5 from 15 - ARB Corporation

Recommendation

- {{x.value}}

{{ twilioFailed ? 'SMS Code Failed to Send…' : 'Enter verification code' }}

{{ completedStep1 ? 'Authentication & Security' : content.trialHeading.replace('{0}', user.FirstName) }}

{{ content.upgradeHeading.replace('{0}', user.FirstName) }}

The email address you entered is registered with InvestSMART

Please login to continue

We have sent you an email with the details of your registration.

Looks you are already a member. Please enter your password to proceed

{{ upgradeCTAText }}

Updating information

Please wait ...

Your membership to InvestSMART Group recently failed to renew.

Please make sure your payment details are up to date to continue your membership.

Having trouble renewing?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

You've recently updated your payment details.

It may take a few minutes to update your subscription details, during this time you will not be able to view locked content.

If you are still having trouble viewing content after 10 minutes, try logging out of your account and logging back in.

Still having trouble viewing content?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

Please click on the ACTIVATE button to activate your Intelligent Investor 15-day free trial

Please click on the ACTIVATE button to finalise your membership

Unsuccessful registration

Registration for this event is available only to Eureka Report members. View our membership page for more information.

Registration for this event is available only to Intelligent Investor members. View our membership page for more information.

- You are already registered for this event.

- This event is already full.

- Please select a quantity for at least one ticket.

- {{ i }}

Forgotten password

Please enter your email address below to request a new password

- Indepth analysis of ASX listed shares

- BUY, Hold and Sell Recommendations

- Ideas Lab

- Special Reports

- Alan Kohler’s Weekend Briefing

- Interviews with CEO’s & top influencers

- Money Cafe and Talking Finance

- Super Advice and Q&A with Ask Alan

For me at least, much of the last 15 years can be summed up in two figures. The first – 3 – is the number of kids I have acquired over the period. The second – 486 – is how many Buy recommendations Intelligent Investor made between June 2001 and June 2016. I'm grateful those two numbers are not reversed. Life is tricky enough.

To mark the 15th anniversary of the launch of our model Growth and Equity Income portfolios and our latest recommendations report, each fortnight over the next few months I'm going to examine a recommendation from the period.

Key Points

-

It's often worth paying up for good businesses

-

Use deep research to get comfortable with high multiples

-

Don't let good stocks go too easily

This isn't an exercise in boosterism, although analytical team members past and present should feel proud of their contribution to our 3.7% annual outperformance of the All Ordinaries Accumulation Index.

It won't just be winners, though; we'll also be looking at two of our biggest ever losers. The real purpose is to show how value investing works in practice, from the demands it places on your analytical skills to the psychological turmoil Mr Market can induce, and how to overcome it.

Each recommendation is its own journey, full of bumps, breakdowns and satisfying vistas. We hope sharing some of the high and lows of a few memorable trips will be enlightening. Let's start with a company originally recommended over a decade ago and sold, slightly controversially, in 2013.

Car parks and carpets

In the midwinter of 2004, analyst Gareth Brown returned from a Victorian holiday where he'd made a side trip to a company in Melbourne's outer-suburbs. He spoke of a daggy building in a low rent industrial estate and a car park stuffed with dirty off-road vehicles. Inside, the carpets were threadbare, supporting ancient filing cabinets and busted desks. Gareth was impressed.

He'd spent months prior to the visit researching ARB Corp, a manufacturer and distributor of four-wheel drive components founded in 1976 by Tony Brown after an expedition to Cape York. The company was then run, as it is now, by Anthony's brothers Roger and Andrew. By 2003, ARB had increased profits by an average of 29% a year over the previous decade. As Gareth wrote in his first review in October of that year, ‘in compiling a list of excellent businesses, ARB is up there with the best of them'.

Back then return on equity stood at about 26% and had grown in each of the previous five years. The problem was the price. Even though we stated ‘the odds of this company growing its earnings at a good clip for the next decade are good,' a PER of 20 and an uninspiring yield of 2.4% produced a Hold recommendation.

More research followed, along with the company visit. That produced three key insights, the first being the quality of this company's management. ARB was stacked with 4WD enthusiasts and run by highly capable, energised owner managers. To quote the original Buy recommendation: ‘It's a cliché, but for a business to reach its full potential, managers must treat it as a passion rather than as a pay cheque.'

That was ARB down to a tee. Salaries were modest and executive options packages non-existent. At the 2002 AGM, so the story goes, Roger Brown took the leftover sandwiches back to HQ for the enjoyment of his staff. Much as corporate boards might try, you can't buy that kind of commitment.

Second, the company invested heavily in research and development. According to a company profile, management's adage is that ‘if it's not broken, break it anyway and find a better way of making it'. ARB already had a few hits on its hands, including the Air Locker and Old Man Emu suspension kits – the first 4WD accessory to sound like a boutique beer. But the chances of new and better products were high and the market for 4WD accessories was growing. Finally, ARB's typical customer was an enthusiast that appreciated highly engineered, reliable products.

Those three factors were an enticing combination. Good management kept manufacturing costs down, high levels of investment produced great products, and the company's market niche was a large and growing pool of aficionados prepared to pay top dollar. The result was a consistent EBIT margin of 15%, more than twice that of its nearest competitor.

Biting the bullet

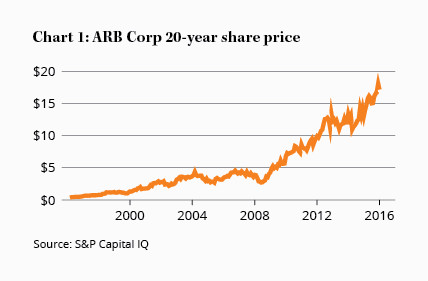

None of this had gone unnoticed. Two years previously ARB shares were trading at around $2. Now they had climbed to over $3.50. We bit the bullet anyway, calling ARB a Long Term Buy at $3.53 on 19 Aug 04.

Our confidence was immediately tested with the stock registering a 25% loss over the next 18 months to $2.66. But having done the work, we were comfortable with the stock and continued to recommend buying. Hopefully members were able to take advantage of the lower prices.

A recovery above $4 followed but the stock again fell below $3 in the midst of the global financial crisis in early 2009. We kept saying buy and that proved to be the best opportunity of the lot, with the share price subsequently embarking on an almost relentless rise to its current level above $17.

We first downgraded to Hold in April 2010 at $6.00, for no reason other than price. We got two more opportunities to buy, in August 2010 and again a year later but that was it. By 21 May 2013 the share price had climbed to $13.49 having met all our expectations and then some.

Trading on a multiple of 22 times that year's earnings, we baulked. Fretting about the potential fallout from the then-looming mining bust, we made our solitary Sell recommendation and removed the stock from our model Growth Portfolio. We should have held our nerve, but you can't have everything.

From beginning to end ARB had delivered a return of 23.9% a year over the decade we owned it. So, what can we learn from this potted history?

1. Deep research pays off

Even a cursory look at ARB's annual reports of a decade ago revealed the company's quality. This was more than a low margin metal basher. The ‘softer' factors were less obvious: the level of commitment among managers; the loyalty of customers and staff; and the quality of its products. It was these factors, not the high return on equity or profit margin, that got us to a point where we were comfortable paying a seemingly high price for the stock.

It's a mistake to think that everything important can be gleaned from a company's accounts. Deep research must also address the softer side of analysis, the art as much as the science – the sandwiches and the car park. Rich rewards await those that make that commitment (or pay someone else to do it for them).

2. It's worth paying up for quality

One of the problems with value investing is that it can lead us to a conventional conception of value. Ben Graham saw cheapness purely in terms of asset value – buying a dollar's worth of assets for 50 cents. Graham's protégé Warren Buffett, however, shifted over the years (much assisted by his partner Charlie Munger) to an approach that focused on high-quality businesses, producing ample cash flows that could be reinvested at high rates of return.

In 2004, ARB, at 20 times earnings, wasn't cheap in the Graham sense. But after getting to grips with it, the Buffett perspective made sense. We paid what looked like a high price but in return got an even higher return. As senior analyst James Greenhalgh puts it: ‘Quality stocks can look expensive for a time but they have a habit of surprising on the upside'. That's been true not just of ARB, but also Cochlear, ResMed, CSL and plenty more. Quality is usually worth paying for.

3. Don't let good stocks go easily

Other team members may disagree but I think over the years Intelligent Investor has had a tendency to let go of good businesses too easily. ARB is a case in point. Having sold out in 2013 at a price of $13.49, we quickly upgraded it to Hold a few months later after a price fall and have stuck with that recommendation ever since, most recently in ARB shifts back into gear (Hold – $17.74). Between those two recommendations the share price rose a further 32%.

Worse mistakes have been made. The All Ordinaries Index returned 27% in the period, so ARB has hardly shot the lights out – particularly since the gains are purely the result of its P/E ratio increasing; earnings have been flat over the period. Still, there's plenty more time to regret our Sell recommendation. As research director James Carlisle put it in our latest review: ‘ARB is being rated at its highest ever because its prospects are as strong as ever.'

That highest-ever rating of around 30 times earnings, though, is hard to stomach. That's why I – having ignored James's recommendation to sell in 2013 – also ignored his latest recommendation to Hold and sold my shares. There's a fair chance I'll regret that, but I'll try not to beat myself up about it. No-one said this was easy.

4. Hang on and enjoy the ride

Humans have a tendency towards action, maybe because simply doing stuff is life affirming. Investing is no different. We tend to think of it as buying and selling rather than sitting. ARB proves the value of inactivity, of sitting.

Once you've found a well managed, growing company, and you've bought in at a reasonable price, don't get sucked into thinking there's an even better one just around the corner. Overtrading can ruin your returns. Sometimes the next big thing is the stock you already own.

Note: The Intelligent Investor Growth and Equity Income Portfolio used to own shares in ARB Corp and we wish they still did.

Disclosure: The author used to own shares in ARB Corp and will probably wish he still did.

Recommendation