Argo: staying the course

Recommendation

- {{x.value}}

{{ twilioFailed ? 'SMS Code Failed to Send…' : 'Enter verification code' }}

{{ completedStep1 ? 'Authentication & Security' : content.trialHeading.replace('{0}', user.FirstName) }}

{{ content.upgradeHeading.replace('{0}', user.FirstName) }}

The email address you entered is registered with InvestSMART

Please login to continue

We have sent you an email with the details of your registration.

Looks you are already a member. Please enter your password to proceed

{{ upgradeCTAText }}

Updating information

Please wait ...

Your membership to InvestSMART Group recently failed to renew.

Please make sure your payment details are up to date to continue your membership.

Having trouble renewing?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

You've recently updated your payment details.

It may take a few minutes to update your subscription details, during this time you will not be able to view locked content.

If you are still having trouble viewing content after 10 minutes, try logging out of your account and logging back in.

Still having trouble viewing content?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

Please click on the ACTIVATE button to activate your Intelligent Investor 15-day free trial

Please click on the ACTIVATE button to finalise your membership

Unsuccessful registration

Registration for this event is available only to Eureka Report members. View our membership page for more information.

Registration for this event is available only to Intelligent Investor members. View our membership page for more information.

- You are already registered for this event.

- This event is already full.

- Please select a quantity for at least one ticket.

- {{ i }}

Forgotten password

Please enter your email address below to request a new password

- Indepth analysis of ASX listed shares

- BUY, Hold and Sell Recommendations

- Ideas Lab

- Special Reports

- Alan Kohler’s Weekend Briefing

- Interviews with CEO’s & top influencers

- Money Cafe and Talking Finance

- Super Advice and Q&A with Ask Alan

With the ASX's biggest stocks struggling recently, the country's two largest listed investment companies have both underpeformed the index, but they're responding in different ways.

At its full-year result a fortnight ago, Australian Foundation Investment Company revealed a 1.6% loss for the year, compared to the 0.6% positive return of the S&P/ASX 200 Accumulation Index. However, it said it had increased its weighting to small and mid-capitalisation companies from 15% to 22%, in a bid to find better returns (see AFIC: turning a big ship on 25 Jul 16 (Hold – $5.84).

Today it was Argo Investments' turn to 'fess up to a loss of 1.6% (even after accounting for management fees from the company's listed global infrastructure fund launched just over a year ago.)

The 70-year-old LIC declared a fully franked final dividend of 15.5 cents per share taking the total for the year to 30.5 cents, 1 cent higher than in 2015. The dividends flowing in from its investments are clearly under pressure and managing director Jason Beddow said he expected ‘further challenges to dividends from a number of companies'.

Unlike AFIC, however, Argo seems intent on staying the course. Instead of selling down its larger holdings and increasing its exposure to smaller stocks Argo seems happy to back its existing portfolio. Beddow made specific mention to this, saying that despite the negative impact the larger sectors had on its investment performance in 2016, he was confident that the portfolio would deliver growth and income over the long term.

This is a point of difference investors should watch. Argo and AFIC's performance numbers were pretty much in line last year with Argo returning 0.4% more. However, AFIC's strategic shift means that future performance may diverge by more.

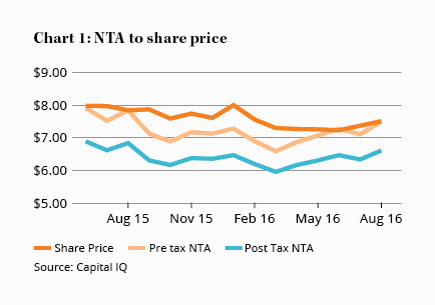

Over the past twelve months Argo has consistently traded at a premium to its pre-tax net tangible assets (NTA), and that continues to be the case, although the premium currently stands at a skinny 0.40%. To argue that the stock is undervalued we'd need to see a decent discount to pre-tax NTA and ideally closer to post-tax NTA. But, as with AFIC, it is nevertheless a reasonable option for long-term investors that don't want to pick their own stocks. HOLD.