CSL solves chicken and egg problem

Recommendation

- {{x.value}}

{{ twilioFailed ? 'SMS Code Failed to Send…' : 'Enter verification code' }}

{{ completedStep1 ? 'Authentication & Security' : content.trialHeading.replace('{0}', user.FirstName) }}

{{ content.upgradeHeading.replace('{0}', user.FirstName) }}

The email address you entered is registered with InvestSMART

Please login to continue

We have sent you an email with the details of your registration.

Looks you are already a member. Please enter your password to proceed

{{ upgradeCTAText }}

Updating information

Please wait ...

Your membership to InvestSMART Group recently failed to renew.

Please make sure your payment details are up to date to continue your membership.

Having trouble renewing?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

You've recently updated your payment details.

It may take a few minutes to update your subscription details, during this time you will not be able to view locked content.

If you are still having trouble viewing content after 10 minutes, try logging out of your account and logging back in.

Still having trouble viewing content?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

Please click on the ACTIVATE button to activate your Intelligent Investor 15-day free trial

Please click on the ACTIVATE button to finalise your membership

Unsuccessful registration

Registration for this event is available only to Eureka Report members. View our membership page for more information.

Registration for this event is available only to Intelligent Investor members. View our membership page for more information.

- You are already registered for this event.

- This event is already full.

- Please select a quantity for at least one ticket.

- {{ i }}

Forgotten password

Please enter your email address below to request a new password

- Indepth analysis of ASX listed shares

- BUY, Hold and Sell Recommendations

- Ideas Lab

- Special Reports

- Alan Kohler’s Weekend Briefing

- Interviews with CEO’s & top influencers

- Money Cafe and Talking Finance

- Super Advice and Q&A with Ask Alan

In early 2009, a woman died of the flu in eastern China. Although tragic for her and her family, particularly in light of her being only 27 years old, there was nothing particularly unusual in that. This time, though, was different. The virus that killed her was the H5N1 bird flu virus and, although millions of chickens are infected with the virus every year, it had rarely been transmitted to humans. Following this case, however, the World Health Organisation warned that the virus had become highly contagious and could become a global pandemic – a terrifying prospect given that the mortality rate for human cases of H5N1 is 60%.

All eyes turned to CSL and the world's other large vaccine makers, including GlaxoSmithKline and Sanofi Pasteur. CSL has had an H5N1 vaccine approved since 2008, but as flu viruses continually mutate the stock quickly goes out of date.

All of its H5N1 vaccines, like the vast majority of flu vaccines, are produced by injecting virus strains into chicken eggs, where they're allowed to replicate before being inactivated and the antigen purified.

Key Points

-

Seqirus is No. 2 global player

-

Quadrivalent vaccine shows potential

-

Holly Springs plant offers temporary competitive advantage

Each dose of vaccine requires one egg. CSL buys around 50 million eggs each year which, placed end to end, would apparently be enough to line the highways between Sydney and Uluru, via Adelaide (let's not try it).

With this in mind, egg-based vaccine production has a major drawback, particularly in the case of bird flu: if an outbreak reaches pandemic proportions, chicken flocks could be decimated and the supply of eggs might decline right when they're needed most. CSL literally has a chicken and egg problem.

Introducing Seqirus

In July 2015, CSL bought the influenza vaccine operations of Swiss healthcare behemoth Novartis for US$275m. The operations were combined with CSL's own vaccine division, bioCSL, and renamed Seqirus. CSL is now the second-largest player in the US$4 billion flu vaccine industry.

The Novartis flu business was a financial disaster as we'll explain later, but it did have a major selling point: it was the first and only vaccine manufacturer at the time with two methods of production.

The business uses traditional egg-based processing for seasonal and pandemic vaccines, but it can also produce vaccines by propagating the virus in cell cultures using a state-of-the-art facility in Holly Springs, in the US state of North Carolina.

Cell culture manufacturing has some significant advantages over egg-based production. The obvious one is that it doesn't rely on eggs, and thus eliminates supply risk during a bird flu pandemic.

A further benefit is that antibiotics aren't necessary during the production process, which is the case for egg-based manufacturing. The vaccines are therefore free of impurities and reduce the risk of reaction for people allergic to eggs.

Best of all, though, the Holly Springs site, which opened in 2010, is the largest cell culture-based flu vaccine facility in the world and has been designed for rapid scale-up during a crisis. Cell culture-based vaccines have shorter production times and can be expanded quickly on short notice, compared to the long lead-time necessary to procure millions of eggs. This one plant could produce enough vaccine for half the US population within six months of the start of a pandemic.

Seasonal vaccines

While pandemics can lead to rapid surges in sales, seasonal flu vaccines are Seqirus's bread and butter.

And here, competition is cut-throat. Sanofi Pasteur is the largest producer, supplying around 65 million doses a year, followed by Seqirus, which supplies around 50 million, and GlaxoSmithKline, at around 35 million.

This is where the Novartis acquisition will really make its mark. In addition to its pandemic response capability, Holly Springs manufactures the first cell culture-based seasonal flu vaccine, known as Flucelvax, with capacity for 50 million doses.

Flu vaccines are unique because the virus they are trying to protect against is constantly mutating. At the beginning of every flu season, the World Health Organisation has to assess what strains pose the greatest risk and supplies the right seed viruses to manufacturers. They then have a six-month window to develop a vaccine and begin production.

The first to market has a significant advantage as pharmacies, clinics and other customers like to buy in bulk early in the season. CSL's cell culture-based manufacturing can cut months from production time, making it highly competitive, especially given the large manufacturing capacity. It's worth noting, however, that other manufacturers are building their own cell-based capability, with two FDA-approved vaccines already on the market in addition to Seqirus's Flucelvax (Preflucel and Celvapan by Baxter).

But Seqirus has a potential trump card up its sleeve. Seasonal flu vaccines have traditionally been ‘trivalent', which means they contain three flu strains: an H1N1, an H3N2 and one type B strain.

But Seqirus has a potential trump card up its sleeve. Seasonal flu vaccines have traditionally been ‘trivalent', which means they contain three flu strains: an H1N1, an H3N2 and one type B strain.

This has its drawbacks, though, because if the World Health Organisation chooses the wrong strains for the current flu season, the vaccine is ineffective. And the hit rate for the B strain hasn't been great – WHO fails to predict the dominant circulating B strain around half the time.

Seqirus, however, has a cell culture-based quadrivalent vaccine (one with two B strains, as well as the two A strains) that has made it through Phase III clinical trials and is awaiting regulatory approval.

Assuming it is approved, CSL will have a seasonal flu vaccine that offers protection against four strains of influenza, rather than three. The added protection adds pricing power – quadrivalent vaccines like GlaxoSmithKline's Fluarix and Sanofi's Fluzone cost $16.82 and $16.62 a dose, compared to Seqirus's trivalent Fluvirin, which costs $14.41 and is the cheapest on the market.

Seqirus's quadrivalent vaccine would be competitive from a strain protection standpoint and likely be the first to market each year given the faster cell culture-based production method. If approved, we expect it to take market share.

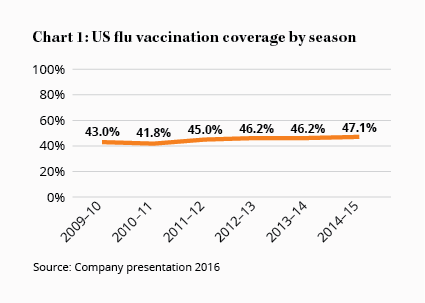

Unfortunately, as other manufacturers bring their own cell culture-based vaccines to market – as will inevitably be the case – and increase capacity, the competitive advantage is likely to be relatively short lived. The overall market, however, has been steadily growing thanks to the US Government recommending universal coverage in 2010. Although that goal is some way off with only around half the population getting a seasonal flu vaccination in 2015 (see Chart 1) and the 2016 season shaping up to be slightly worse.

One man's trash…

Nonetheless, CSL's flu business shows significant potential, both operationally and financially.

In the year prior to its acquisition, the Novartis flu business generated US$527m in revenue and an earnings before interest, tax, depreciation and amortisation (EBITDA) loss of US$138m.

BioCSL was only barely profitable itself, with US$425m in revenue – around $125m of which was from flu vaccines – and $23m in EBITDA.

Given the strong economies of scale associated with vaccine manufacturing, this isn't surprising: CSL and Novartis simply couldn't compete with Sanofi and GlaxoSmithKline. The acquisition combines two sub-scale manufacturers into one global heavyweight, with a strong product pipeline and plenty of manufacturing capacity.

CSL's management has outlined some optimistic goals for Seqirus. Even without a pandemic, Seqirus has several multi-year contracts to supply pre-pandemic vaccine stockpiles to various governments around the world. Management expects flu vaccine sales to reach US$1bn by 2020, up from around US$650m last year, and to cut US$75m a year in duplicated administration and research costs.

Management believes its flu business is capable of a 20% operating margin by 2020, which implies EBITDA of US$200m (CSL had total EBITDA of $1.8bn over the past 12 months).

If it gets anywhere close to that goal, the acquisition price of US$275m looks like a steal. Indeed, Novartis wrote off US$1.1bn on the sale reflecting the significant sunk cost of building the billion-dollar Holly Springs plant (which says nothing of the $487m pitched in by the US Department of Health).

With CSL's track record of successful acquisitions, we think management has a good chance at turning the flu business around and meaningfully contributing to growth in earnings per share over the next few years, despite 2016 likely to be poor due to integration costs and what turned out to be a benign Northern Hemisphere flu season. Management expects the flu business to produce a net loss of US$90m–120m in 2016.

CSL's overall revenue is expected to grow 7% and net profit to rise 5% in 2016, excluding the Novartis flu business. The stock is trading on a forward price-earnings ratio of around 24 and we continue to recommend you HOLD.

Recommendation