Reece: Three reasons

Recommendation

- {{x.value}}

{{ twilioFailed ? 'SMS Code Failed to Send…' : 'Enter verification code' }}

{{ completedStep1 ? 'Authentication & Security' : content.trialHeading.replace('{0}', user.FirstName) }}

{{ content.upgradeHeading.replace('{0}', user.FirstName) }}

The email address you entered is registered with InvestSMART

Please login to continue

We have sent you an email with the details of your registration.

Looks you are already a member. Please enter your password to proceed

{{ upgradeCTAText }}

Updating information

Please wait ...

Your membership to InvestSMART Group recently failed to renew.

Please make sure your payment details are up to date to continue your membership.

Having trouble renewing?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

You've recently updated your payment details.

It may take a few minutes to update your subscription details, during this time you will not be able to view locked content.

If you are still having trouble viewing content after 10 minutes, try logging out of your account and logging back in.

Still having trouble viewing content?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

Please click on the ACTIVATE button to activate your Intelligent Investor 15-day free trial

Please click on the ACTIVATE button to finalise your membership

Unsuccessful registration

Registration for this event is available only to Eureka Report members. View our membership page for more information.

Registration for this event is available only to Intelligent Investor members. View our membership page for more information.

- You are already registered for this event.

- This event is already full.

- Please select a quantity for at least one ticket.

- {{ i }}

Forgotten password

Please enter your email address below to request a new password

- Indepth analysis of ASX listed shares

- BUY, Hold and Sell Recommendations

- Ideas Lab

- Special Reports

- Alan Kohler’s Weekend Briefing

- Interviews with CEO’s & top influencers

- Money Cafe and Talking Finance

- Super Advice and Q&A with Ask Alan

What idiot would buy a plumbing supplies business near the peak of a housing boom? Well, this idiot, for one. We've waited a long time to recommend Reece which is, without question, one of Australia's best businesses. But why are we upgrading now?

You might think the timing peculiar. New dwelling commencements exceeded 220,000 in 2015, an Australian record and up 57% since 2009. That's widely considered to be a short-term peak. Reece will benefit for a while yet, as pipes and toilets are fitted to buildings near completion – sales will exceed $2,200m in the 2016 financial year, up almost 50% over the past three years – but surely there's a downturn on the way?

Key Points

-

Reece is a very high quality business

-

Upside from Actrol is significant

-

Housing downturn a key risk

Perhaps so, but picking cycles is harder than it looks. It's also much less important for high-calibre companies because they tend to suffer less than competitors during downturns. Indeed, Reece's 'wonderful business' status is the first of three reasons why the stock deserves an upgrade.

Reece dominates the plumbing supplies market, fending off competition from Tradelink, Bunnings and Mitre10. Its customers are mainly plumbers, who prefer not to cart the heavy materials around in their utes: an account with Reece allows them access to more than 100,000 items from almost 500 outlets around Australia.

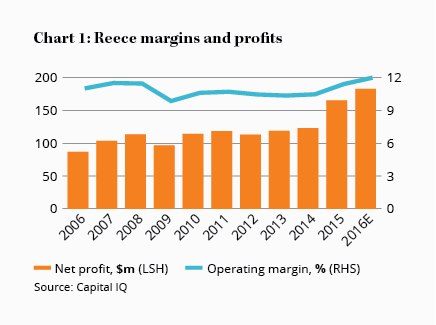

This mix of range, service, convenience and buying power enables Reece to earn margins consistently above 10% (see Chart 1). Margins of that magnitude are unusual for a wholesaler; they compare, for example, with Fletcher Building-owned Tradelink, the plumbing industry's poor cousin, whose sales have flat-lined for a decade and whose 2015 operating margin was just 2.2% (see Analytical Footnote 1 below).

Reece's high margins have helped it deliver a return on capital employed consistently above 20%, which means management can reinvest capital (very) profitably in the business – something that lower-margin wholesalers often find difficult. With the Wilson family controlling 67% of the company's stock, they manage Reece for ultra-long term performance and the results speak for themselves, with net profit more than doubling over the past decade.

Reasonable price

Of course, a great business with strong management is only useful if it's available at a reasonable price. In Reece's case, the value has improved while the share price has remained more or less stable. This is the second reason the stock is worth buying.

Reece's net profit should exceed $180m in 2016, up from $123m in 2014. The housing boom has certainly helped, as has the acquisition of Actrol (which we'll get to shortly). Yet the share price has barely budged between 2014 and today.

The reason is that the market looks forward – at least a little bit – and it's expecting the housing boom to ease. Reece now trades on a forecast 2016 price-earnings ratio of 19, its lowest for years. Similarly, the enterprise value to earnings before interest, tax, depreciation and amortisation (EV/EBITDA) multiple is 11.2 (see Table 1). These are inexpensive multiples – historically and absolutely – for a business of superb quality.

What's perhaps a little less attractive is Reece's free cash flow yield. Reece has always spent heavily on capital expenditure, including outlet refurbishments and openings, distribution centres (a new one has just opened in Perth) and technology investment. A 2016 forecast free cash flow yield of 3.5% is lower than we'd normally like but we can live with it given the business's quality.

You're probably thinking the earnings multiples will rise if profits suffer in a housing downturn. That's true, as Reece's profits fell in 2009 and then again in 2012 as the cycle ebbed. But neither year was a crushing blow – net profit in each year fell by 15% and 4% respectively.

Chronic undersupply

The recent housing boom has been the strongest for decades and yet Australia's housing market is widely considered to be in chronic undersupply; particularly so in markets such as New South Wales. Any downturn in housing construction or renovation activity won't necessarily be severe and Reece, diversified as it is across all states, should be reasonably well insulated.

Indeed, Reece might suffer less than expected because of largely unrecognised growth potential. This is the third reason for upgrading the stock – the company's potential to take market share in the heating, ventilation, air-conditioning and refrigeration industry (which goes by the acronym HVAC-R).

| $m | |

|---|---|

| Market capitalisation | 3,370 |

| Add share of net debt | 90 |

| Enterprise value (EV) | 3,460 |

| EBITDA (2016e) | 315 |

| EV/EBITDA (2016e) x | 11.0 |

| PER (2016e) x | 18.6 |

| Free cash flow yield (2016e) | 3.6% |

In January 2014 Reece acquired Actrol, the largest independent wholesaler to the HVAC-R industry. Actrol is similar to Reece's existing plumbing supplies business, in that it services air conditioning and refrigeration tradesmen with 80-odd outlets throughout Australia.

The HVAC-R wholesaling market is much more fragmented than plumbing supplies. Actrol's major competitor is Heatcraft, which also operates as a de facto distributor for its US parent and equipment manufacturer Lennox International. Most other HVAC-R wholesaling competitors are foreign-owned, including Totaline and Beijer Ref, which has been acquiring small competitors in Australia and New Zealand.

Secret squirrel

Reece's management hasn't provided a lot of detail about its plans for Actrol. Indeed, all it has really said is that it is 'steadily building a unique and compelling offer for HVAC and refrigeration plumbers'. So what does this mean?

Well, Reece can bring professionalism and capital, as well as independence from manufacturers, to the HVAC-R industry. The aim will be to take market share from other players, just as it has done in plumbing supplies. Acquisitions of competitors are possible but, even without them, the sales upside looks significant. In the long term Reece will presumably colocate Reece and Actrol outlets.

The fragmentation of the HVAC-R industry, potential counter-attacks from foreign-owned wholesalers and the multitude of manufacturers means Actrol is in a weaker competitive position in HVAC-R than Reece is in plumbing supplies. But if you want a management team to capitalise on an opportunity, then Reece's is as good as any you'll find.

Profit up, price down

Since our last full review, in Reece: Result 2015, the company's profit has jumped sharply and the potential benefits from the Actrol acquisition have become clearer. And yet the share price has fallen slightly. While there's a risk the housing downturn will hit profitability and the share price, we think the market is overestimating that risk and underestimating the potential upside from Actrol.

We're therefore lifting our Buy price to $36 a share and our Sell price to $55. Our maximum portfolio weighting remains the same at 5% although, as usual, we suggest you buy in stages.

Reece shares are near their all-time high. So the stock is not a standout buy, especially given where we are in the housing cycle and the relatively low free cash flow yield. Even so, this is the very definition of a wonderful business at a fair price. We're upgrading Reece to BUY up to $36.

Note: Reece is an illiquid stock. It might take a while to build a position and we recommend patience.

Analytical footnote (1): Reece's margins are higher than Tradelink's partly because the former owns $342m of property. Tradelink's margins must necessarily be lower because its cost structure includes a greater proportion of rent. Reece's property ownership is of course a good thing – and a source of competitive advantage – but strictly speaking we're not comparing like-for-like.

Recommendation