AFIC: turning a big ship

Recommendation

- {{x.value}}

{{ twilioFailed ? 'SMS Code Failed to Send…' : 'Enter verification code' }}

{{ completedStep1 ? 'Authentication & Security' : content.trialHeading.replace('{0}', user.FirstName) }}

{{ content.upgradeHeading.replace('{0}', user.FirstName) }}

The email address you entered is registered with InvestSMART

Please login to continue

We have sent you an email with the details of your registration.

Looks you are already a member. Please enter your password to proceed

{{ upgradeCTAText }}

Updating information

Please wait ...

Your membership to InvestSMART Group recently failed to renew.

Please make sure your payment details are up to date to continue your membership.

Having trouble renewing?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

You've recently updated your payment details.

It may take a few minutes to update your subscription details, during this time you will not be able to view locked content.

If you are still having trouble viewing content after 10 minutes, try logging out of your account and logging back in.

Still having trouble viewing content?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

Please click on the ACTIVATE button to activate your Intelligent Investor 15-day free trial

Please click on the ACTIVATE button to finalise your membership

Unsuccessful registration

Registration for this event is available only to Eureka Report members. View our membership page for more information.

Registration for this event is available only to Intelligent Investor members. View our membership page for more information.

- You are already registered for this event.

- This event is already full.

- Please select a quantity for at least one ticket.

- {{ i }}

Forgotten password

Please enter your email address below to request a new password

- Indepth analysis of ASX listed shares

- BUY, Hold and Sell Recommendations

- Ideas Lab

- Special Reports

- Alan Kohler’s Weekend Briefing

- Interviews with CEO’s & top influencers

- Money Cafe and Talking Finance

- Super Advice and Q&A with Ask Alan

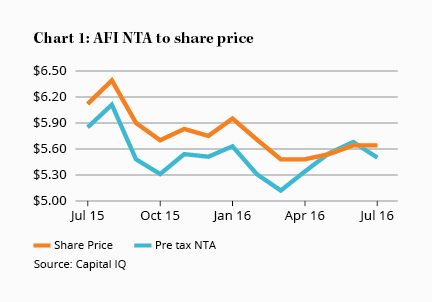

Listed investment company (LIC) results tend to be a bit of a non-event. If you've kept up with the announcements on net tangible assets (NTA) you'll know how an LIC has performed through the year. On the basis of Chart 1, we could tell that Australian Foundation Investment Company's 2016 performance was going to be down on last year.

Key Points

-

Increased dividend

-

Negative portfolio return

-

More exposure to smaller stocks

The portfolio, including dividends, suffered a 1.6% loss for the year, falling short of the S&P/ASX 200 Accumulation Index, which returned 0.6%. AFIC announced a 14 cent fully franked dividend today, taking total dividends for the year to 24 cents – 1 cent more than last year. The management expense ratio remained low at 0.16%, in line with last year's costs.

More than any of this, though, what caught the attention was an increase in AFIC's weighting in small- and mid-capitalisation stocks, from 15% to 22%, since last year. When you're managing a $6.4bn portfolio and selling larger holdings is likely to incur tax costs, a 7% shift is significant.

Management noted in its outlook statement that subdued returns were ‘likely for quite some time' and, to deliver reasonable growth, they clearly feel they need to take a broader approach. Given the outperformance of small and mid-caps over the past year and more, though, they may have missed the boat – or at least the best cabins.

It takes time to turn such a big ship as AFIC, though, and we expect this process to continue, with the majority of its dividend still coming from income paid by its core holdings, topped up by profits taken on smaller positions.

It takes time to turn such a big ship as AFIC, though, and we expect this process to continue, with the majority of its dividend still coming from income paid by its core holdings, topped up by profits taken on smaller positions.

With such a low management expense ratio, AFIC remains one of the cheapest ways to get Australian equity exposure, even compared to ETFs. As a result, it's a reasonable option for long-term investors that don't want to pick their own stocks – despite the 6% premium to its current pre-tax NTA of $5.50.

For it to offer value, though – against other stocks (including those it holds) – we'd need to see its share price closer to its post-tax NTA, which currently stands at $4.79. The stock is up 3% since 6 Oct 15 (Hold – $5.67). HOLD.