Tatts: The lottery that always pays?

Recommendation

- {{x.value}}

{{ twilioFailed ? 'SMS Code Failed to Send…' : 'Enter verification code' }}

{{ completedStep1 ? 'Authentication & Security' : content.trialHeading.replace('{0}', user.FirstName) }}

{{ content.upgradeHeading.replace('{0}', user.FirstName) }}

The email address you entered is registered with InvestSMART

Please login to continue

We have sent you an email with the details of your registration.

Looks you are already a member. Please enter your password to proceed

{{ upgradeCTAText }}

Updating information

Please wait ...

Your membership to InvestSMART Group recently failed to renew.

Please make sure your payment details are up to date to continue your membership.

Having trouble renewing?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

You've recently updated your payment details.

It may take a few minutes to update your subscription details, during this time you will not be able to view locked content.

If you are still having trouble viewing content after 10 minutes, try logging out of your account and logging back in.

Still having trouble viewing content?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

Please click on the ACTIVATE button to activate your Intelligent Investor 15-day free trial

Please click on the ACTIVATE button to finalise your membership

Unsuccessful registration

Registration for this event is available only to Eureka Report members. View our membership page for more information.

Registration for this event is available only to Intelligent Investor members. View our membership page for more information.

- You are already registered for this event.

- This event is already full.

- Please select a quantity for at least one ticket.

- {{ i }}

Forgotten password

Please enter your email address below to request a new password

- Indepth analysis of ASX listed shares

- BUY, Hold and Sell Recommendations

- Ideas Lab

- Special Reports

- Alan Kohler’s Weekend Briefing

- Interviews with CEO’s & top influencers

- Money Cafe and Talking Finance

- Super Advice and Q&A with Ask Alan

Online lottery ticket seller OzLotteries has some advice for hopeful customers: "Experienced lotto players use various techniques in order to improve their chance of getting a prize … Although every single number is randomly drawn, there are certain numbers which appear more often than others, known as ‘hot numbers'."

A more useful bit of guidance would be that buying a Powerball ticket gives you a 1 in 77 million chance of winning the jackpot – which is only slightly less likely than you being killed by an asteroid impact this year.

Lotteries are designed to be a bad deal for punters. And that's precisely why Tatts Group – which operates all the lotteries in Australia, except those in Western Australia – has been a fountain of cash for shareholders year in, year out. The odds are in its favour.

Key Points

-

Lotteries is a good business

-

Wagering faces ongoing decline

-

Fair valuation; Hold

What's more, Tatts requires almost no capital to operate – it's just a collection of marketing and IT staff, computers and a roof over their heads. The company spent just 1.5% of revenue on property and equipment in 2015.

This has a couple of benefits. The first is that Tatts essentially earns infinite returns on tangible capital, and, after taking intangible assets such as licences into account, a return on equity of around 9%.

The second benefit is that Tatts doesn't need to keep reinvesting profits to upgrade expensive equipment – though it does have to keep buying licences, which we'll get to in a minute – so free cash flow has come in slightly ahead of net profit in each of the past five years.

Compare this to, say, Oil Search, which must constantly use last year's profits for the exploration and development of new oil and gas bodies, leaving little cash left over for dividends. Tatts, on the other hand, can use its cash flow to grow the business or direct it to shareholders. The company has paid out more than 90% of profits as dividends since listing in 2005.

The licence problem

There's no debate: lotteries are a great business. The catch is that for the privilege of operating a state lottery, you need to buy a licence from the Government (is there never a free lunch?). They're expensive, too. When Tatts bought the 40-year licence to operate NSW Lotteries in 2010, it had to fork out $850m.

The need to keep buying licences does add an element of risk to an otherwise low-risk business model. Being the incumbent with a near-monopoly gives Tatts a significant advantage when bidding for the licence renewal, but it could still be caught overpaying. Perhaps worse, the Government could award the licence to a foreign competitor or not renew the licence at all, as was the case for Tatts' Victorian pokies operation in 2012 (see Tatts loses pokie compensation case).

Nonetheless, these are mainly long-term risks. Some 80% of earnings before interest and tax (EBIT) from the Lotteries division – and a further 95% of EBIT from Wagering – is earned on licences with over 35 years to expiry (see Table 1).

| Licence | Expires |

|---|---|

| Race wagering licence - Qld | 2098 |

| Sports wagering licence - Qld | 2098 |

| Sports bookmaker licence - NT | 2020 |

| Major betting operations licence - SA | 2100 |

|

Inter-club linked gaming system licence - NSW

|

2017 |

|

Inter-hotel linked gaming system licence - NSW

|

2019 |

| Lotteries licence - Vic | 2018 |

| Lotteries licence - NSW | 2050 |

| Race and sports wagering licence - Tas | 2062 |

The Victorian lotteries licence will probably be the firecracker, as it needs to be renewed every 10 years. The next renewal is in 2018 and, for what it's worth, Deutsche Bank believes the winning bid is likely to be around the $250m mark – well above the $19m paid in 2007.

Because the Victorian government takes a big slice of revenue, the Victorian licence is the lowest margin lottery in Australia. That gives Tatts a slight advantage when bidding: as the incumbent, with existing infrastructure integrated across several states, Tatts is likely to be the lowest cost operator, meaning it can take the lowest margin work and still turn a profit. There's a good chance that the company will win the licence, even if it does have to pay up for it.

Wagering a long shot

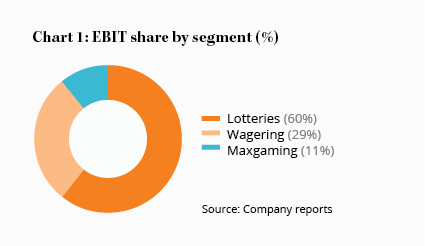

All up, we like the Lotteries division, which accounts for around 60% of EBIT. Wagering on the other hand – which contributes around 29% of EBIT – gives us the heebie jeebies.

Tatts' wagering operations encompass tote and fixed odds betting on horses, greyhounds and other sports in Queensland, South Australia, Tasmania and the Nothern Territory.

The trouble with wagering, though, is that it's in the opposite situation to that of the Lotteries division. Firstly, it isn't a monopoly – it's facing growing competition from online operators such as Betfair. Secondly, its network of TAB retail outlets puts it at a cost disadvantage, in the same way that, say, Dick Smith had a difficult time competing with online sellers like Amazon.

The difference is material: Betfair's business model means that punters only lose around 5% in commissions, compared to the 15–20% takeout at a typical TAB. Betfair almost invariably offers better odds than those you would receive on the track or at a physical outlet.

The difference is material: Betfair's business model means that punters only lose around 5% in commissions, compared to the 15–20% takeout at a typical TAB. Betfair almost invariably offers better odds than those you would receive on the track or at a physical outlet.

Still, while we consider Tatts' wagering business to have a losing business model over the long term, it has held up better than expected. Online sales increased 20% in the six months to December, though this wasn't enough to offset a decline at retail outlets. Total revenue for the Wagering division fell 4%, leading to a 17% fall in EBIT due to those pesky fixed cost storefronts and higher marketing expenses. The quicker Tatts moves to an online model, the better.

Valuation

We expect Wagering to continue to be the company's problem child, and the upcoming Victorian lottery licence renewal could add some extra volatility to the share price. But with plenty of free cash flow, a monopoly position and long licences, Tatts is still a business we would love to own at the right price.

Management expects net profit of between $255m and $265m for the 2016 financial year, putting the stock on a price-earnings ratio of 23. Given the historical precedent, we expect free cash flow to come in slightly ahead of net profit, putting the stock on a free cash flow yield of around 5.5–6.0%. The board intends to maintain a payout ratio of 90% of net profit, so you're also getting a fully-franked dividend yield of around 4.0%.

That's a fair valuation for a high-quality company. We're raising the Buy price from $3.00 to $3.50, which would put the stock on a free cash flow yield above 6.5%. We think that's quite conservative, but it's important to be mindful that the high fixed cost base of the Wagering business means any falls in revenue are amplified by the time they reach the bottom line.

However, we're also increasing our recommended Sell price from $5.00 to $6.50 to give the stock more leeway should Wagering continue to beat our expectations or Tatts win the Victorian licence at a decent price. HOLD.

Disclosure: The author owns shares in Paddy Power Betfair PLC.

Recommendation