Flight Centre beats expectations

Recommendation

- {{x.value}}

{{ twilioFailed ? 'SMS Code Failed to Send…' : 'Enter verification code' }}

{{ completedStep1 ? 'Authentication & Security' : content.trialHeading.replace('{0}', user.FirstName) }}

{{ content.upgradeHeading.replace('{0}', user.FirstName) }}

The email address you entered is registered with InvestSMART

Please login to continue

We have sent you an email with the details of your registration.

Looks you are already a member. Please enter your password to proceed

{{ upgradeCTAText }}

Updating information

Please wait ...

Your membership to InvestSMART Group recently failed to renew.

Please make sure your payment details are up to date to continue your membership.

Having trouble renewing?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

You've recently updated your payment details.

It may take a few minutes to update your subscription details, during this time you will not be able to view locked content.

If you are still having trouble viewing content after 10 minutes, try logging out of your account and logging back in.

Still having trouble viewing content?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

Please click on the ACTIVATE button to activate your Intelligent Investor 15-day free trial

Please click on the ACTIVATE button to finalise your membership

Unsuccessful registration

Registration for this event is available only to Eureka Report members. View our membership page for more information.

Registration for this event is available only to Intelligent Investor members. View our membership page for more information.

- You are already registered for this event.

- This event is already full.

- Please select a quantity for at least one ticket.

- {{ i }}

Forgotten password

Please enter your email address below to request a new password

- Indepth analysis of ASX listed shares

- BUY, Hold and Sell Recommendations

- Ideas Lab

- Special Reports

- Alan Kohler’s Weekend Briefing

- Interviews with CEO’s & top influencers

- Money Cafe and Talking Finance

- Super Advice and Q&A with Ask Alan

Flight Centre has surprised everyone – including us – by pre-announcing a bullish second half result. After a weak first half result, where underlying net profit fell 26%, the second half of 2017 will actually be a little stronger than the second half of 2016.

Altogether it implies earnings per share will be around $2.25 in the 2017 financial year, a far cry from the $2.00 to $2.10 we'd expected this past year. The announcement means the company will deliver close to the top end of management's guidance. We'd been prepared for a cyclical recovery (see Is Flight Centre the next JB Hi-Fi?), but not quite this soon.

In truth, it's partly because of a rising tide. Second-ranked travel agency group Helloworld reported ‘solid' total transaction value (TTV) and ‘very strong trading in the March quarter' a few months back. After concerns that Flight Centre might have trouble making $20bn in TTV this year, the company yesterday confirmed it would indeed meet that target.

Key Points

-

Flight Centre to meet upper end of guidance

-

Strong results in major markets

-

Strategic shift worth watching

Lower airfares seem to have stimulated demand in Australia, with Flight Centre also confirming that stronger international volumes had more than offset weaker pricing. Airfare deflation moderated over the period, as expected, after a 7% decline in the first half.

Work in progress

The recovery accelerated as the half progressed. But it was especially pleasing to see that management has taken action to improve performance rather than simply relying on external factors to swing back in the company's favour. Management has focused on improving sales productivity and controlling costs over the past year, and we think this is a work-in-progress. The benefits should keep flowing into 2018.

The good news wasn't confined to Australia. New Zealand will report a record profit in 2017, as will the USA. The UK will report a record profit in local currency, although the weak pound means it won't be as impressive in Australian dollars. The Canadian division also seems to be turning around, although Asia will take a little longer. The potential growth from Flight Centre's international operations remains under-appreciated in our view (see Flight Centre's ongoing evolution from October 2015).

So far, so impressive. But, if you're a shareholder, you should be aware that there's a significant strategic shift underway. Management announced in March that offering ‘in-destination travel experiences' would become the company's third major pillar alongside its corporate and leisure travel businesses. Yesterday's profit upgrade also focused on Flight Centre's intention to expand in this area in 2018. You should expect growth initiatives and perhaps acquisitions of so-called ‘destination management companies'.

So what exactly are ‘in-destination' experiences? Well, they include travel products such as tours or even hotels. In fact, Flight Centre specifically flagged expansion into hotel management ‘in some key markets'.

Flight Centre already operates several touring businesses such as Top Deck, Back Roads and Buffalo Tours but running your own tours and hotels is a very different skill set to selling the flights and hotels of other companies. In fact, it was over-capacity (read: poor management) in the British touring business that partly contributed to weak first half earnings.

Funnel web

Flight Centre presumably wants to become a ‘destination management company' partly because it can then funnel travellers into its own products. This might help address weaknesses in Flight Centre's hotel offer, but we're not convinced ‘vertical integration', as it's known, works well in the travel industry. Travellers might resent agents pushing them towards particular products given the trend towards more personalised experiences.

Of course, Flight Centre's management isn't silly. Far from it. We're prepared to give it the benefit of the doubt but how this ‘third pillar' evolves is something we'll watch carefully.

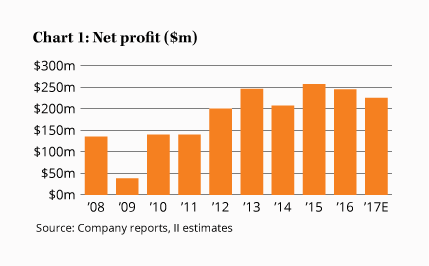

Whatever happens with future diversification, the fact remains that Flight Centre has exceeded our – and the market's – expectations for 2017. Hopefully this shouldn't be too much of a surprise to shareholders – it's always been a great business, despite the well-recognised threats from online competition. As Chart 1 shows, the company's profitability has generally been much more stable than the share price.

Fears of lower earnings – and the threat from online competition – have occasionally enabled us to buy the stock cheaply. With Flight Centre's share price up 25% since we downgraded to Hold in May and 36% higher than our initial upgrade last November, that opportunity has now passed.

Flight Centre's is business proving more resilient than even we expected and we're upgrading our price guide. Our Buy price moves up to $35 and our Sell price to $55. With the stock well above $40, that means our recommendation stays at HOLD.

Note: The Intelligent Investor Growth and Equity Income portfolios own shares in Flight Centre. You can find out about investing directly in Intelligent Investor and InvestSMART portfolios by clicking here.

Recommendation