Aggressive investors: Two case studies

- {{x.value}}

{{ twilioFailed ? 'SMS Code Failed to Send…' : 'Enter verification code' }}

{{ completedStep1 ? 'Authentication & Security' : content.trialHeading.replace('{0}', user.FirstName) }}

{{ content.upgradeHeading.replace('{0}', user.FirstName) }}

The email address you entered is registered with InvestSMART

Please login to continue

We have sent you an email with the details of your registration.

Looks you are already a member. Please enter your password to proceed

{{ upgradeCTAText }}

Updating information

Please wait ...

Your membership to InvestSMART Group recently failed to renew.

Please make sure your payment details are up to date to continue your membership.

Having trouble renewing?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

You've recently updated your payment details.

It may take a few minutes to update your subscription details, during this time you will not be able to view locked content.

If you are still having trouble viewing content after 10 minutes, try logging out of your account and logging back in.

Still having trouble viewing content?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

Please click on the ACTIVATE button to activate your Intelligent Investor 15-day free trial

Please click on the ACTIVATE button to finalise your membership

Unsuccessful registration

Registration for this event is available only to Eureka Report members. View our membership page for more information.

Registration for this event is available only to Intelligent Investor members. View our membership page for more information.

- You are already registered for this event.

- This event is already full.

- Please select a quantity for at least one ticket.

- {{ i }}

Forgotten password

Please enter your email address below to request a new password

- Indepth analysis of ASX listed shares

- BUY, Hold and Sell Recommendations

- Ideas Lab

- Special Reports

- Alan Kohler’s Weekend Briefing

- Interviews with CEO’s & top influencers

- Money Cafe and Talking Finance

- Super Advice and Q&A with Ask Alan

‘In theory,’ said the great New York Yankees catcher Yogi Berra, ‘there’s no difference between theory and practice. In practice there is.’ And so, after the first two articles on our new model portfolios, which focused on theory, it’s time we took a look at how it might all come together in practice.

If you haven’t read those first two articles – The first step in building your portfolio and A dance through the financial aspects of risk – it would make sense to do so first. In this article and the two that will follow, we’ll explore six case studies. We’re going to start with our two most aggressive candidates. Next week we’ll look at our two most conservative profiles and then finish off with the pair in the middle.

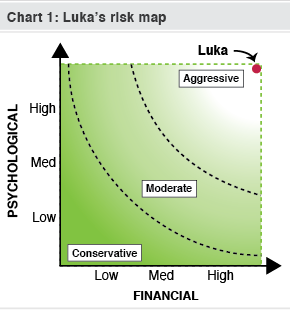

Luka stands at the frontier

Let’s start with our most aggressive investor: Luka. He’s an up and coming executive in one of the world’s largest software companies. To put it mildly, Luka has high hopes for his future career and financial position.

His plan is to join a Silicon Valley start-up over the coming few years and receive a bunch of share options. Then he’ll help the company to grow and prosper by utilising his extensive industry experience. It will eventually list on a sharemarket somewhere and he’ll cash out with an eight-figure bank balance.

Luka is relatively young (in his early 30s), single with no dependents and doesn’t own his own home. Using the terms we coined in A dance through the financial aspects of risk, he has a lot of human capital and very little financial capital.

He wants a shot at ending up mega-wealthy even if it means risking a bad retirement outcome. So he invests his superannuation as aggressively as possible. From a psychological perspective, he’s used to seeing his financial situation wax and wane dramatically from year to year. His first investment was in a basket of technology stocks back in 2000 when he first started working in the industry. So he understands the downside of high-risk sharemarket investments and is prepared to accept it.

Chart 1 plots Luka’s situation on the risk map presented in our previous article. You can see that he’s a ‘frontier’ investor – lying as far out in the top right of the map as you can get.

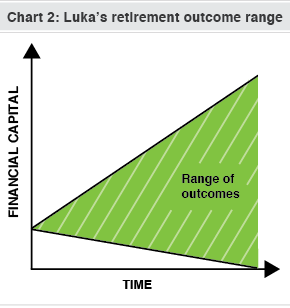

Chart 2 illustrates the risk Luka is prepared to accept in a different way. The vertical axis plots financial capital and the horizontal access represents time: the far left-hand side being today and the far right-hand side being his potential position at retirement. You can see that on the right-hand side, Luka faces an extremely wide range of potential retirement outcomes.

If his aggressive investments pay off, or if he manages to strike it rich with a lucrative share option scheme, he might end up on easy street. But he risks a rather grim outcome if his aggressive investment strategy proves unsuccessful.

In summary, from both financial and psychological perspectives, Luka is the epitome of an ultra-aggressive investor.

Aggressive Angela

Still at the aggressive end of the scale is Angela, a 60 year old professor with tenure at one of Australia’s largest universities. Not only does her position offer an extremely high level of income stability – meaning her human capital is quite high even though she’s 60 – but she has the safety net of a generous defined benefit pension scheme. In addition to this, she has been making contributions into her own self-managed superannuation fund (SMSF) for the past nine years.

From a psychological perspective, Angela is a natural contrarian. She found herself getting excited as share prices fell sharply in 2008 and early 2009 and continued buying shares through that period.

Angela owns her own house and feels financially secure with her defined benefit fund offering a comfortable, guaranteed retirement income. Yet the balance of her SMSF is still well short of allowing her to finance her long-held dream: to spend her 70th year on the planet travelling abroad and staying in the world’s finest hotels.

Knowing she has a good safety net in her pension, Angela is prepared to invest her SMSF aggressively to give her a shot at funding her dream in 10 years’ time. She’s figured out that an average return of more than 12% each year for the next decade will be required to achieve her dream retirement balance and she knows that in order to have a realistic chance of hitting such an ambitious number, she must accept the possibility of much lower – or even negative – returns.

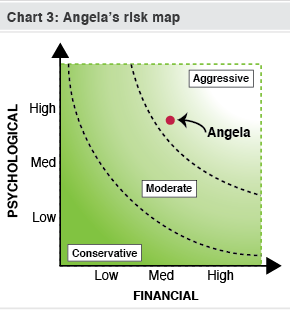

Chart 3 plots Angela’s position on the risk map. When it comes to her SMSF, she’s not as aggressive as Luka but she’s still comfortably in the top right of the map.

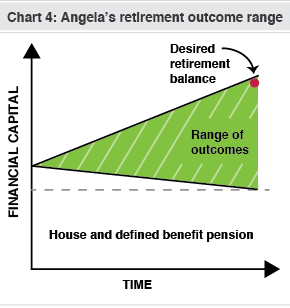

Chart 4 describes the variability of her retirement outcomes. You can see the solid base provided by her house and defined benefit pension – so the variability of outcomes from aggressively investing her SMSF sits atop a firm financial foundation.

Summary

It may seem counter-intuitive that our two most aggressive investors are at quite different life stages. Angela is almost 30 years older than Luka and we often think of academics as conservative by nature. Indeed, without the safety net of her house and pension, Angela would no doubt be much more conservative with her SMSF.

Yet a combination of her sound financial safety net, decent level of remaining human capital, lofty retirement aspirations and naturally contrarian bent clearly places her in the aggressive category when it comes to investments in her SMSF.

These positions aren’t set in stone, though. Let’s imagine that Angela’s SMSF managed to achieve a 20% annual return over the next five years, putting it within easy reach of her goal. In that case, she might become quite conservative – placing a lot more of her fund into predictable investments like term deposits to ensure her dream doesn’t slip away.

Angela’s psychology could change, too. Perhaps when she’s 65, she’ll be more perturbed by market fluctuations than she was in the GFC when she was closer to 55. In that case, she’d need to re-examine her goal and whether it is appropriate. Perhaps she might aim to only travel for six or nine months rather than the originally-hoped-for 12.

Luka, meanwhile, might settle down and start a family, perhaps leaving less of his future earnings to shore up his retirement assets if his investments don’t go to plan.

Such changes open up the topic of ‘asset allocation’, or getting the balance between asset classes right. It’ll be a key topic of discussion once we work through our six case studies and will set the decisions made in our three model portfolios (launching in May – don’t forget) in more context.

For now, we hope you’re developing a good feel for how your tolerance for risk is determined by a combination of your psychological disposition and your human and financial capital. In our next article, we’ll slide right to the other end of the spectrum and look at a couple of case studies for conservative investors.