Computershare upgraded to Buy

Recommendation

- {{x.value}}

{{ twilioFailed ? 'SMS Code Failed to Send…' : 'Enter verification code' }}

{{ completedStep1 ? 'Authentication & Security' : content.trialHeading.replace('{0}', user.FirstName) }}

{{ content.upgradeHeading.replace('{0}', user.FirstName) }}

The email address you entered is registered with InvestSMART

Please login to continue

We have sent you an email with the details of your registration.

Looks you are already a member. Please enter your password to proceed

{{ upgradeCTAText }}

Updating information

Please wait ...

Your membership to InvestSMART Group recently failed to renew.

Please make sure your payment details are up to date to continue your membership.

Having trouble renewing?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

You've recently updated your payment details.

It may take a few minutes to update your subscription details, during this time you will not be able to view locked content.

If you are still having trouble viewing content after 10 minutes, try logging out of your account and logging back in.

Still having trouble viewing content?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

Please click on the ACTIVATE button to activate your Intelligent Investor 15-day free trial

Please click on the ACTIVATE button to finalise your membership

Unsuccessful registration

Registration for this event is available only to Eureka Report members. View our membership page for more information.

Registration for this event is available only to Intelligent Investor members. View our membership page for more information.

- You are already registered for this event.

- This event is already full.

- Please select a quantity for at least one ticket.

- {{ i }}

Forgotten password

Please enter your email address below to request a new password

- Indepth analysis of ASX listed shares

- BUY, Hold and Sell Recommendations

- Ideas Lab

- Special Reports

- Alan Kohler’s Weekend Briefing

- Interviews with CEO’s & top influencers

- Money Cafe and Talking Finance

- Super Advice and Q&A with Ask Alan

- Merger synergies and $A have delivered earnings boost

- Corporate actions revenue needs higher interest rates to flourish

- Core business remains strong; shares undervalued

Computershare is the world's largest share registry business, managing records, legal titles and dividend payments on behalf of the shareholders of its clients across the globe. It also takes queries and phone calls from shareholders and manages complex employee equity plans.

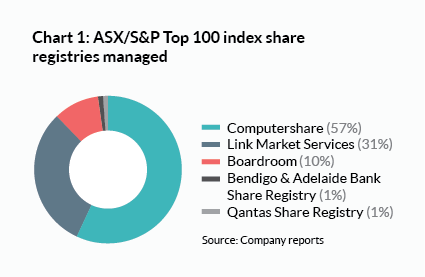

Its dominant market share in Australia (see Chart 1) is just a small part of its global network of registries. Computershare has operations in over 20 countries, provides services to more than 16,000 clients and its share registries occupy market-leading positions in all major markets, including the United States following the 2011 acquisition of the Shareowner Services business.

Over the past three years, forecast earnings per share has increased 61% to 74 cents, pushing its share price up 20%. You'd think we'd be happy with that, but it feels like there's something missing.

Computershare has been a major beneficiary of the 21% fall in the A$ from US$1.06 to US$0.84 in recent years, which has almost doubled the 29% rise in US$ earnings to 54% in A$ terms. The company will continue to benefit from further falls in the A$ although keep in mind that the reverse is also true: if the A$ rises, then profits will suffer.

Antiquated system

The other major tailwind for earnings has been cost cutting from the integration of its US Shareowner Services acquisition, with management exceeding its previous target of $73m in annual cost savings and now aiming for $80m by June 2015.

Yet there could have been many more benefits from this acquisition. Given Computershare's skills in this area and the US's antiquated system of broker accounts and 'street' shareholdings, the company should have been able to sell more services to its new customers.

But the system remains as antiquated as ever and, in fact, is getting steadily worse. As shareholders convert from paper certificates to electronic dealing, they mostly opt to let their broker manage their holding, effectively amalgamating themselves for the purposes of the share register. The result is annual attrition of about 2% in Computershare's US registry business and organic growth is barely keeping up, with US revenues of $468m in the six months to June, up just 3% in two years. So the Shareowner Services acquisition has been good but not great.

Heart and soul

Computershare is entitled to the interest on much of the cash it holds on behalf of clients (and their shareholders) and has suffered from continuing low interest rates. At some stage interest rates will have to go higher, but that's looking as far away as ever. Ultimately, though, if Computershare isn't getting its value from interest rates, then we'd expect it to start moving its client agreements to a different revenue model as they roll over.

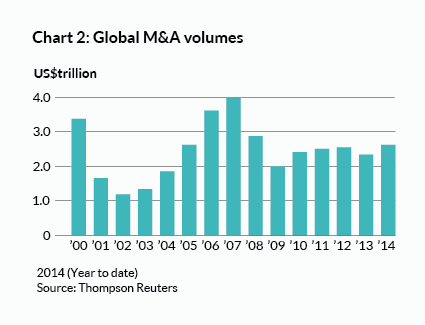

The company's corporate activity business has been the most frustrating. This goes to the heart and soul of Computershare, because not only does it provide its own revenue stream, but it feeds into other areas. IPOs, for example, will hopefully bring a new client for the rest of the business, and mergers and acquisitions increase communications with shareholders, some of which feeds into stakeholder relationship management and communications services revenues.

So with global merger & acquisition (M&A) activity in the first nine months of 2014 already exceeding its level for each of the past five years (see Chart 2), it's disappointing that revenues from this area are still bumping along the bottom. And we'd guess against any immediate improvement, with management saying at last month's AGM that underlying group earnings per share in the first half of the current financial year are likely to be lower than the prior period.

When we asked the company about this, they explained that deal flow had indeed improved but that, particularly in North America, a significant portion of corporate actions revenue comes from interest earned on client cash balances. So instead of hoping for a rise in interest rates or an increase in corporate activity, it looks like we probably need at least a bit of both.

Core business strong

So some of the gloss has come off Computershare's business, but a couple of things keep us positive. The first is that the company's lock on the share registry business looks as tight as ever. Of the 74 companies in the ASX 100 in both 2005 and 2014, Computershare has a market share of 57%.

Over the nine-year period it has lost five clients and gained three, but it has made up for the difference due to a 65% share of companies entering the index. More remarkably, only 11 of the 74 companies switched registrars between 2005 and 2014 – a 'churn' rate of about 1.7%.

Year to 30 Jun (US$m) | 2010 | 2011 | 2012 | 2013 | 2014 |

|---|---|---|---|---|---|

Register maintenance | 660 | 699 | 775 | 824 | 822 |

Corporate actions | 183 | 180 | 156 | 169 | 154 |

Business services | 276 | 266 | 383 | 489 | 488 |

Stakeholder relationship mgmt | 164 | 97 | 87 | 77 | 75 |

Employee share plans | 120 | 158 | 197 | 237 | 260 |

Communication Services | 159 | 172 | 182 | 198 | 195 |

Technology & other revenue | 58 | 48 | 39 | 31 | 30 |

Total revenue | 1,620 | 1,619 | 1,819 | 2,025 | 2,023 |

Operating costs | 1,111 | 1,125 | 1,360 | 1,555 | 1,520 |

Underlying operating profit | 511 | 494 | 459 | 470 | 503 |

Underlying net profit | 321 | 309 | 273 | 305 | 335 |

Underlying EPS (US cents) | 58 | 56 | 49 | 55 | 60 |

Underlying EPS (A cents | 67 | 53 | 48 | 60 | 64 |

PER | 17 | 22 | 24 | 19 | 18 |

DPS (A cents) | 28 | 28 | 28 | 28 | 29 |

Dividend yield (%) | 2.4 | 2.4 | 2.4 | 2.4 | 2.5 |

Franking (%) | 55 | 60 | 60 | 20 | 20 |

Now Australia only contributes about 18% of group revenues, but these numbers tell you something about the strength of Computershare's share registry business around the world. We also have confidence that – one way or another – it will be able to earn good money for the value it adds.

Attractive cash flow

All up, we remain comfortable with Computershare's core share registry business, and our biggest concern is that new chief executive Stuart Irving tries to buy growth elsewhere. If growth is subdued in the core business, we'd much prefer to see the company paying down debt and paying a larger dividend.

With management guiding for 2015 earnings of US$0.62 or $0.74, that puts the stock on a forward price-earnings ratio of 15 and a free cash flow yield of 7%, given the almost 100% flow-through of earnings to cash. Despite our frustrations, that's plenty to keep us interested. With the stock down 7% since Computershare to benefit from M&A 'explosion' from 19 Aug 14 (Hold - $12.09) and below our buy price of $12.00, we're upgrading to BUY with a maximum recommended portfolio weighting of 7%.

Recommendation