CSL and Australia's biggest lottery ticket

Recommendation

- {{x.value}}

{{ twilioFailed ? 'SMS Code Failed to Send…' : 'Enter verification code' }}

{{ completedStep1 ? 'Authentication & Security' : content.trialHeading.replace('{0}', user.FirstName) }}

{{ content.upgradeHeading.replace('{0}', user.FirstName) }}

The email address you entered is registered with InvestSMART

Please login to continue

We have sent you an email with the details of your registration.

Looks you are already a member. Please enter your password to proceed

{{ upgradeCTAText }}

Updating information

Please wait ...

Your membership to InvestSMART Group recently failed to renew.

Please make sure your payment details are up to date to continue your membership.

Having trouble renewing?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

You've recently updated your payment details.

It may take a few minutes to update your subscription details, during this time you will not be able to view locked content.

If you are still having trouble viewing content after 10 minutes, try logging out of your account and logging back in.

Still having trouble viewing content?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

Please click on the ACTIVATE button to activate your Intelligent Investor 15-day free trial

Please click on the ACTIVATE button to finalise your membership

Unsuccessful registration

Registration for this event is available only to Eureka Report members. View our membership page for more information.

Registration for this event is available only to Intelligent Investor members. View our membership page for more information.

- You are already registered for this event.

- This event is already full.

- Please select a quantity for at least one ticket.

- {{ i }}

Forgotten password

Please enter your email address below to request a new password

- Indepth analysis of ASX listed shares

- BUY, Hold and Sell Recommendations

- Ideas Lab

- Special Reports

- Alan Kohler’s Weekend Briefing

- Interviews with CEO’s & top influencers

- Money Cafe and Talking Finance

- Super Advice and Q&A with Ask Alan

Investors love to fixate on a company's numbers: its recent profit growth, margins, or price-earnings ratio, for example. We all like dealing with things that are easy to measure and often downplay – or outright ignore – those fuzzy factors like ‘optionality'.

CSL is the world's largest producer of drugs derived from blood plasma, accounting for just over a third of the market. Its bread and butter is selling antibodies and haemophilia therapies, but it also owns a few dozen lottery tickets – drugs that are in various stages of research and development (R&D). Their low probability of success makes it hard to gauge what they're worth, but they collectively expose CSL to new markets worth tens of billions. They're worth something.

Key Points

-

CSL-112 moves to Phase III

-

Cost of trial expected to hit US$500m

-

China offers further optionality

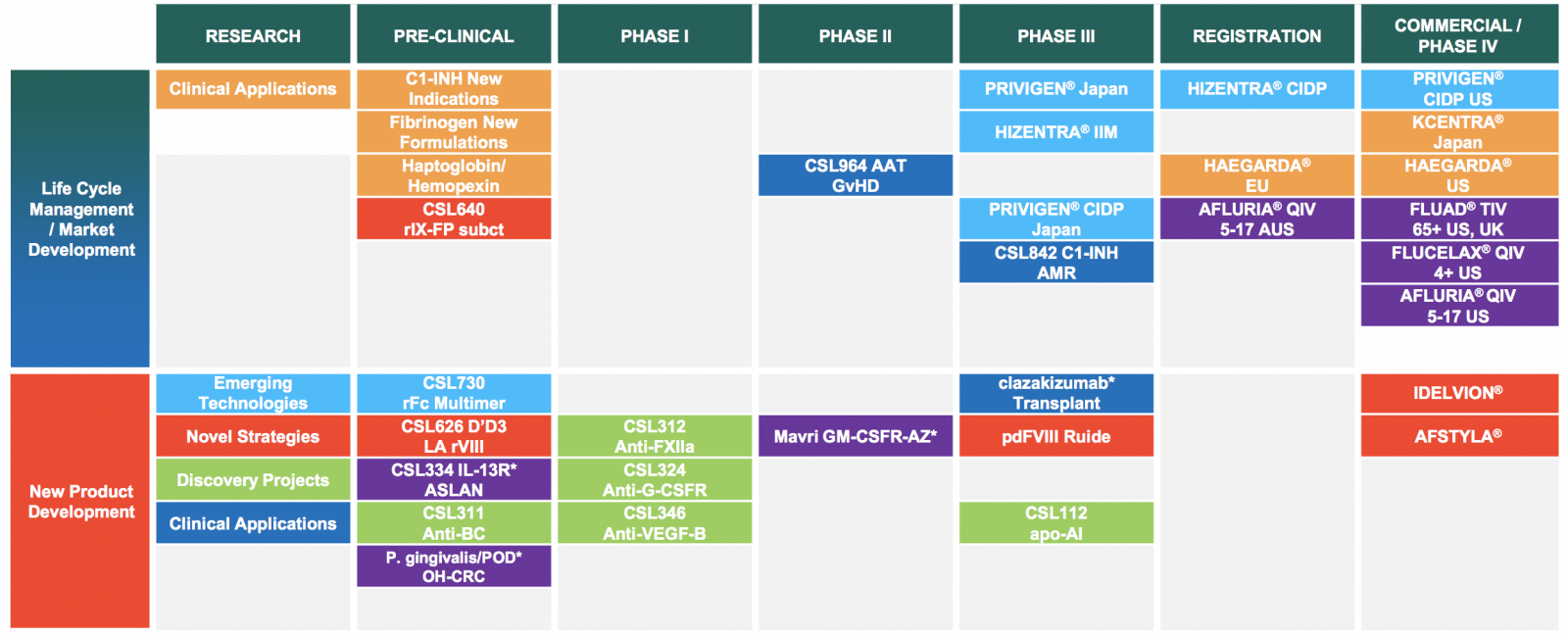

Take a look at the chart below, which was taken from December's R&D analyst briefing. It's a list of the key drugs currently being researched by CSL. You can think of it as a race, with each drug being tested at different levels of the clinical trial process. When successful, they take a step to the right. When they fail, they fall off the chart, or sometimes go back to an earlier stage for some tweaking.

One unassuming contestant is a product called CSL-112 and, in December, it notched up a spot in the race to Phase III. If CSL-112 notches up one place more, it could be the biggest molecular goldmine the company has ever unearthed – a ‘game changer' for CSL, as chief executive Paul Perreault put it.

Cost of living

Imagine that you are unlucky enough to have a heart attack, then lucky enough to survive. You're not out of the woods: around 14% of high-risk patients go on to have another heart attack within the first year, one that often does them in.

A few drugs already exist that reduce your risk of recurrent heart attacks but they only kick in after six months. More than two-thirds of subsequent attacks happen within the first 90 days.

So, the question is, after having a heart attack, what would you pay for a magic bullet that detoxes your body of bad cholesterol, cuts your chances of another heart attack or stroke and, crucially, starts acting immediately? Now multiply that price by half-a-million. That's how much revenue CSL could earn each year from this one drug.

Between the US and the five largest countries in Europe, roughly 1.2 million people have a heart attack each year. Half-a-million or so are at risk of a second event, and after adjusting for insurance coverage and other factors, CSL believes between 200,000 and 270,000 patients a year would be eager to buy its new ‘cholesterol killing' drug.

That's just the six largest markets – those that CSL will target in the first five years of launch. Consider that they represent less than a tenth of the world population, or half of the developed world, where sales are going to be highest.

Green light

We've been following the progress of CSL-112 since 2014 (see CSL tackles leading cause of death). Back then it was little more than a curious drug that had only just entered Phase II of the clinical trial process. At that point in the game, failure is far more common than success: broadly, five drugs fail the next set of trials for every one that makes it through.

A lot has changed in three years: CSL-112's odds of success have progressed from ‘roll of the dice' status to ‘flip a coin'. Since then it has passed three more clinical trials that cover things like dosing and patient safety.

In December, management announced that after review of all the clinical trial data collected to date, it has given the green light to Phase III trials.

The size and importance of this study is super-colossal, even by ‘big pharma' standards. The company will recruit 17,400 patients spread over 1,000 hospitals in 40 countries. It's expected to last 3.5 years or so. With a total price tag of US$450–550m, CSL will be chewing through around US$400,000 a day. It's the largest clinical trial the company has ever undertaken.

Although management hasn't given any concrete guidance of what it expects CSL-112 to earn if it reaches commercialisation, it's clear that it's a multi-billion dollar opportunity to justify this level of up-front investment.

CSL is still negotiating the final details of the study with the US Food & Drug Administration to ensure that, if it meets the requirements, the drug will be approved for sale. Management is confident those final details will be resolved in the next few months and that recruitment of patients can begin mid this year.

Whether all this pays off won't be known until 2021, and CSL-112 will only hit the market in 2022 if all goes well.

It's also worth noting that only 58% of drugs entering Phase III trials make it through. This could be money down the drain, though the company has said it will review preliminary data roughly two years in to see that the drug is having the intended effect and, if not, will cancel the rest of the trial.

China expansion

For those who like adrenaline, CSL-112 adds some high-risk/high-reward pizazz to a healthcare stalwart. Even if the Phase III trial fails, though, the rest of the business is still performing admirably. That's the point: CSL isn't a ‘lottery ticket stock', as with most small-cap biotechs. It's a high-quality blue chip with a lottery ticket attached.

Demand for antibodies in CSL's main markets is growing at 8% a year, and the company has been increasing its market share in recent years. Sales grew 14% in the year to June, with CSL's two flagship products – Hizentra and Privigen – growing 10% and 21% respectively due to more convenient dosing than competitors.

Overall revenue rose 15% to US$6.9bn after removing the effect of currency fluctuations, with underlying net profit up 24% to US$1.3bn. Not bad for a 102-year-old company.

Even the antibody side of the business, however, has its own ‘optionality'. In June, CSL purchased a small Chinese plasma therapy maker, making it the first major plasma company to now have Chinese operations. China is the second largest antibody market in the world (behind the US) and the fastest growing. It's expected to reach US$4.9bn in sales by 2020 but, until now, CSL has been locked out of the market because China forbids imports. That's why securing a local operator was so important.

CSL has significant economies of scale and is the world's lowest-cost producer of plasma products, so there's every reason to believe the company will take significant market share when it receives approval to sell its products in China.

Management expects net profit of US$1,480–1,550m in 2018, up around 13%, for a forward price-earnings ratio of 33 at current exchange rates.

Undoubtedly, CSL is one of the priciest healthcare stocks around, but making the case that it's overvalued is more difficult. With formidable competitive advantages, a dominant market position, economies of scale, and lottery tickets in CSL-112 and China, we're sticking with HOLD.

Recommendation