The Thorn identity

- {{x.value}}

{{ twilioFailed ? 'SMS Code Failed to Send…' : 'Enter verification code' }}

{{ completedStep1 ? 'Authentication & Security' : content.trialHeading.replace('{0}', user.FirstName) }}

{{ content.upgradeHeading.replace('{0}', user.FirstName) }}

The email address you entered is registered with InvestSMART

Please login to continue

We have sent you an email with the details of your registration.

Looks you are already a member. Please enter your password to proceed

{{ upgradeCTAText }}

Updating information

Please wait ...

Your membership to InvestSMART Group recently failed to renew.

Please make sure your payment details are up to date to continue your membership.

Having trouble renewing?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

You've recently updated your payment details.

It may take a few minutes to update your subscription details, during this time you will not be able to view locked content.

If you are still having trouble viewing content after 10 minutes, try logging out of your account and logging back in.

Still having trouble viewing content?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

Please click on the ACTIVATE button to activate your Intelligent Investor 15-day free trial

Please click on the ACTIVATE button to finalise your membership

Unsuccessful registration

Registration for this event is available only to Eureka Report members. View our membership page for more information.

Registration for this event is available only to Intelligent Investor members. View our membership page for more information.

- You are already registered for this event.

- This event is already full.

- Please select a quantity for at least one ticket.

- {{ i }}

Forgotten password

Please enter your email address below to request a new password

- Indepth analysis of ASX listed shares

- BUY, Hold and Sell Recommendations

- Ideas Lab

- Special Reports

- Alan Kohler’s Weekend Briefing

- Interviews with CEO’s & top influencers

- Money Cafe and Talking Finance

- Super Advice and Q&A with Ask Alan

With the stroke of a pen, legislators can permanently change the fortunes and futures of businesses forever. APRA could force the banks to raise capital and slash the funding of the vocational education, heathcare and childcare sectors. As we noted in How to Back Rudd and McMillan, the viability of an industry can depend on a vote.

Does this mean businesses facing regulatory risk should be avoided? Not at all. In fact, the fear of regulatory change can deliver opportunities if uncovered at the right time. In our view, Thorn Group is one such example.

With concern over usurious interests rates, excessive penalty fees and unfair terms mounting, just over a year ago the Federal Government announced a review of the laws regulating Small Amount Credit Contracts (SACC). These are the kinds of agreements those on low incomes might enter into when they can't pay for a fridge or dishwasher outright, or need a payday loan to tide them over.

Key Points

-

Regulatory risk is overplayed

-

Business growth will offset Radio Rentals softness

-

FY16 one-offs are indeed one-off

When the SACC review was announced on 7 August 2015, Thorn Group shares were changing hands at $2.50. Yesterday, they closed at $1.50, a 40% fall in just over a year. The market view is that Thorn will be adversely affected by the new laws. Our analysis suggests those fears are overdone.

Thorn is cheap as a result, or at least it was when we started our research. This detailed review is in the hope the price may fall by 10% or so, which would be enough to tempt us to put it on our buy list.

Consumer leasing

You may have heard of Radio Rentals, Thorn's best business, which accounts for four-fifths of group earnings (we'll get to the others later). Radio Rentals began financing radio purchases in the Great Depression and now offers a wide range of credit options for the purchase of everyday items like electronics, furniture and whitegoods. Over 70% of Radio Rentals customers say it is the only way for them to access essential goods and 92% rate it as affordable, a sharp contradiction to the claims that Thorn's leasing practices are predatory.

This is a business with a clear, established niche, one often compared with unsecured lenders like Cash Converters. Whilst there is some customer overlap there are two important differences that make Thorn a far more attractive business. First, whilst Cash Converters makes unsecured loans which can be used for everyday expenditure, its loans can instead be shovelled into a poker machine. Radio Rentals only finances equipment purchases with collateral. Should the lease go unpaid, the asset can be seized and re-rented, reducing arrears.

Second, Radio Rentals receives a large portion of payments – some estimate as much as half – directly from Centrepay, a service that automates bill payments for Centrelink customers. This dramatically reduces the risk of bad debts. If a Radio Rentals customer chooses to use the Centrepay service, Radio Rentals is paid before the Centrelink client receives their payment, reducing the risk of funds being misspent. Unfortunately, this adds to the regulatory risk, which we'll get to.

After 80 years Radio Rentals has become the country's dominant consumer leasing business. With an estimated market share twice that of nearest competitor Walker Stores, the scale delivers purchasing power that can be passed on to customers. A 65-inch smart UHD LED TV costs $35.28 per week at Radio Rentals but $66.85 at Walker's RT Edwards stores. Radio Rental's country-wide network dwarfs competitors that only operate in certain geographic pockets.

Scale advantages

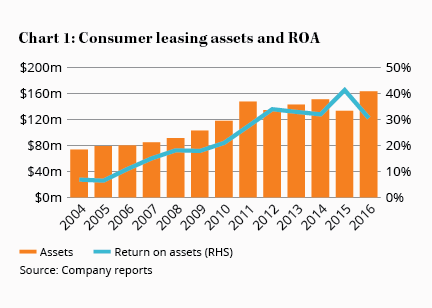

The size of the business also means funding costs are lower than competitors, along with product and compliance costs. As assets have increased, the return on those assets has also increased (measured using earnings before interest and tax to assets – see Chart 1). The bigger Radio Rentals becomes, the more profitable it gets.

| Bear | Base | Bull | |

| NPAT | 8x | 10x | 12x |

| $26m | $1.35 | $1.68 | $2.02 |

| $28m | $1.45 | $1.81 | $2.17 |

| $30m | $1.55 | $1.94 | $2.33 |

Against the background of adverse regulatory changes, this long-term history has been forgotten. The market has concluded that Thorn's future profitability will be greatly reduced. How else can one explain a company with a long history of profit and market share growth, and satisfied customers, trading on an underlying price-earnings ratio of just six?

This fear isn't entirely irrational. The final report issued 24 recommendations, including pricing caps and restrictions on the size of total leases relative to income. These reduce the implied interest rates on leases and limit the amount that can be loaned to each consumer. But only 3% of customers currently exceed these restrictions, so the likely impact is probably less than the market expects. That said, if Radio Rentals earns less, Thorn is worth less (although far from worthless). ASIC is also conducting a review into Thorn's lending practices, which has only exacerbated these concerns.

The company's response to the review's findings is instructive, pre-empting the legislation by implementing price caps across its business. This will reduce margins on some products, but not as much as the share price fall would indicate. Our worst case expectation is that Radio Rentals' earnings will fall by about $5m this financial year. A valuation guide which includes our net profit estimates for 2017 is summarised in Table 1.

And there's a hidden benefit. More price caps will only enhance Radio Rentals' reputation for price leadership. There's every chance the company can increase sales volumes by taking market share from more expensive competitors. The new rules could enhance the market power of the biggest players at the expense of the smallest. Thorn may have the opportunity to acquire competitors at attractive prices as it turns the screws.

Business finance

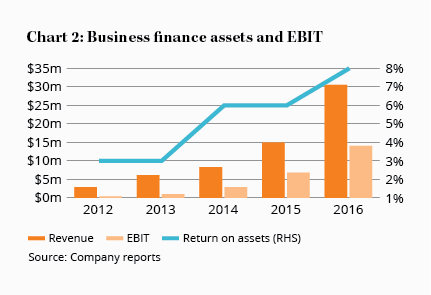

What of the company's other businesses? Thorn's business finance division is showing promise. By targeting the areas underserviced by the major banks, it has carved out a profitable niche providing equipment and trade debtor finance for small businesses.

Revenue is up tenfold since 2012, with EBIT reaching $14m in 2016 (see Chart 2). With loan receivables up 60%, this year could be one of further growth. Potential falls in Radio Rentals' future earnings could well be offset by handsome profit growth in the company's finance division, another possibility that Thorn's share price seems not to acknowledge.

| FY16 | |

| Underlying NPAT | 30.3 |

| – Goodwill impairment | (6.7) |

| – Customer credit refunds | (2.8) |

| – Asset revaluations | (2.3) |

| – Tax effect | 1.5 |

| Reported NPAT | 20 |

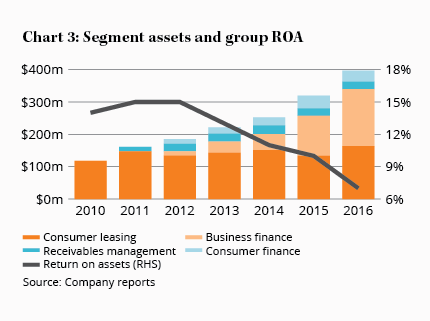

Thorn also has a renewed focus on profitability. In a classic case of ‘diworseification' in 2011, it bought a debt collection business and created two other finance divisions. Chart 3 shows how much value this destroyed. No one paid much attention to the plummeting return on assets because Radio Rentals' rising profitability was papering over the cracks.

New management has cottoned on to the problem – and solved it with the sale of the consumer loans business. National Credit Management Ltd (NCML), the debt collection business, has also been restructured. The consequence is that $37m in capital can now be recycled from low-return businesses to the star performers. With the current financial year (to March 2017) free from the $10.3m in one-offs incurred last year, statutory earnings are set to jump by about 30–50% on our numbers.

Thorn's return on equity has historically averaged about 20% but setbacks last financial year saw that figure halve. With earnings set to rebound, Thorn is on track to reclaim its former highs. At closer to book value ($1.30), we'd look to make Thorn Group a Buy – and we'll watch it closely for an opportunity. Unless and until we reach that point, though, we won't be initiating formal coverage.