Unibail-Rodamco-Westfield: A bear case

Recommendation

- {{x.value}}

{{ twilioFailed ? 'SMS Code Failed to Send…' : 'Enter verification code' }}

{{ completedStep1 ? 'Authentication & Security' : content.trialHeading.replace('{0}', user.FirstName) }}

{{ content.upgradeHeading.replace('{0}', user.FirstName) }}

The email address you entered is registered with InvestSMART

Please login to continue

We have sent you an email with the details of your registration.

Looks you are already a member. Please enter your password to proceed

{{ upgradeCTAText }}

Updating information

Please wait ...

Your membership to InvestSMART Group recently failed to renew.

Please make sure your payment details are up to date to continue your membership.

Having trouble renewing?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

You've recently updated your payment details.

It may take a few minutes to update your subscription details, during this time you will not be able to view locked content.

If you are still having trouble viewing content after 10 minutes, try logging out of your account and logging back in.

Still having trouble viewing content?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

Please click on the ACTIVATE button to activate your Intelligent Investor 15-day free trial

Please click on the ACTIVATE button to finalise your membership

Unsuccessful registration

Registration for this event is available only to Eureka Report members. View our membership page for more information.

Registration for this event is available only to Intelligent Investor members. View our membership page for more information.

- You are already registered for this event.

- This event is already full.

- Please select a quantity for at least one ticket.

- {{ i }}

Forgotten password

Please enter your email address below to request a new password

- Indepth analysis of ASX listed shares

- BUY, Hold and Sell Recommendations

- Ideas Lab

- Special Reports

- Alan Kohler’s Weekend Briefing

- Interviews with CEO’s & top influencers

- Money Cafe and Talking Finance

- Super Advice and Q&A with Ask Alan

Members who followed our original Unibail-Rodamco-Westfield recommendation (Buy at $14.24) will be understandably disappointed - holders have been lumped with a negative 23 per cent return.

Is the share price telling us something? Ben Graham - father of value investing - told us that 'the market is there to serve you, not guide you', so it's easy to write it off as market volatility.

But the only way to know for sure is consider why sellers are selling. If you can't state their point of view clearly, you run the risk of getting blindsided. So, with Unibail's stock consistently lower, it's time to ask: are we being blindsided?

Let's revisit the bear case.

Key Points

-

Exploring the bear case

-

Well compensated for risks

-

Setting down markers

Bear argument #1: Management lacking

Let's start here, because it's one of our biggest gripes with Unibail too. As we explained in 'URW's first result falls flat', this is how management prefaced an earnings downgrade earlier this year:

UNIBAIL-RODAMCO-WESTFIELD, THE PREMIER DEVELOPER AND OPERATOR OF FLAGSHIP SHOPPING DESTINATIONS, REPORTS STRONG RESULTS FOR 2018

It seemed like it was going to be good. Except it wasn't - the share price promptly fell 10 percent once shareholders uncovered the tiny detail about a distribution cut.

This sort of commentary earns a black mark from us, and it's one of the reasons we slashed the price guide and raised our risk rating (to Medium-High).

The reasons for the Unibail-Rodamco/Westfield merger also appear shaky. Shareholders were promised that lower funding costs, synergies, extra rental income and the roll-out of the Westfield brand would lead to a post-merger rise in earnings per share.

But those promises were forgotten and guidance downgraded. Shareholders have been left with the worst of both worlds: higher gearing and lower earnings per share. It's a bitter pill to swallow.

That said, Unibail still houses the worlds finest shopping malls, nicely diversified by geography and a pipeline of promising development. We're giving management another chance, with the caveat that any further signs of poor capital allocation may kill our investment case. It's something we'll need to watch closely.

Bear argument #2: e-Commerce will kill bricks-and-mortar retail.

There are other challenges to contend with. In Europe, online sales have grown at around 17% annually since 2004 and now makeup 12% of all retail sales. There's no end in sight, either, because technology keeps improving so that once unimaginable online experiences are commonplace.

You can now see how a couch looks inside your living room with the Ikea Place app; Instagram is fast positioning itself as an online shopping centre, complete with a browsing and check-out experience; and shoppers can now virtually 'try on' clothes. Additionally, as logistics improve, same-day delivery is fast becoming the norm, and more online retailers are supplying return packages with your order for added convenience. Online shopping is faster, more convenient and cheaper than ever before.

It's a sure thing growth for shopping centres will be lower than in an internet-free world, but does this mean brick-and-mortar retail is dead? For neighbourhood shopping centres that exist solely for run-of-the-mill transactions, we wouldn't bet against it.

But we'd argue that premium shopping centres - those that are well-located and create inviting hubs where people can enjoy novel experiences and entertainment - can offer something a purely online retailer can't: a good day out.

Adding fuel to the debate are brands like Apple, Warby Parker and even Amazon, who are finding that combining physical showrooms with websites, online sales, apps and social media - so-called 'omni-channel' marketing - is a successful way to build a brand. These retailers should soak up space vacated by ailing, conventional chains.

It's still not clear whether creating 'living centres' will be a good business. Shopping centres are likely to be more capital intensive than they've been in the past - upgrading aesthetics, revamping communal areas and offering attractions is expensive.

And the online-physical dynamic muddies the picture further. Consumers are more likely to purchase something they've seen in-store online - so there isn't a clear relationship between in-store sales and the value added by a physical retail presence.

That's why footfall - as opposed to annual in-store turnover - is fast becoming the key operating metric to watch. Rising footfall would be a 'proof-of-concept' for living centres, and here there is some good news: Footfall across URW's European assets rose 1.8% last year. If these figures begin to deteriorate, however, we need to be prepared to change our mind quickly.

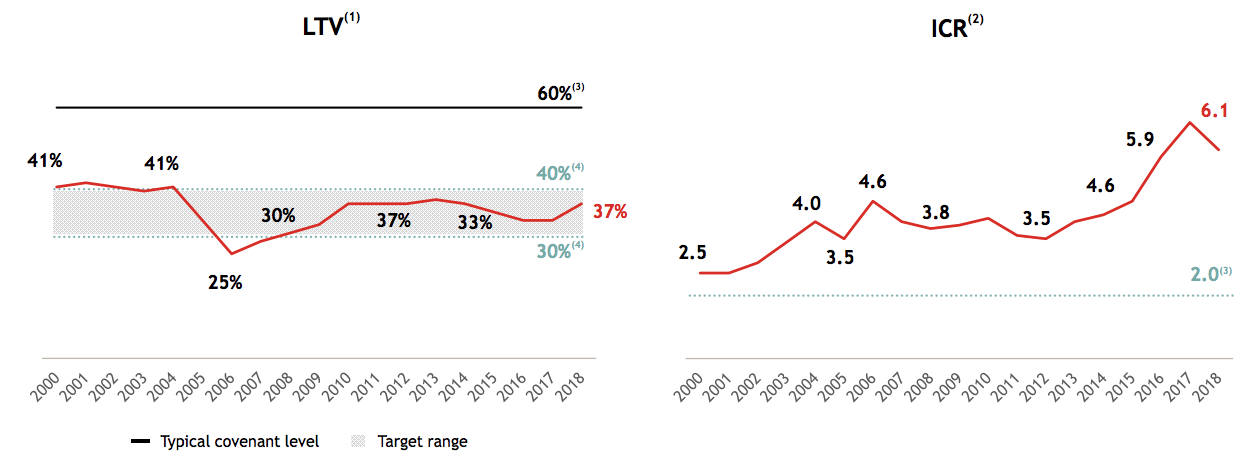

Bear argument #3: Debt too high

Excessive debt is another proven way property trusts become unstuck, and Unibail has its fair share. The trust had to take on a good chunk of debt to finance the Westfield takeover - so large it incurred a US$103m advisory bill.

It's easy to lever up when interest rates are falling, asset values are rising, consumers are spending and credit is easy to come by. But it's best to maintain a conservative level of gearing for when things inevitably turn the other way.

We admit we'd feel more comfortable with lower debt, but there are counter-arguments here. For starters, while URW's loan-to-value (LTV) ratio rose to 37% at the end of 2018, that still leaves plenty of headroom under the 60% covenant requirements. Same for the interest coverage ratio; at 6 times, it's well above the requirement of 2 times.

And with interest rates across the world at or near record lows, it's a highly favourable time to be a borrower. With the cost of debt so low, and much of global debt issuance 'covenant-lite', it arguably makes sense for companies to gear up - especially at longer maturities. URW's recent €500m placement for 30 years at a record-low 1.75% is a case in point.

Bear argument #4: Distribution unsustainable

| Expansion (bp) | Gearing (%) | NAV per share (€) | NAV per CDI (AU$) |

|---|---|---|---|

| Unchanged | 37 | 222 | 18 |

| 50 | 40 | 182 | 15 |

| 100 | 44 | 150 | 12 |

| 150 | 47 | 123 | 10 |

| 250 | 54 | 72 | 6 |

| *Assumes all other variables constant. | |||

| Fall in net operating income (%) | Gearing (%) | NAV per share (€) | NAV per CDI (AU$) |

|---|---|---|---|

| Unchanged | 37 | 222 | 18 |

| 5 | 39 | 198 | 16 |

| 10 | 41 | 175 | 14 |

| 15 | 44 | 151 | 12 |

| 20 | 46 | 127 | 10 |

| *Assumes all other variables constant. | |||

| Asset sales (€b)** | Distribution yield (%) |

|---|---|

| 0 | 8.2 |

| 2 | 7.8 |

| 4 | 7.1 |

| 6 | 6.0 |

| 9 | 4.3 |

| *Assumes all other variables constant. | |

| **Above current target of €6b | |

Either way, management thinks gearing is a little too high, so the targeted range was lowered from 35-45% to 30-40%. To bring this about, management opted to increase planned asset sales from €3bn to €6bn.

That's important; Because the assets are financed at such low rates, URW's yield per share inevitably falls when they're sold. More asset sales, therefore, result in lower distributions.

Management is at pains to dispel concerns around this - at a recent investor day, one presentation repeated that the 'dividend is sustainable' no less than six times. Additionally, they're anticipating growth of 5-7%, which if true would mean shareholders are in for good times ahead.

But so far, URW is about halfway through asset sales and it's not clear if this will be enough. If capitalisation rates rise or rent increases dry up or reverse, assets will be revalued lower and Unibail's gearing will rise further. And given an enormous development pipeline - $12b at last count - further asset sales are a possibility.

Bottom line

To get an idea of the potential downside, we've included a table that shows the effect of a few bearish assumptions, although these are intended to be a rough guide rather than gospel.

What we've outlined above are what we believe to be the main bear arguments (If you think there are any we've missed, we'd love to hear your thoughts below in the comments). This idea isn't risk free but no decent idea is. The idea isn't to avoid risk altogether but to be well compensated for taking it on. We think that's the case here.

URW's 40 per cent discount to net asset value and 8 percent yield tell us the market is already factoring in plenty of negativity. It won't take much good news from here for members to achieve a reasonable result, which is why we're staying put. BUY.

Recommendation