Crown demerger: enhancing value?

Recommendation

- {{x.value}}

{{ twilioFailed ? 'SMS Code Failed to Send…' : 'Enter verification code' }}

{{ completedStep1 ? 'Authentication & Security' : content.trialHeading.replace('{0}', user.FirstName) }}

{{ content.upgradeHeading.replace('{0}', user.FirstName) }}

The email address you entered is registered with InvestSMART

Please login to continue

We have sent you an email with the details of your registration.

Looks you are already a member. Please enter your password to proceed

{{ upgradeCTAText }}

Updating information

Please wait ...

Your membership to InvestSMART Group recently failed to renew.

Please make sure your payment details are up to date to continue your membership.

Having trouble renewing?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

You've recently updated your payment details.

It may take a few minutes to update your subscription details, during this time you will not be able to view locked content.

If you are still having trouble viewing content after 10 minutes, try logging out of your account and logging back in.

Still having trouble viewing content?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

Please click on the ACTIVATE button to activate your Intelligent Investor 15-day free trial

Please click on the ACTIVATE button to finalise your membership

Unsuccessful registration

Registration for this event is available only to Eureka Report members. View our membership page for more information.

Registration for this event is available only to Intelligent Investor members. View our membership page for more information.

- You are already registered for this event.

- This event is already full.

- Please select a quantity for at least one ticket.

- {{ i }}

Forgotten password

Please enter your email address below to request a new password

- Indepth analysis of ASX listed shares

- BUY, Hold and Sell Recommendations

- Ideas Lab

- Special Reports

- Alan Kohler’s Weekend Briefing

- Interviews with CEO’s & top influencers

- Money Cafe and Talking Finance

- Super Advice and Q&A with Ask Alan

Your maths teacher might not like it, but in the strange world of corporate reorganisations and spin-offs two plus two can potentially equal five. Herein lies the potential attraction of the proposed Crown Resorts restructure aimed at ‘enhancing shareholder value'.

As noted in Crown spins off international ops and hotels on 16 Jun 16 (Buy — $12.75), Crown Resorts intends to demerge most of its international operations into a separate company.

Key Points

-

Most international holdings demerged

-

Crown Resorts to keep Australian casinos

-

Potential IPO of Australian hotels too

The spin-off – InternationalCo – will hold a 27.4% interest in Melco-Crown Entertainment, a majority interest in the planned Alon casino in Las Vegas and other smaller assets (see Table 1).

Existing shareholders will retain their shares in Crown Resorts while also receiving new shares in InternationalCo proportionate to their existing holdings.

Crown Resorts – we'll tag it ‘OzCo' to avoid confusion – will retain full ownership of Crown's Australian casinos in Melbourne and Perth, the future Crown Sydney, Crown Aspinalls in the United Kingdom and the company's fast-growing wagering and online gaming businesses.

| OzCo | InternationalCo |

|---|---|

| Crown Melbourne | Melco Crown Entertainment (27.4% interest) |

| Crown Perth | Alon Las Vegas |

| Crown Sydney | Nobu (20%) |

| Crown Aspinalls (UK) | Aspers (50%) |

| Wagering & Online | Caesars |

|

Note: OzCo may also float 49% of most of its Australian hotels |

|

The company is also considering floating a 49% interest in its Australian hotels (except for Crown Towers Melbourne) by way of a listed property trust. The proposed trust will own more than 2,300 hotel rooms and lease them to OzCo on long-term leases.

The demerger and proposed initial public offering (IPO) are still subject to final sign-off from the Board and ratification by shareholders and various regulators. However, by spinning off InternationalCo, the goal is for the strong performance of Crown Resorts' Australian assets to become more visible to the market and hopefully more highly valued as a result. In that way, OzCo and InternationalCo should be worth more in total as separate entities than combined under the one banner as they are now.

To see whether this is a reasonable goal, let's analyse the proposed reorganisation, starting with OzCo.

Australia

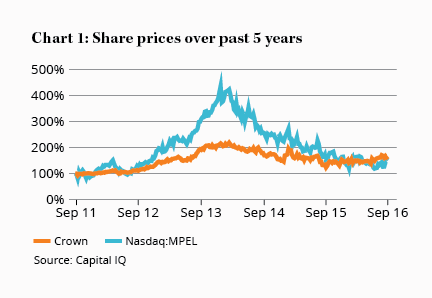

Management claims that ‘Crown Resorts' share price has been highly correlated to the performance' of Melco-Crown and the share price charts back them up (see Chart 1).

The demerger will mean shareholders in InternationalCo will now have to deal with concerns over Macau's future due to the Chinese government's corruption crackdown and the stuttering Chinese economy. As such, OzCo's share price should more closely track the performance of its monopoly casinos in Melbourne and Perth.

Although its greater geographical concentration means OzCo will be even more affected by any future Australian economic downturns, we'd expect growth in earnings to at least match economic growth over the long term (see Betting on Crown – part 1 on 20 Apr 15 (Buy — $13.15)).

Crown Resort's equity accounted profit from its Melco-Crown investment fell 64% in 2016 and its Australian casinos in Melbourne and Perth now generate around 83% of net profit. So it isn't surprising that Crown Resorts recently amended its dividend policy to pay out 100% of normalised profit excluding profits from associates but including dividends from associates (due to the volatility arising from the large amounts VIPs bet, casinos adjust their earnings to reflect theoretical rather than actual win rates from VIPs). This should also help support OzCo's share price in this era of very low interest rates and the resulting search for yield.

OzCo also has attractive growth prospects, not least from its $2bn Crown Sydney casino now under construction but also from its fast-growing (albeit currently barely profitable) wagering and online gaming businesses. Freed from exposure to Macau, this could also help OzCo trade on higher multiples. On the downside, Crown Sydney could prove more expensive than expected to build and/or the company could receive less than the $500m expected from the sale of apartments included in the Crown Sydney building.

Hotel REIT

InternationalCo's status as a holding company means it's unlikely to be able to support much on-balance sheet debt, so most if not all of Crown Resorts' existing $2.3bn in gross debt is likely to remain with OzCo.

This is another reason why further value may be realised should Crown Resorts (and hence presumably OzCo) proceed with the IPO of 49% of its Australian hotels except for Crown Towers Melbourne.

Crown is clearly taking advantage of high property prices – and, in particular, foreign investor demand for Australian hotels – and will be able to use the cash raised to help fund capital expenditure and/or reduce its debt burden.

Importantly, not only will Crown Resorts/OzCo likely earn top dollar from the IPO, it will also profit from the difference between what it pays in leasing costs and the hotels' earnings. Australian hotels are currently much sought after due to increasing occupancies and revenue earned per room as a result of rising numbers of foreign visitors and the dearth of new hotels being constructed.

As for the IPO, it may be of interest to members depending on its price, yield and lease terms and your personal situation and return expectations (see Getting a Hold on property trusts for more on our recent slight shift in emphasis on listed property trusts).

InternationalCo

By contrast, InternationalCo will be dominated by its investment in Melco Crown Entertainment. Adding in its likely mediocre yield and it's possible that investors will quickly dump InternationalCo, perhaps giving those who aren't currently shareholders in Crown an opportunity.

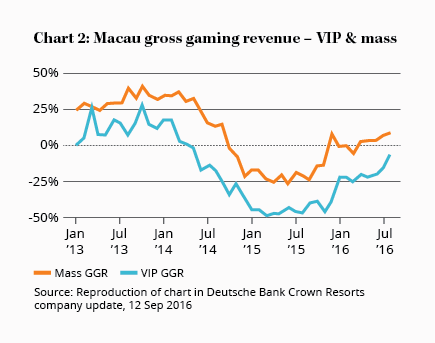

As we noted in Betting on Crown – part 1, though, there are many reasons to think that Macau will overcome its present difficulties over the medium to long term. More recently, in Crown: 2016 result on 18 Aug 16 (Hold — $13.82) we noted that the decline in Macau's gross gambling revenue (GGR) may have bottomed and more recent evidence supports this view (see Chart 2).

As you can see from Chart 2, the more profitable mass market GGR has finally started to increase, albeit helped by recent casino openings including Melco Crown's still-ramping-up Studio City. Total visitors to Macau, visitors staying overnight and gaming spend per visitor are all rising too. Whilst still early, this suggests that the increase in supply of hotel rooms and tables from recent and future casino openings may be absorbed over the medium term, particularly as various infrastructure improvements are completed (see Betting on Crown – part 1 for more).

We'll have to wait for final details on the proposed demerger and IPO before determining whether the sum of the parts will in fact be greater than the whole. We suspect they will be, but like any recommendation, our views will depend on the relationship between price and value. In the meantime, we recommend you HOLD.

Note: The Intelligent Investor Growth Portfolio owns shares in Crown. You can find out about investing directly in Intelligent Investor and InvestSMART portfolios by clicking here.

Recommendation