Macro Investing: The coming iron ore glut

- {{x.value}}

{{ twilioFailed ? 'SMS Code Failed to Send…' : 'Enter verification code' }}

{{ completedStep1 ? 'Authentication & Security' : content.trialHeading.replace('{0}', user.FirstName) }}

{{ content.upgradeHeading.replace('{0}', user.FirstName) }}

The email address you entered is registered with InvestSMART

Please login to continue

We have sent you an email with the details of your registration.

Looks you are already a member. Please enter your password to proceed

{{ upgradeCTAText }}

Updating information

Please wait ...

Your membership to InvestSMART Group recently failed to renew.

Please make sure your payment details are up to date to continue your membership.

Having trouble renewing?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

You've recently updated your payment details.

It may take a few minutes to update your subscription details, during this time you will not be able to view locked content.

If you are still having trouble viewing content after 10 minutes, try logging out of your account and logging back in.

Still having trouble viewing content?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

Please click on the ACTIVATE button to activate your Intelligent Investor 15-day free trial

Please click on the ACTIVATE button to finalise your membership

Unsuccessful registration

Registration for this event is available only to Eureka Report members. View our membership page for more information.

Registration for this event is available only to Intelligent Investor members. View our membership page for more information.

- You are already registered for this event.

- This event is already full.

- Please select a quantity for at least one ticket.

- {{ i }}

Forgotten password

Please enter your email address below to request a new password

- Indepth analysis of ASX listed shares

- BUY, Hold and Sell Recommendations

- Ideas Lab

- Special Reports

- Alan Kohler’s Weekend Briefing

- Interviews with CEO’s & top influencers

- Money Cafe and Talking Finance

- Super Advice and Q&A with Ask Alan

Key Points

- Iron ore expansion plans far exceed demand growth

- Price falls will lead to market share gains for low cost producers

- Investors should avoid all but the majors

In early 2003, Australian iron ore was trading at $12.05 per tonne. Relations between Australia and the dominant buyer of iron ore, Japan, were cordial. Each year a meeting took place between miners and steel mills to negotiate an annual contract price for bulk iron ore shipments in the year ahead.

Against the backdrop of gleaming Tokyo skyscrapers, perhaps tea was shared during gentlemanly discussions. Either way, BHP Billiton and Rio Tinto made handsome profits.

With the exception of handsome profits, all of that was about to change. Within five years, the Japanese would be forgotten. Iron ore prices would be 500% higher, on their way to an astonishing 1,500% rise.

Negotiations between miners and Asian clients are now so rancorous that mining employees are jailed, special envoys fly between nations on crisis missions and the integrity of the contract system has disintegrated.

Common element

How did the planet’s fifth most common element, constituting 5% of the earth’s crust, realign loyalties and catapult Australia into an era of gold rush-like riches?

In a word: China. In 2003, China accelerated its urbanisation program, liberalising the private sector, accepting foreign capital and fixing its currency to the $US at a cheap exchange rate. That unleashed an investment deluge. The 1.3bn people that had been excluded from the global middle class for generations were invited back in, en masse. Iron ore, a key ingredient in steel production, was central to that program.

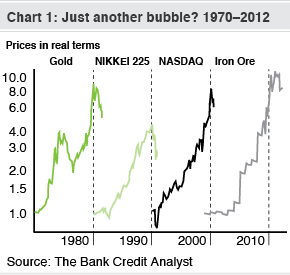

After a 1,500% price rise in eight years to 2011, for a commodity that’s abundant, how can this be anything but a bubble?

Global investment research house BCA seems to see it that way (see Chart 1), charting the iron ore price against gold and major stockmarket indicies.

And there is some evidence to support this view. In any commodities bubble one might expect to see large inventories being stockpiled by speculators waiting for higher prices. After the global financial crisis, that did happen in China; port inventories tripled from 35m tonnes in 2008 to 100m tonnes in 2011.

But the opposing case is stronger. The growing stockpiles reflected increased port capacity and high steel production growth. As prices have corrected in the past year or so, Chinese port stocks have fallen back to 76m tonnes.

Speculating in iron ore is no simple matter, either. The derivatives market for iron ore doesn’t offer the breadth of swap, futures and options that exist for, say, oil. But perhaps the most compelling argument against an iron ore bubble is that basic economics can explain the price rise.

Demand shock

A sudden and unexpected rise in demand is called a ‘demand shock’. Markets that cannot readily respond to new demand are called ‘inelastic’. Commodities, capital intensive and with long lead times, typify such markets. When a demand shock hits an inelastic market the supply/demand curve steepens and prices rocket. Iron ore is a textbook case, explored at length by the Reserve Bank of Australia here and here.

In the first of three stages, prices rise. In the second, miners invest heavily in new supply to capture greater profits from the price rise. Finally, as new mines begin to ship greater volumes, prices fall.

This is the so-called ‘three staged’ mining boom, but don’t feel reassured. Theories of demand shocks in inelastic markets predict one more outcome: volatility.

In the early phases of the mining boom, Australian miners were sceptical of the sustainability of Chinese demand and moved only slowly to expand supply. Later, convinced of the boom’s durability, they aggressively invested in supply. Australian miners shipped about 270m tonnes of iron ore in 2005.

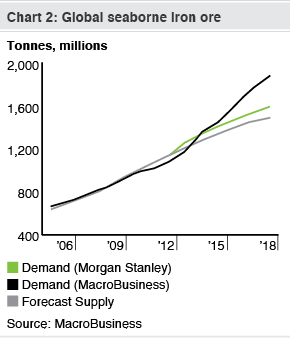

Australian capacity on current plans is forecast by Morgan Stanley to reach 950m tonnes by 2018. And that is only in Australia. Global seaborne iron ore shipments were 650m tonnes in 2005 and are projected to rise to a capacity of 1,880m tonnes.

Expansion

In short, current mining expansion plans have dramatically overshot demand growth because China has suddenly changed its steel consumption pattern from growth of 8-10% per year to just 2-3%.

If all current expansion plans proceed, the iron ore market will suffer a glut of 300m tonnes per annum by 2018. According to Morgan Stanley, that begins in earnest in 2015 at 100m tonnes. Macrobusiness believes Chinese growth will slow even earlier and that the iron ore glut will arrive at the end of this year.

If Chinese demand growth remains on a lower track than earlier assumed, a 300m tonne iron glut won’t eventuate. Instead, current plans will be wound back as the iron ore price falls.

But the 2013-2016 Australian capacity expansion is already committed and much of it is under construction. Rio Tinto, BHP and Fortescue are building like mad. Australian miners will account for some 250m tonnes of the planned 300m tonnes of new seaborne capacity coming online in the next three years.

How should investors plan for this? High cost producers are in much greater danger of losing market share as oversupply comes on stream, lowering prices.

Low cost producers

BHP and Rio Tinto can produce iron ore at a cash cost of around $40 per tonne. They’re far more likely to win the market share battle as prices fall. The trouble is that Rio faces huge exposure to the ore price. It generates about 90% of its profits, which means any substantial fall in the iron ore price is likely to outpace volume growth, producing lower earnings.

BHP is better placed. In 2012 iron ore contributed 50% of earnings (and 60% if coking coal is included as a twin commodity, largely due to the huge margins it was making. [Look out for a review of BHP Billiton tomorrow].

Fortescue, with a delivery cost of around $80 per tonne, has hung its future on the notion that it can displace current Chinese suppliers producing at $100-$120 per tonne and establish a ‘price floor’ around $120 per tonne. Meanwhile, the new iron futures market in Singapore is already pricing iron ore at $97 in 2016.

Estimates of Chinese costs of production are also falling over time, and that country’s government has also shown an appetite for protecting local production for strategic reasons. As last year’s price plunge showed, there are doubts that iron ore has a ‘price floor’ in the $120 range as Fortescue argues.

All of this adds up to a market that is in for a lot more volatility, in price and corporate activity. As new supply arrives, the iron ore price will probably fall to new lows and the highest marginal cost of production players will be knocked over.

The major producers will grow market share and ultimately be in a strong position to pick off the marginal players and consolidate production. Along with Brazilian rival Vale, BHP and Rio account for 80% of the traded iron ore market, so BHP and Rio shareholders need to play a long game and expect volatility. Once the market stabilises and adjusts to the new reality, there’s a good chance they’ll be able to once again exert pricing power.

David Llewellyn-Smith is the founding publisher and former global economy editor of The Diplomat magazine, Asia Pacific’s leading geo-politics and economics website. He is also the co-author of The Great Crash of 2008 with Ross Garnaut and a regular economics and markets contributor for Fairfax and the ABC. David is the editor-in-chief and publisher of MacroBusiness.