APN Property: REIT or fund manager?

- {{x.value}}

{{ twilioFailed ? 'SMS Code Failed to Send…' : 'Enter verification code' }}

{{ completedStep1 ? 'Authentication & Security' : content.trialHeading.replace('{0}', user.FirstName) }}

{{ content.upgradeHeading.replace('{0}', user.FirstName) }}

The email address you entered is registered with InvestSMART

Please login to continue

We have sent you an email with the details of your registration.

Looks you are already a member. Please enter your password to proceed

{{ upgradeCTAText }}

Updating information

Please wait ...

Your membership to InvestSMART Group recently failed to renew.

Please make sure your payment details are up to date to continue your membership.

Having trouble renewing?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

You've recently updated your payment details.

It may take a few minutes to update your subscription details, during this time you will not be able to view locked content.

If you are still having trouble viewing content after 10 minutes, try logging out of your account and logging back in.

Still having trouble viewing content?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

Please click on the ACTIVATE button to activate your Intelligent Investor 15-day free trial

Please click on the ACTIVATE button to finalise your membership

Unsuccessful registration

Registration for this event is available only to Eureka Report members. View our membership page for more information.

Registration for this event is available only to Intelligent Investor members. View our membership page for more information.

- You are already registered for this event.

- This event is already full.

- Please select a quantity for at least one ticket.

- {{ i }}

Forgotten password

Please enter your email address below to request a new password

- Indepth analysis of ASX listed shares

- BUY, Hold and Sell Recommendations

- Ideas Lab

- Special Reports

- Alan Kohler’s Weekend Briefing

- Interviews with CEO’s & top influencers

- Money Cafe and Talking Finance

- Super Advice and Q&A with Ask Alan

Businesses don't get much more asset-light than fund managers.

After a few desks and computers, little else is needed to manage $50m, or $5bn, of funds. Some even operate without equity altogether, like Platinum Asset Management (ASX:PTM), whose shareholders would have virtually nothing invested if its excess cash and investments were distributed.

But then there's APN Property (ASX:APD), a manager of $2.4bn of property funds, that clearly missed the asset-light memo.

Key Points

-

Part REIT, part fund manager

-

Sensitive to interest rates

-

Put on your watchlist

Instead of a barren balance sheet, APN's is bloated with investments. To be on APN's level, Platinum would need to hold $2.6bn of investments.

This asset rich model makes APN part real estate investment trust (REIT), part fund manager, creating a valuation conundrum that requires some untangling.

We hoped its unique structure might breed opportunity, if the value of the funds management business was being obscured by the investments.

But after some untangling, it seems that the market has it about right. So, you won't find a buying opportunity here, but there is a decent business worth keeping an eye on.

The sausage factory

You're probably wondering why APN chooses to hold so many assets. The short answer is to grow its funds management business.

A large asset base allows APN to manufacture new property funds. It does this by purchasing property assets and then packaging them into new funds to sell to investors.

By appointing itself as the fund manager, APN locks in an ongoing revenue stream (typically worth around 0.60% of gross assets each year). Selling units to investors unlocks APN's capital, which allows it to be reused to create the next fund. Rinse and repeat.

This strategy requires foresight to anticipate popular funds, the expertise to manufacture them and the distribution capability to sell them. APN has skill across all three.

A recent example is Convenience Retail REIT, which packages a bunch of existing private funds (including APN's Property Plus Portfolio) to create a larger, ASX-listed fund.

APN's asset-rich balance sheet is partly born out of necessity. Property assets are unique and payment is required upfront and in full. You can't buy 10% of a warehouse. This means property funds are often prepared first and sold second, hence the need for bridging capital.

In addition to distributions, APN's co-ownership strategy adds the possibility of additional profits from property gains, which have been free flowing over the last five years. But with that comes the risk of losses. The falling interest rate cycle has been a tremendous tailwind. But one only needs to review the losses of the post-GFC period to be reminded of this strategy's downside.

Investments

If APN's asset base is just a sausage factory for new funds, then why does it continue to hold large investments in established funds?

| All figures AUD$m | Value | % of total assets |

| Industria REIT (ASX:IDR) | $52.9* | 40% |

| APN Asian REIT | $1.0 | 1% |

| APN Property Plus | $2.6 | 2% |

| APN Development Fund No 2 | $1.2 | 1% |

| APN Steller Developer Fund | $2.6 | 2% |

| APN AREIT Fund | $0.2 | 0% |

| APN Retail Property Fund | $9.1 | 7% |

| Investment properties | $24.2 | 18% |

| Cash (adjusted) | $28.9** | 22% |

| Other assets | $15.7 | 12% |

| Total liabilities | $26.9 | |

| Net tangible assets | $111.5 | |

| Diluted shares | 333.89 | |

| NTA per share | $0.33 | |

| All figures 1H17 value, except * market value, ** 1H17 value, less divs paid plus option proceeds Source: Company reports |

||

As Table 1 shows, APN continues to hold $53m worth of Industria (40% of APN's market cap). APN listed Industria in 2013, and it continues to derive fees as the fund's manager. But instead of selling down post-IPO it has only increased its ownership stake since.

You'd think shareholders would be better served if this capital was used to create new funds instead of sitting idle in established ones.

The answer could be due to the subscale state of APN's funds management business. As we are about to discuss, it isn't exactly spewing cash, so receiving regular distributions from the co-investments helps to keep the lights on.

The question is, is APN's funds management business going cheap? If we deduct the market value of APN's investments from its market cap, it gives a value of around $23m for the funds management business.

Funds management

APN manages $2.4bn of gross assets across 14 funds. It derives management fees of around 0.60% of gross assets and is also eligible for performance fees.

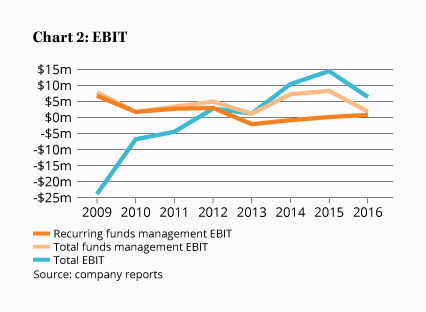

While $2.4bn under management sounds like a lot, APN has struggled to convert it into reliable profitability. It's management and registry fees only just cover its operating costs (as Chart 2 shows with the recurring funds management EBIT line).

Lower interest rates are to thank for the strong profits of the recent past, adding performance fees (see Chart 2, total funds management EBIT) and re-valuations of its co-investments (total EBIT).

But despite a purple patch of performance, it would be a mistake to expect it to continue indefinitely. We think it's best to focus on the recurring management and registry fees. Performance fees become free upside.

With an implied value of around $23m, it seems that the market has it about right.

With a growing cohort of aging investors who need income-producing investments, it's easy to see funds under management growing strongly if management can execute well. But its hard to see a situation where falling interest rates provide another free kick, which encourages us to be cautious.

It's likely that APN is worth more to a trade buyer than it is to ordinary shareholders, as extra value could be added if duplicated costs were removed. So we wouldn't rule out a takeover.

But without a big margin of safety, APN is just one for the watchlist. If we saw a much lower price (below $0.30 has a nice ring to it), or vastly improved business performance, we could be interested.

Until then, we recommend you sit tight, or check out another business on our BUY list.