Sirtex: The value of innovation

Recommendation

- {{x.value}}

{{ twilioFailed ? 'SMS Code Failed to Send…' : 'Enter verification code' }}

{{ completedStep1 ? 'Authentication & Security' : content.trialHeading.replace('{0}', user.FirstName) }}

{{ content.upgradeHeading.replace('{0}', user.FirstName) }}

The email address you entered is registered with InvestSMART

Please login to continue

We have sent you an email with the details of your registration.

Looks you are already a member. Please enter your password to proceed

{{ upgradeCTAText }}

Updating information

Please wait ...

Your membership to InvestSMART Group recently failed to renew.

Please make sure your payment details are up to date to continue your membership.

Having trouble renewing?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

You've recently updated your payment details.

It may take a few minutes to update your subscription details, during this time you will not be able to view locked content.

If you are still having trouble viewing content after 10 minutes, try logging out of your account and logging back in.

Still having trouble viewing content?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

Please click on the ACTIVATE button to activate your Intelligent Investor 15-day free trial

Please click on the ACTIVATE button to finalise your membership

Unsuccessful registration

Registration for this event is available only to Eureka Report members. View our membership page for more information.

Registration for this event is available only to Intelligent Investor members. View our membership page for more information.

- You are already registered for this event.

- This event is already full.

- Please select a quantity for at least one ticket.

- {{ i }}

Forgotten password

Please enter your email address below to request a new password

- Indepth analysis of ASX listed shares

- BUY, Hold and Sell Recommendations

- Ideas Lab

- Special Reports

- Alan Kohler’s Weekend Briefing

- Interviews with CEO’s & top influencers

- Money Cafe and Talking Finance

- Super Advice and Q&A with Ask Alan

Sirtex Medical is a one-product company, but whilst its liver cancer therapy is a very successful product, Sirtex's reliance on a single source of income makes it risky. When the future of SIR-Spheres was called into question early last year following a poor clinical trial result, the stock promptly fell 60%.

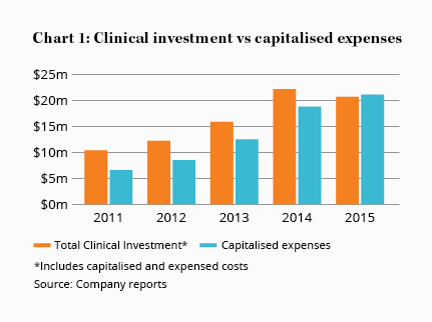

This point hasn't been lost on management. The company is ploughing a good 10% of revenue back into the business to fund research and development (R&D) and clinical studies to expand its product pipeline. Sirtex spent $20m on clinical investment in the 12 months to December, the bulk of which was to improve acceptance of SIR-Spheres among doctors.

But the company is also funding the development of new technologies that could help to treat brain cancer and eye disorders, including carbon cage nanoparticles (small stuff) and magnetic nanoparticles (attractive small stuff).

Key Points

-

New cancer treatment R&D programs

-

R&D leads to profits exceeding cash flow

-

Government funding cuts a risk; Hold

More interesting, perhaps, is Sirtex's development of a radioprotector, which makes healthy skin less sensitive to radiation. This could potentially reduce side effects for many different cancer therapies, and may eventually allow for expanded use of SIR-Spheres specifically.

Is R&D an expense or asset?

Before anyone gets too excited, though, R&D is inherently risky due to the long lead times, high upfront cost and uncertain outcomes. If any of Sirtex's new products do make it to commercialisation, it's still many years away. At such an early stage of development, these products are next to worthless from a company valuation perspective, so our focus is still on SIR-Spheres.

Furthermore, accounting for R&D is a fiddly business. Basic research costs are expensed through the income statement, which reduces net profit. However, if a company is confident that it will receive a financial benefit from incurring particular development costs, then those costs can be recorded as an intangible asset on the balance sheet. This is called ‘capitalising' expenses and Sirtex capitalises its development outlays and certain clinical trial costs.

The company currently has $75m of these mysterious expense-asset hybrids sitting on its balance sheet, with $20m of clinical investment expenses added to this figure in the 12 months to December. That's $20m Sirtex handed over to someone, but that bypassed the income statement. Were it to be fully expensed, net profit would be some 30% lower.

Now, we're not arguing that development and clinical trial costs should be fully expensed – in Sirtex's case, they will almost certainly produce an economic benefit and so probably are more akin to assets – but it needs to be taken into consideration when looking at what proportion of net profit can be distributed to shareholders. Of $49m in net profit, only $29m was free cash flow.

Time to market

All the research and microscope peering in the world means little without a sales team to get your product in front of customers. Sirtex has tripled its sales and marketing budget over the past four years to $40m for the six months to December (including a US$750,000 booth at the annual meeting for the American Society of Clinical Oncology).

Make no mistake: A $40m marketing budget is a huge sum for a company this size. As a proportion of revenue it's almost four times what CSL spends. Still, we think it's money well spent.

Make no mistake: A $40m marketing budget is a huge sum for a company this size. As a proportion of revenue it's almost four times what CSL spends. Still, we think it's money well spent.

Sirtex already has an approved and commercially viable product, yet management believes only 2% of the addressable market currently uses SIR-Spheres. Now's the time to shout from the rooftops, before competition intensifies. There's plenty of room for growth, and small increases in dose sales can have a big impact on profits.

The upfront investment in marketing reduces current profitability but, as dose sales grow, Sirtex will benefit from widening margins due to a large proportion of the company's expenses being fixed. Sirtex's operating margin has increased from 18% to 29% since 2011, and we expect profits to continue to grow faster than revenues as dose sales march upwards.

Growth continues

Sirtex achieved a 16% increase in dose sales for the year to June, compared to last year. Strong growth of 19% in the Americas was dragged down by growth of ‘only' 11% and 9% in Europe and Australia Pacific. The poor result was mainly due to: the late publication of clinical study results, which affected marketing; supply constraints in Asia; and less generous funding in European markets. We'll know more when the full-year results are released in August.

Management said the issues were mainly temporary – and, in any case, 9% growth isn't something to cry over – but they also underscore one of Sirtex's major risks: government funding.

When assessing most drug companies, the risk is usually whether or not the product will be successful. With full regulatory approval and commercialisation, that's no longer an issue for Sirtex. The question then becomes to what extent will physicians and patients endorse SIR-Spheres, and that largely comes down to competition and whether or not the product is subsidised.

Governments and insurers currently pay for the therapy in Australia, the US and several other countries, though their willingness to do so may decline as healthcare budgets become unwieldy. Using an expensive product to prolong the life of a terminally ill patient has an opportunity cost – and with SIR-Spheres priced at around US$16,000 a dose, that opportunity cost is significant. It isn't hard to imagine a company announcement at some future date saying that sales have declined due to cuts to government funding. You can manage these risks by locking in profits as the share price rises and by ensuring that your holding stays below our recommended portfolio limit of 3%.

It's too early to tell whether any of Sirtex's R&D programs will pay off, but with a clean balance sheet and $74m of net cash, profitable sales, and a large untapped market for SIR-Spheres, there's still every reason to believe Sirtex will be bigger and stronger five years from now. HOLD.