Is Smartgroup a smart buy?

Recommendation

- {{x.value}}

{{ twilioFailed ? 'SMS Code Failed to Send…' : 'Enter verification code' }}

{{ completedStep1 ? 'Authentication & Security' : content.trialHeading.replace('{0}', user.FirstName) }}

{{ content.upgradeHeading.replace('{0}', user.FirstName) }}

The email address you entered is registered with InvestSMART

Please login to continue

We have sent you an email with the details of your registration.

Looks you are already a member. Please enter your password to proceed

{{ upgradeCTAText }}

Updating information

Please wait ...

Your membership to InvestSMART Group recently failed to renew.

Please make sure your payment details are up to date to continue your membership.

Having trouble renewing?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

You've recently updated your payment details.

It may take a few minutes to update your subscription details, during this time you will not be able to view locked content.

If you are still having trouble viewing content after 10 minutes, try logging out of your account and logging back in.

Still having trouble viewing content?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

Please click on the ACTIVATE button to activate your Intelligent Investor 15-day free trial

Please click on the ACTIVATE button to finalise your membership

Unsuccessful registration

Registration for this event is available only to Eureka Report members. View our membership page for more information.

Registration for this event is available only to Intelligent Investor members. View our membership page for more information.

- You are already registered for this event.

- This event is already full.

- Please select a quantity for at least one ticket.

- {{ i }}

Forgotten password

Please enter your email address below to request a new password

- Indepth analysis of ASX listed shares

- BUY, Hold and Sell Recommendations

- Ideas Lab

- Special Reports

- Alan Kohler’s Weekend Briefing

- Interviews with CEO’s & top influencers

- Money Cafe and Talking Finance

- Super Advice and Q&A with Ask Alan

When searching for Peter Lynch's famed 10-baggers, perhaps you think of rapidly growing technology or biotechnology companies with a nifty new product that can help millions around the world. You certainly don't imagine a salary packaging and novated lease company like Smartgroup.

Chief executive Deven Billimoria joined the company in 2000 and became CEO in 2002. More recently, the stock price has increased six-fold while the company's paid a growing stream of dividends since the company listed at $1.50 in July 2014.

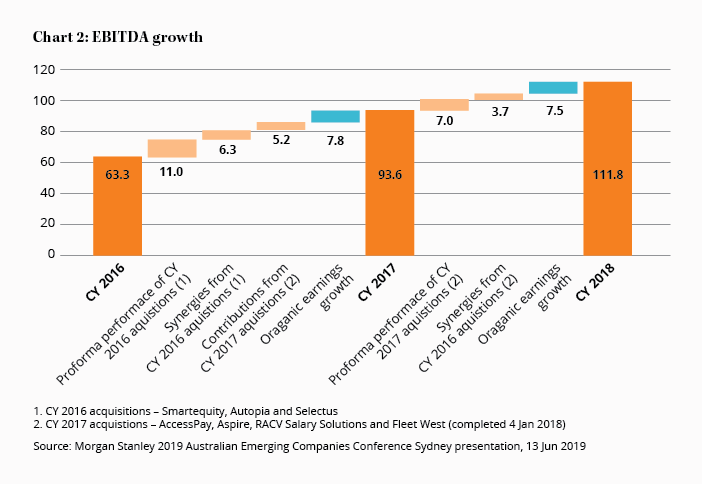

While research suggests more than 70% of acquisitions fail to add value, Billimoria has quietly turned them into an art form by maintaining a return on equity above 23%. Despite shares on issue increasing 27% since 2015, earnings per share have increased 150%.

Key Points

-

Remarkable track record

-

Owner operator

-

4.7% fully franked dividend yield

This impressive track record sent the share price to a record of almost $13 last August, increasing the price-to-earnings ratio (PER) to 26. Soon after, on 16 October, the company announced that Billimoria was taking long service leave. Over the following six months, the share price steadily dropped below $8, suggesting that he wasn't coming back.

Billimoria returned, but any excitement was dulled by his sale of 1.1m shares at $7.60. Thankfully, his remaining holdings mean he still has almost 30 million reasons to stay motivated.

Tougher economic environment

The share price has recently recovered to around $9, but that's a long way from the highs of 2018. Let's dig into the business to find out why.

Salary packaging and novated leases are chiefly used by charities and public employers to increase staff remuneration by reducing their tax. Changes to the tax rules will always be the biggest risk to the industry.

But we don't believe either side of politics has the stomach for reducing the after-tax wages of some of our nation's lowest-paid staff like teachers and nurses. Particularly since Scott Morrison has promised Australians that their house prices won't fall, and wage growth remains anemic despite pygmy interest rates.

Smartgroup's revenue should be fairly stable, as we need nurses and teachers in every economic environment. But revenues aren't totally immune to changes in the economy.

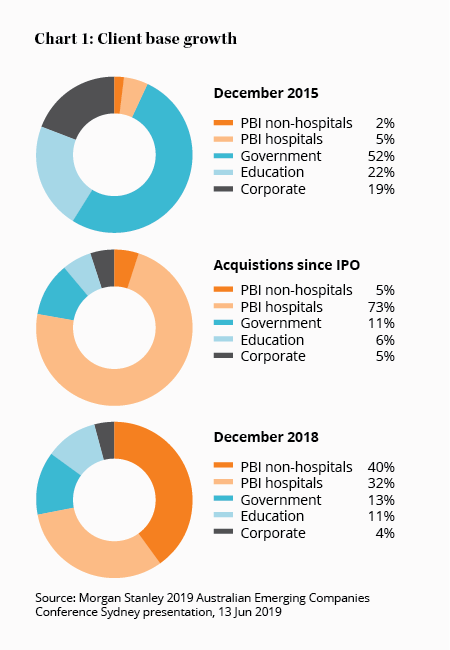

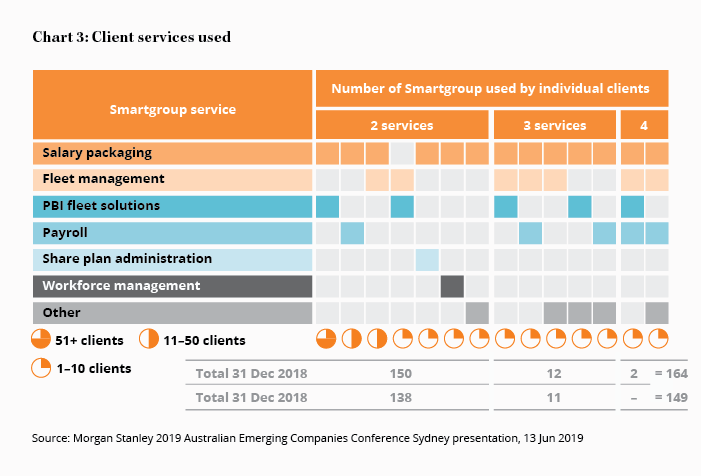

Smartgroup's best customers are employees that buy new cars with add-ons such as finance and warranties. Smartgroup's best clients - those charities and public employers - are those that don't just offer salary packaging and leasing to their staff, but also purchase fleet management and payroll services. In the year to 30 June, 164 clients use two or more services, up 10% from a year earlier. This is great for profit margins.

On the flipside, more people have recently been saving money by refinancing old cars rather than buying new ones, and new car buyers are buying cheaper cars. A further $2m of profit has been lost from extended warranty services as most new cars now come with a 5-year warranty.

Still, Billimoria has done a good job maintaining novated lease volumes and margins despite the headwinds. Processing more applications online has saved money and made life easier for lessees.

Slower growth ahead

With Smartgroup now the same size as its biggest rival McMillan Shakespeare, the opportunity for large acquisitions has reduced. While that means future earnings growth won't resemble the V8 speeds of the past, the company has recently made a couple of tuck-in acquisitions, which should be the norm. Expect a capital raising if Billimoria spots a big opportunity during a recession.

Billimoria's reinvestment of the company's profits has been exceptional, even if shares on issue have increased by 50% since listing. Special dividends, such as the 20 cents per share declared in April, reflects the company's excellent financial position and management's shareholder friendliness.

We believe the stock can produce a greater than 10% annualised return with a starting 4.7% fully franked dividend yield. On a PER of 16 excluding amortisation, Smartgroup is suitable for up to 3% of a well-diversified portfolio. The 5% portfolio weight leaves room for the position to grow or to buy more shares at lower prices. A weak result in August could also create a better buying opportunity. BUY.

Note: The Intelligent Investor Ethical, Equity Growth and Equity Income funds own shares in Smartgroup.

Note: We're buying 5,130 shares in Smartgroup at $8.98 for our Model Growth Portfolio and 4,935 shares for our Model Income Portfolio at $8.98, amounting to weightings of about 3%.

Recommendation