Wesfarmers' coal curveball

Recommendation

- {{x.value}}

{{ twilioFailed ? 'SMS Code Failed to Send…' : 'Enter verification code' }}

{{ completedStep1 ? 'Authentication & Security' : content.trialHeading.replace('{0}', user.FirstName) }}

{{ content.upgradeHeading.replace('{0}', user.FirstName) }}

The email address you entered is registered with InvestSMART

Please login to continue

We have sent you an email with the details of your registration.

Looks you are already a member. Please enter your password to proceed

{{ upgradeCTAText }}

Updating information

Please wait ...

Your membership to InvestSMART Group recently failed to renew.

Please make sure your payment details are up to date to continue your membership.

Having trouble renewing?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

You've recently updated your payment details.

It may take a few minutes to update your subscription details, during this time you will not be able to view locked content.

If you are still having trouble viewing content after 10 minutes, try logging out of your account and logging back in.

Still having trouble viewing content?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

Please click on the ACTIVATE button to activate your Intelligent Investor 15-day free trial

Please click on the ACTIVATE button to finalise your membership

Unsuccessful registration

Registration for this event is available only to Eureka Report members. View our membership page for more information.

Registration for this event is available only to Intelligent Investor members. View our membership page for more information.

- You are already registered for this event.

- This event is already full.

- Please select a quantity for at least one ticket.

- {{ i }}

Forgotten password

Please enter your email address below to request a new password

- Indepth analysis of ASX listed shares

- BUY, Hold and Sell Recommendations

- Ideas Lab

- Special Reports

- Alan Kohler’s Weekend Briefing

- Interviews with CEO’s & top influencers

- Money Cafe and Talking Finance

- Super Advice and Q&A with Ask Alan

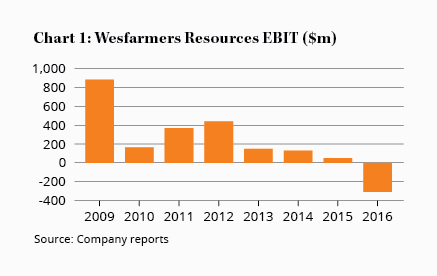

The announcement of a ‘First Half Earnings Update' often foreshadows bad news but in Wesfarmers' case it was the opposite. Last week the company announced that its Resources division – which mines coal – would produce operating earnings of $135m–$140m for the first half of 2017.

‘So what?' you might think. Well, what's surprising is that back in October Wesfarmers forecast the division would only break even in the first half.

It just goes to show that, especially in the resources sector, forecasting earnings is a fool's errand. If Wesfarmers can't forecast a $140m turnaround in earnings three months out, what hope do the rest of us have? You can see the volatility of earnings from the Resources division in Chart 1.

Key Points

-

Coal prices helping Resources division

-

Woolworths price cuts hurting Coles

-

Bunnings entering slower period

The turnaround has been driven largely by soaring coal prices as China cuts capacity at its mines. Prices for metallurgical (or coking) coal have been particularly strong. Wesfarmers' flagship coal mine Curragh is a significant producer of high-quality metallurgical coal and, to take advantage of the high prices, it ramped up production during the quarter. Second-quarter metallurgical coal production at Curragh was up 41% on the weather-affected previous quarter, so the timing was fortuitous.

It's impossible to tell where coal prices will go from here, although they have been weakening again lately. The price rise will, however, help Wesfarmers should it decide to sell the coal assets.

The sum-of-the-parts valuation we outlined in Wesfarmers counts on Chaney just over a year ago valued the Resources division between $1.0bn and $2.5bn. For the reasons outlined then, even the top end might have been a conservative valuation, which the recent strength in coal prices has helped confirm.

Upside surprise?

It's now hard to imagine Wesfarmers selling its Resources division for less than $3bn although it might take a haircut simply to remove the reputational risk that comes with owning coal mines. Management has valued the assets at significantly more than $3bn in the past and, assuming the sale takes place, the eventual figure could surprise the market.

While Wesfarmers' Resources division was last year's ugly duckling – Target was a close second – that moniker may pass to Coles in calendar 2017. Management has apparently been telling broking analysts that its sales growth is being affected by Woolworths' investment in price. Christmas trading for Woolworths was also better than at Coles.

Coles, then, is expected to report anaemic same-store sales growth for the December quarter. Indeed, its sales growth is expected to be below Woolworths for the first time in years. This isn't quite as bad as it sounds for Coles – same-store sales for the December 2015 quarter was a strong 5.3%, which makes it a tough comparison to beat.

We've long wanted to buy Wesfarmers and 2017 may be the year. With Coles slowing and Bunnings' growth also likely to tail off, there's some chance of disappointment. Bunnings' John Gillam has stepped down and it's possible managing director Richard Goyder might choose to move on sooner rather than later too. All in all, it could be a year of disruption for Australia's largest retailing conglomerate.

Flagging these changes will help us be prepared. For now, we're waiting and watching but this is definitely a company we'd like to own. HOLD.

Recommendation