Can't buy me business models

- {{x.value}}

{{ twilioFailed ? 'SMS Code Failed to Send…' : 'Enter verification code' }}

{{ completedStep1 ? 'Authentication & Security' : content.trialHeading.replace('{0}', user.FirstName) }}

{{ content.upgradeHeading.replace('{0}', user.FirstName) }}

The email address you entered is registered with InvestSMART

Please login to continue

We have sent you an email with the details of your registration.

Looks you are already a member. Please enter your password to proceed

{{ upgradeCTAText }}

Updating information

Please wait ...

Your membership to InvestSMART Group recently failed to renew.

Please make sure your payment details are up to date to continue your membership.

Having trouble renewing?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

You've recently updated your payment details.

It may take a few minutes to update your subscription details, during this time you will not be able to view locked content.

If you are still having trouble viewing content after 10 minutes, try logging out of your account and logging back in.

Still having trouble viewing content?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

Please click on the ACTIVATE button to activate your Intelligent Investor 15-day free trial

Please click on the ACTIVATE button to finalise your membership

Unsuccessful registration

Registration for this event is available only to Eureka Report members. View our membership page for more information.

Registration for this event is available only to Intelligent Investor members. View our membership page for more information.

- You are already registered for this event.

- This event is already full.

- Please select a quantity for at least one ticket.

- {{ i }}

Forgotten password

Please enter your email address below to request a new password

- Indepth analysis of ASX listed shares

- BUY, Hold and Sell Recommendations

- Ideas Lab

- Special Reports

- Alan Kohler’s Weekend Briefing

- Interviews with CEO’s & top influencers

- Money Cafe and Talking Finance

- Super Advice and Q&A with Ask Alan

“Guitar groups are on their way out, Mr Epstein.” With those words, Dick Rowe of Decca Records turned down The Beatles. Well, supposedly. Rowe denied saying them ‘till his last breath, but history charged him anyway.

What few people understand is that Rowe wasn't an outlier. Every major label on both sides of the Atlantic repeated his error, without it making an iota of difference to their long-term wellbeing. Yes, theirs was indeed a business model made in a sky with diamonds. If you missed a few stars, well, it didn't matter.

For many Londoners, Liverpool remains a distant, provincial city, reached by a nightmarish train trip from Euston to Lime Street. Rowe sent his assistant to The Cavern, who was evidently impressed. Nineteen days later, after a 10-hour drive in a snowstorm, The Beatles auditioned for Decca.

It did not go well. In Anthology, McCartney admits “we weren't that good,” although Lennon, contrary to the last, said, “we were just doing a demo. They should have seen our potential.” Had Liverpool been closer to London, Rowe might have. Instead, he signed The Tremeloes, from Dagenham, Essex – a place not known for its golden silence – a reasonable cab ride east of his Hampstead office.

The Beatles were turned down by six major UK labels, including EMI, before George Martin signed them to EMI-owned Parlophone in ‘62. The story of missed opportunity then made its way across the Atlantic, told in fascinating detail in this Slate Culture Gabfest podcast. Here's the US Billboard Hot 100 chart from April 4, 1964:

No act has ever repeated The Beatles' occupation of the top five spots in the Billboard charts. But check out the column on the far right in the image above. Those five songs were distributed on three different labels, only two of which were owned by EMI's Capitol Records. How so?

Well, Capitol saw the entire UK as a musical backwater. The US had invented rock and roll and the Yanks weren't about to be pushed around by a country that last topped the US charts with Acker Bilk, a trad jazz clarinet player from Somerset that had lost half a finger in a sledging accident.

EMI didn't push it. Instead, it banged on the industry's biggest doors; Atlantic Records, RCA, Columbia and Mercury, all of whom gave the Capitol response. Rowe may have looked stupid for knocking back The Beatles but he was in good company. Only after three independent labels took a subsequently successful flyer on an unknown UK outfit did Capitol capitulate. The result was five songs by the same artist in the same chart, on three separate labels.

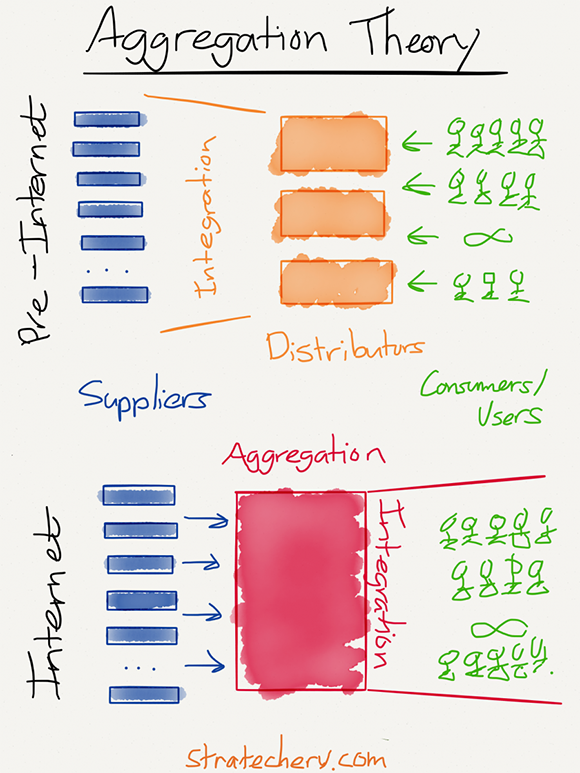

Which makes you wonder, right? Had George Martin not been around, would an entire industry have missed the biggest act of all time? Well, it's possible. This illustration from Ben Thompson of Stratechery explains why:

Prior to the Internet suppliers, distributors and consumers combined to form a typical value chain. For investors, this is a critical model to understand because it shows how a business can capture more of the chain's value.

As Thompson says, “The best way to make outsize profits in any of these markets is to either gain a horizontal monopoly in one of the three parts or to integrate two of the parts such that you have a competitive advantage in delivering a vertical solution. In the pre-Internet era, the latter depended on controlling distribution.”

An example of horizontal integration might be a big bank buying lots of smaller ones in order to control the distribution of mortgages. An example of vertical integration might be a company providing dispatch services to the taxi industry expanding into taxi licences and payments systems.

The beauty of both models is that once you've locked up control of the value chain it doesn't matter what the customer thinks. You can deliver an appalling, over-priced service, as did Cabcharge, for example, and still prosper. As Paul Weller sang in Going Underground, “The public gets what the public wants.”

In the music industry, distribution had been wonderfully integrated with supply through people like Rowe. It was the model that was the haymaker, not a particular band that passed through it. As if to prove the point, a few months after missing out on The Beatles Rowe signed The Rolling Stones.

This long and winding road leads us not to her door but the second part of the diagram. By aggregating customers rather than distributors or suppliers, a dramatic shift in power takes place, from value chain monopolists to their customers. This is a point lost on many investors. Once a product like a music track, book or advertisement can be digitised, the cost of distributing it falls to zero, with transaction costs often not far behind.

Thompson again: “[These factors have] fundamentally changed the plane of competition: no longer do distributors compete based upon exclusive supplier relationships, with consumers/users an afterthought. Instead, suppliers can be aggregated at scale leaving consumers/users as a first order priority.”

Let's run through a few examples. Newspapers aggregated news, opinion, sports coverage and advertising. Google broke this model by aggregating huge audiences with journalism, permitting searches for individual stories that interested them. Targeted advertising came as a very profitable afterthought. Facebook then took targeted advertising to the next level through people's newsfeed.

Amazon has integrated distribution in books, groceries, video, music and other categories through a vast ecommerce platform with one click payment and fast delivery that attracts vast numbers of users. Its services are so good a major part of its business is now supporting other online retailers. Amazon now accounts for more than half of all online sales growth in the US.

This shift, to a business model that aggregates suppliers and customers by focussing on customer experience, has a number of implications for investors.

First, a focus on customer aggregation has created monopolies the likes of which we have never seen. Amazon controls 50 per cent of the US market for books and accounts for more than half of all online sales growth. Google controls 68 per cent of US online searches (90 per cent in Europe). In the third quarter of 2010, Facebook passed 500 million active users. This year it will surpass two billion. In the last (US) quarter, Netflix added 7.05 million subscribers, beating its own expectations by two million. It now has 100 million paying subscribers while Uber has 40 million monthly active riders.

These businesses are only just getting going, which is my second point. The Internet permits customer aggregation on an unprecedented global scale, allowing giant companies to grow at rates formerly seen only by businesses with much smaller footprints.

Alphabet (formerly Google) recently reported first quarter revenue growth of 22 per cent year-on-year (yoy). Amazon managed a similar figure while Facebook recently announced a 50 per cent yoy increase, similar to that achieved by Alibaba, China's online commerce giant.

These would be impressive figures for much smaller companies. Yet Facebook and Amazon's market cap is now almost $US500 billion, Alphabet's $US690bn, Alibaba's $US390bn and Netflix a mere snip at $US71bn. It really is quite astonishing.

The third point to understand is the virtuous circle established by this new business model. More customers begets more data, which begets better services – think Gmail, Facebook Messenger and Amazon Prime – which begets more customers.

There's likely to be a second-order impact in this regard. Because the new monopolists enhance their market position by doing a better job for their users, the backlashes experienced by old-style monopolists are less likely. If competition regulators try to restrict their market power it is they who might face a backlash, from consumers.

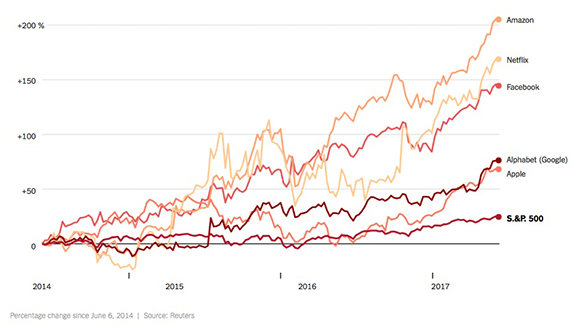

Fourth, only some of the optimism embedded in these market capitalisations has merit. Apple (disclosure: I'm a shareholder), Amazon and Facebook are now so large they account for almost a third of the S&P 500 index (Alphabet is listed on NASDAQ). Here's the chart showing the price rises of major tech stocks over the past few years:

If you're looking to invest in some of the best business models the world has ever seen, well, join the queue. And be prepared to pay a hefty price for the privilege. We're probably going to have to wait for a temporary slip in some of these business to get a chance of a reasonable price (I won't bore you with the multiples, but they're high). In the meantime, local online monopolists like Trade Me still fly under the radar.

Finally, whilst it's tempting to believe these battles have already been fought and won, many industries still operate on the old model of command and control. Think banking, finance, transport, health and energy. The Internet is already having an impact on industries like these but there's a long way to go, which is why understanding aggregation theory is important. Almost every stock in your portfolio is likely to be affected by it one way or another. As Fairfax CEO Greg Hywood, the late Reg Kermode of Cabcharge and Ahmed Fahour, CEO of Australia Post, might admit, it is indeed a Revolution.

That's it. Thanks for your time. I'll wish you a wonderful weekend and let you Get Back to your brekkie.

Coda: Interestingly, the music industry has fared better in the Internet era than newspapers and book publishers. Apple's iTunes aggregated customers by focussing on user experience, as aggregation theory indicates, weakening the label's grip on distribution. But they retained more control over supply. Then, the arrival of streaming services like Spotify, Amazon Music and Tidal opened up more distribution channels, reducing Apple's dominance. It's not as good as it was back in Rowe's day but it could have been worse. Which is to say I might have chosen a better metaphor than the music industry for this piece, but then we wouldn't have had the chance to reminisce about The Beatles, and what could be better than that?