prices – a direct result of its low-cost structure – mean sales have risen to more than $7bn since launch in 2001. Its focus on relatively few products gives it huge buying power in the lines it does stock.

Aldi's market share now exceeds 10%, and it's higher in the eastern states. The business is also pretty profitable, with an operating margin above 5%, more than it earns in most markets overseas.

Unfettered by the need to focus on short-term profits, Aldi will happily sacrifice margin to further its ambitions. This year's entry into South Australia and Western Australia will be costly, with the retailer planning on opening up to 35 stores in the two states this year alone. It expects to have 120 stores west of Cameron Corner by the end of the decade.

Buy-in-bulk US giant Costco now has permanent residency too, with eight Australian warehouses open and sales of $1.3bn last year. The cat food-to-coffins retailer (yes, really) is widely considered to be targeting sales of $4bn in Australia.

Aldi and Costco are just the retailers who are already here. German grocery discounter Lidl has also been registering trademarks in Australia, suggesting it intends to launch at some point. Then there's the fact that an executive of Amazon recently remarked that its grocery delivery arm, Amazon Fresh, had the potential to generate ‘billions of dollars in Australia in terms of grocery sales'.

Of course, there's also the competition Woolworths has been facing for years. Woolworths has now underperformed Coles on same-store sales growth for 27 consecutive quarters. Even Metcash's IGA banner looks in less trouble than before, with the wholesaler working on lowering prices, improving the fresh offer, and refurbishing stores.

Grocery market competition looks more intense than ever. And while the six competitors we've mentioned are top of mind right now, you can bet others will emerge. So what does it all mean for Woolworths?

Self-inflicted wounds

We'll answer that question in Part 2 but, in preview, competition is less intense than the media makes out. Woolworths' wounds are primarily self-inflicted and, while greater competition makes the company's turnaround more difficult, there are many things management can do – and is doing – to improve performance.

Nevertheless, there is obviously the potential for an outcome worse than what is implied by our Buy recommendation. So what's our base case, and just how bad could it get?

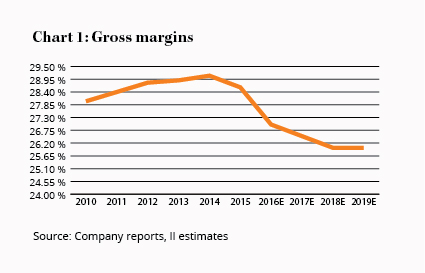

Our base case rests on a contraction in Woolworths' food and liquor gross margin from almost 29% in 2015 to 26% in 2019 (see Chart 1). This decline will be the direct result of the company becoming more price-competitive over time. In turn, we expect an Australian food and liquor operating margin of approximately 5% in that year (compared with 8% in 2015).

In short, Woolworths can still be a decent investment if its 2019 Australian food and liquor earnings are 30% below the mirage that was 2015. We don't need a recovery in earnings – in Australian food and liquor, anyway – for the stock to produce an acceptable return from here.

However, an operating margin significantly below 5% will mean Woolworths turns out to be a poorer than expected investment. In more competitive grocery markets – such as the USA and the UK – operating margins can be as low as 2–3%. If that's where Woolworths' margins are heading, then our Buy recommendation will be a mistake.

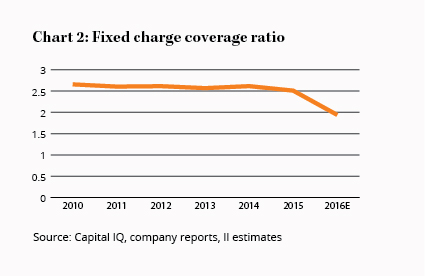

If earnings continue to erode, then Woolworths' financial position will worsen. Whatever happens in a few years, in the short term there is the risk that weaker earnings will impact solvency. You can see the effect of this in the deterioration of the company's fixed charge coverage ratio in Chart 2. This ratio measures how well earnings ‘cover' fixed charges like rent and interest.

Warning signs

There are already a few warning signs that Woolworths' financial position has deteriorated. At the 2016 interim result, the company flagged it was introducing a 1.5% discount on its dividend reinvestment plan, which will help retain more cash for store refurbishments and the like.

The company is also reportedly stretching out payment terms to suppliers, which means it hangs on to cash for longer. The downgrades to the company's credit rating, most recently Standard & Poor's cut to BBB, are further recognition Woolworths is less financially secure.

A capital raising, then, is certainly possible. After a period of underinvestment, managing director Brad Banducci might decide the company needs to accelerate store refurbishments. If so, raising capital sooner rather than later should be his preferred option.

So competition has intensified and Woolworths has been caught napping. In Part 2, we'll examine why the competitive threats might be overstated and what Woolworths is doing to fix its problems. As outlined in Woolworths takes tough decisions, our initial suggested portfolio weighting remains 2–3%, while our recommendation is BUY.

Note: The Intelligent Investor Equity Income Portfolio owns shares in Woolworths. You can find out about investing directly in Intelligent Investor and InvestSMART portfolios by clicking here.

Recommendation