Paul Moore stands his ground

Recommendation

- {{x.value}}

{{ twilioFailed ? 'SMS Code Failed to Send…' : 'Enter verification code' }}

{{ completedStep1 ? 'Authentication & Security' : content.trialHeading.replace('{0}', user.FirstName) }}

{{ content.upgradeHeading.replace('{0}', user.FirstName) }}

The email address you entered is registered with InvestSMART

Please login to continue

We have sent you an email with the details of your registration.

Looks you are already a member. Please enter your password to proceed

{{ upgradeCTAText }}

Updating information

Please wait ...

Your membership to InvestSMART Group recently failed to renew.

Please make sure your payment details are up to date to continue your membership.

Having trouble renewing?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

You've recently updated your payment details.

It may take a few minutes to update your subscription details, during this time you will not be able to view locked content.

If you are still having trouble viewing content after 10 minutes, try logging out of your account and logging back in.

Still having trouble viewing content?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

Please click on the ACTIVATE button to activate your Intelligent Investor 15-day free trial

Please click on the ACTIVATE button to finalise your membership

Unsuccessful registration

Registration for this event is available only to Eureka Report members. View our membership page for more information.

Registration for this event is available only to Intelligent Investor members. View our membership page for more information.

- You are already registered for this event.

- This event is already full.

- Please select a quantity for at least one ticket.

- {{ i }}

Forgotten password

Please enter your email address below to request a new password

- Indepth analysis of ASX listed shares

- BUY, Hold and Sell Recommendations

- Ideas Lab

- Special Reports

- Alan Kohler’s Weekend Briefing

- Interviews with CEO’s & top influencers

- Money Cafe and Talking Finance

- Super Advice and Q&A with Ask Alan

Paul Moore, portfolio manager of PM Capital Global Opportunities Fund (PGF), noted during his company's recent annual roadshow: ‘When it comes to investing, there is no safety in numbers; you have to be doing something different from what other investors are doing.'

This is easier said than done, of course. As Moore continued: ‘You must be able to stand your ground under intense pressure and ridicule.'

After PGF's portfolio fell 11.6% (ignoring currency gains of 2.4%) in 2016, these words have never been more true. Since inception, PGF's portfolio has returned 15.7% pre-tax compared to the 31.9% return of its benchmark, the MSCI World Net Total Return Index.

Bad banks

Much of the damage in 2016 was due to PGF's large exposure to financials and in particular, foreign banks – approximately 57% of its portfolio at 31 July 2016 consisted of financials, with 21% being foreign banks.

When we upgraded PGF in January 2016, part of the attraction was its exposure to banks in the United States, Europe and the United Kingdom, which were much cheaper than their Australian counterparts such as Westpac and Commonwealth Bank. Along with interest rates likely rising over the medium-to-long term and credit growth as their underlying economies expanded, these banks were likely to record increasing earnings and dividends in coming years.

In the meantime, however, the Brexit result hit the share prices of both European and US banks. Investors reasoned that worldwide interest rates would now be lower for even longer – thus penalising banks' net interest margins – while British and European economic growth would be reduced by Brexit and its direct and indirect impacts on the EU.

Among the banks in PGF's portfolio, British-based Lloyds Banking Group declined 38% in 2016, Bank of America fell 23% and ING Groep declined 39%. All three are in PGF's top ten holdings and falls in Sterling have made matters worse (PGF also owns shares in Barclays).

However, as colleague Jon Mills noted recently, we think the long-term impact of Brexit on both the British and European economies won't be as bad as many have predicted. And since then, much of the initial shock has dissipated: since the end of 2016, Bank of America has recovered its post-Brexit losses and ING Groep is now only a shade below its pre-Brexit share price.

Paul Moore expects the UK and other European banks to follow suit but thinks it will require time and patience. We agree.

High conviction contrarian

Patience and a long-term perspective are necessities if you're investing with Paul Moore. Being a contrarian with high conviction (that is, a concentrated portfolio) has been his trademark since he founded PM Capital in 1998. This investment approach often leads to high volatility in investor returns over the short to medium term as well as periods of underperformance, so it's not an approach that many investors will be comfortable with.

Still, it has been highly successful: over the past eighteen years, PM Capital's Global Companies Fund – which PGF aims to mimic – has returned more than double its benchmark. This is despite its unit value falling 19% since its high point in July 2015, significantly underperforming the 4% decline in its benchmark during this period.

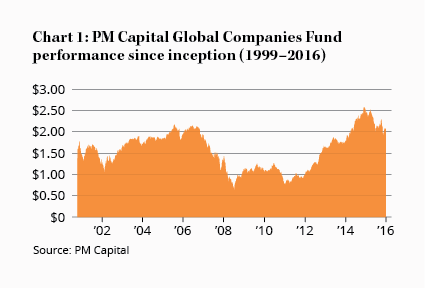

The Global Companies Fund's historical unit prices are disclosed on PM Capital's website and, as you can see in Chart 1, double digit declines have been quite common since inception in 1998. Yet there have also been large increases, with the fund returning 27% in 2004 and a whopping 63% in 2013, helping account for the outperformance compared to its benchmark since inception.

Still a Buy

Underlying our original investment case for PGF was its then 16% discount compared to its post-tax NTA, which we felt provided satisfactory compensation for the management fees charged by PM Capital. The share price has fallen by 5% since then but so has its post-tax NTA so you can still purchase PGF at a 13% discount to its underlying holdings.

Although it is difficult and you risk ‘ridicule', you should try to take advantage of periods of volatility rather than being affected by them. We think this is one such opportunity.

We'll leave the last word to Paul Moore who summed up our thoughts exactly in the 2016 annual report: ‘If our investment propositions do in fact meet our long term investment objectives, I find it intriguing that I can obtain exposure to the very same investments at a significant discount to their public market values via an investment in PGF'. BUY