When the thing is not the thing

- {{x.value}}

{{ twilioFailed ? 'SMS Code Failed to Send…' : 'Enter verification code' }}

{{ completedStep1 ? 'Authentication & Security' : content.trialHeading.replace('{0}', user.FirstName) }}

{{ content.upgradeHeading.replace('{0}', user.FirstName) }}

The email address you entered is registered with InvestSMART

Please login to continue

We have sent you an email with the details of your registration.

Looks you are already a member. Please enter your password to proceed

{{ upgradeCTAText }}

Updating information

Please wait ...

Your membership to InvestSMART Group recently failed to renew.

Please make sure your payment details are up to date to continue your membership.

Having trouble renewing?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

You've recently updated your payment details.

It may take a few minutes to update your subscription details, during this time you will not be able to view locked content.

If you are still having trouble viewing content after 10 minutes, try logging out of your account and logging back in.

Still having trouble viewing content?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

Please click on the ACTIVATE button to activate your Intelligent Investor 15-day free trial

Please click on the ACTIVATE button to finalise your membership

Unsuccessful registration

Registration for this event is available only to Eureka Report members. View our membership page for more information.

Registration for this event is available only to Intelligent Investor members. View our membership page for more information.

- You are already registered for this event.

- This event is already full.

- Please select a quantity for at least one ticket.

- {{ i }}

Forgotten password

Please enter your email address below to request a new password

- Indepth analysis of ASX listed shares

- BUY, Hold and Sell Recommendations

- Ideas Lab

- Special Reports

- Alan Kohler’s Weekend Briefing

- Interviews with CEO’s & top influencers

- Money Cafe and Talking Finance

- Super Advice and Q&A with Ask Alan

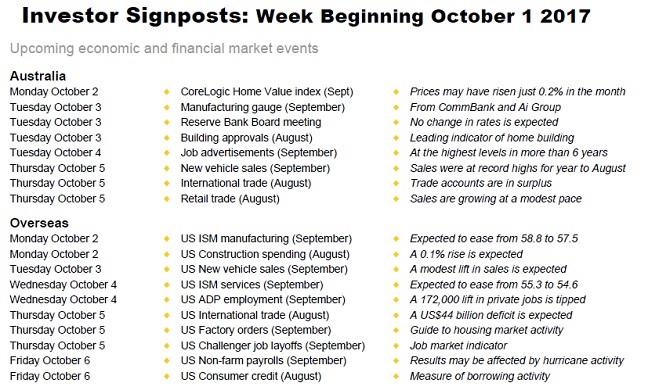

Investor Signposts (by Craig James, CommSec)

Readings & Viewings

One night in 1975, Australian psychologist Don Thomson found himself at the centre of the very problem he was researching. A day after appearing on national television, where he enlightened his audience on the unreliability of eyewitness statements, he was charged with assault and rape.

His alibi was good. Hundreds of thousands of people had seen him on live television at the time of the alleged attack. And one of the people appearing with him on the box that night was an assistant commissioner of police. Still, the officer taking his statement didn't buy it: “I suppose you've got Jesus Christ, and the Queen of England, too.”

Investigators eventually worked it out. The rapist had attacked the victim as she was watching Thomson on television. She had confused his face with that of her assailant. Thomson was released, no doubt more convinced of the veracity of his experiment's conclusions.

Research into the unreliability of eyewitness reports supports the notion that seeing and believing have less to do with each other than we think.

Psychologists call it misattribution, one of the seven sins of memory. Misattribution occurs when we use information to make inferences about the causes of behaviour or events, despite there being no link between them.

Remember all that fuss in the '90s about false memory syndrome? Well, it turns out that the memory of an event can be influenced merely by imagining it. And the more we imagine it, the more likely we are to believe it to be real (Mazzoni and Memon, 2003).

Language can also influence memory. A 1974 study had participants view films of minor car crashes where nothing broke or shattered. After being asked how fast the vehicles were going when they “smashed” into each other – as opposed to “hit” – participants were more likely to describe speeding and shattered glass they never actually saw.

More serious consequences are reported by the US-based Innocence Project. Between 1989 and 2014, 72 per cent of wrongful convictions were based on eyewitness testimony. As Professor Tim Valentine told The Guardian, "Witnesses' recall can be influenced by information acquired during an investigation. Just repeatedly questioning a witness tends to increase their confidence in both correct and mistaken answers.”

It's a popular misconception – a misattribution in fact – that human memory functions like a computer. Instead, it's malleable and prone to revision following the ‘recorded' events.

If what we see with our own eyes can't be relied upon to recount an accurate assessment of events, imagine what fun you can have misleading people with press releases?

Take the recent decision by Commonwealth Bank to eliminate fees on ‘foreign' ATMs. After several scandals, the bank needed some good publicity. The misattribution was in the bank thinking the average person is just as driven by money as a mortgage broker. Removing the fees looked like a cheap bribe, rather than an act of goodwill, reminding us of a cynical, quid pro quo, money-driven culture.

Broker 12-month share price targets are another example. Novice investors use them to calculate how much they'll purportedly make in a year's time. You can understand their thinking. Brokers are smart and almost every broking house provides them. What would be the point if they were useless?

Here, the misattribution is with the client. The number is useful to the broker because it gets the client to trade, potentially opening the door to more transactions. They've calculated it to be worthwhile, even at the expense of leading clients astray. The misattribution is in the client thinking their interests coincide with those of their broker.

Garry White, chief investment commentator for UK broker Charles Stanley, gives us the honest truth: “We do not issue price targets as we deem them to have too many variables to be accurate, market fluctuation being the biggest driver.”

Once you start thinking about this stuff there's no end to it. Have you ever taken a rising share price as confirmation of your decision to buy a stock a few months previously? That's misattribution. Our decisions will be validated years down the track, when the market has ceased to be a voting machine and become a weighing machine.

At the level of the individual, misattribution is normal and contained. But in the political and economic spheres it can be more damaging.

A study published by the Journal of International Business and Economics in 2012 supports Garry White's argument that emotion plays a far bigger role in investment decisions, concluding that “equity and bill prices are positively correlated to investor mood, with higher asset prices associated to better mood.”

The closing remarks of the paper are especially challenging for believers in the efficient market hypothesis: “Supposing that the individual is rational in his decision (supposition that shapes the neoclassical theory) has been consistently refuted in empirical work, validating the hypothesis that cognition and emotion have direct implications on how the individual decides and allocates his assets.”

Forget rationality – emotion, mixed with faulty memory, is the far bigger driver of markets.

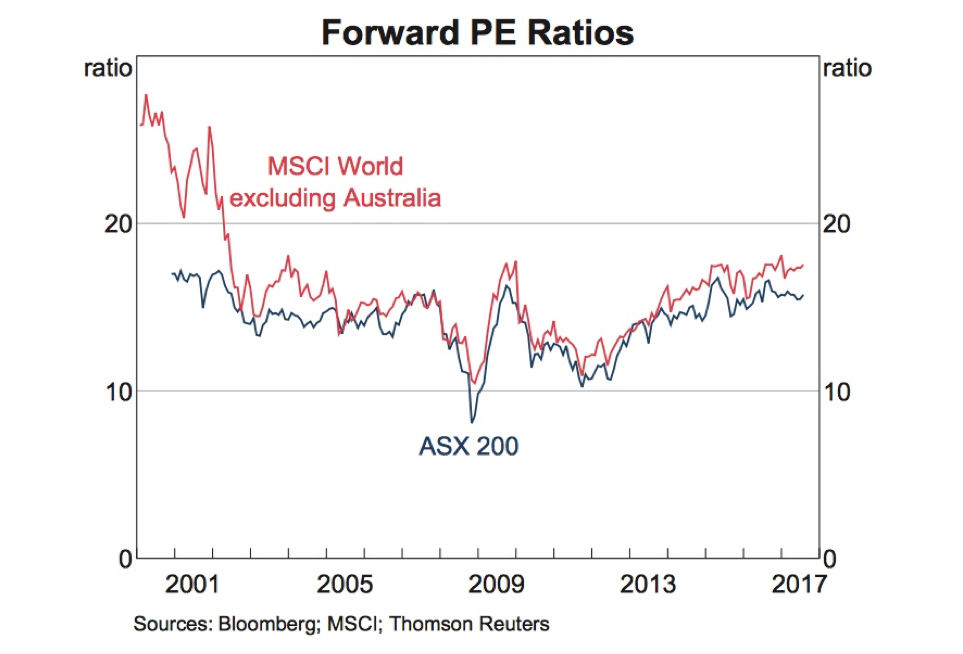

Right now, everyone's feeling very good. Check out this chart, showing the forward price-to-earnings ratio for the ASX 200 and the MSCI (exc. Australia) from the most recent RBA data pack.

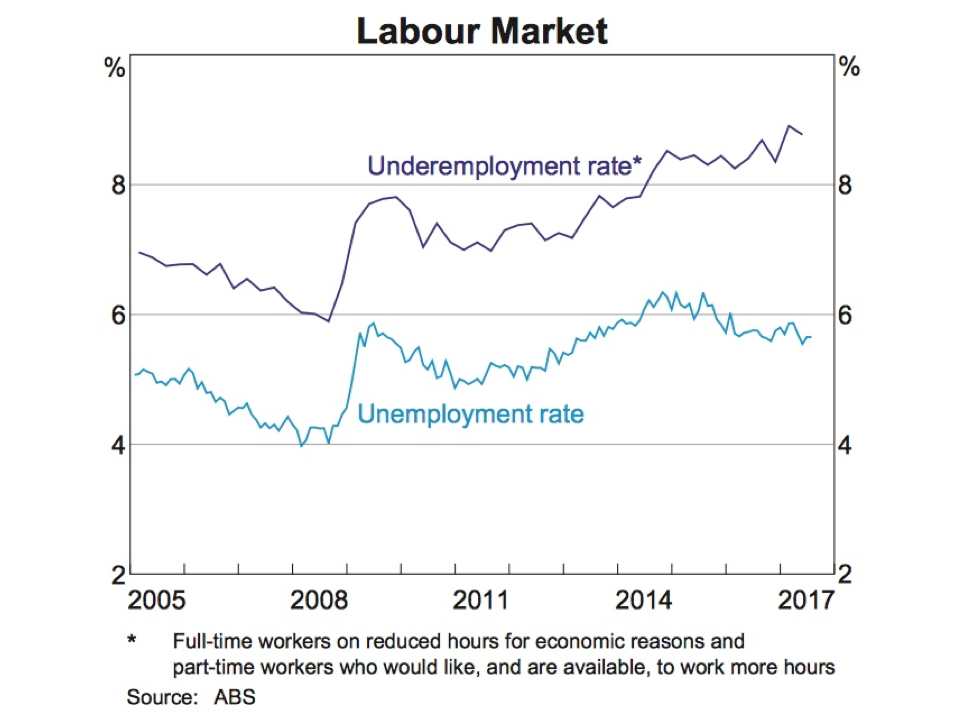

The unemployment rate, or the misuse of it, is another example. The media has schooled us into taking the headline number and drawing conclusions about the general state of the economy. Low inflation, low unemployment, good economic growth? Tick, tick and tick.

But too often we misattribute one number as a proxy for complex social and economic circumstances. The chart below shows the headline unemployment rate (the light blue line) falling in recent years, for which politicians have been eager to claim credit. The purple line above it is increasing, and that's a measure of the number of people with a job but wanting more hours. That's a big problem masked by a single number.

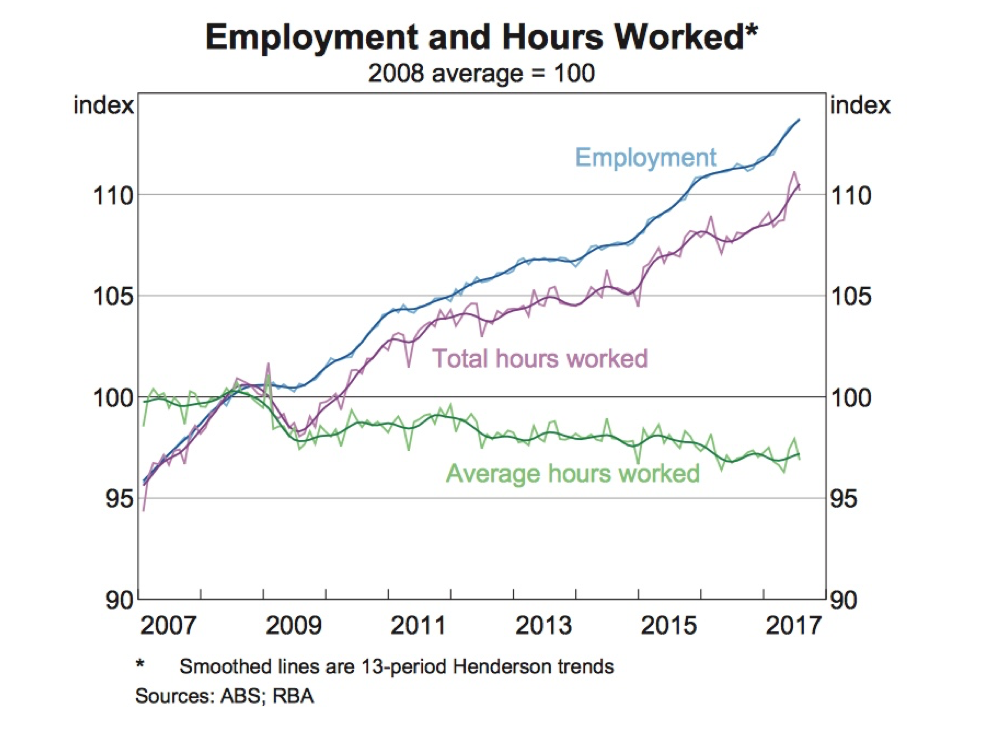

This chart below gives an even better indication. While employment and total hours worked has grown, as you'd expect with a rapidly growing population, average hours worked has been steadily falling. This is a major source of angst, and concern, for those who can't get by on a part-time job. It's a loss of economic output for all – especially when you consider the ABS determines a person as ‘employed' if they work just one hour a week. Nothing in the headline unemployment rate hints at the scope of this problem.

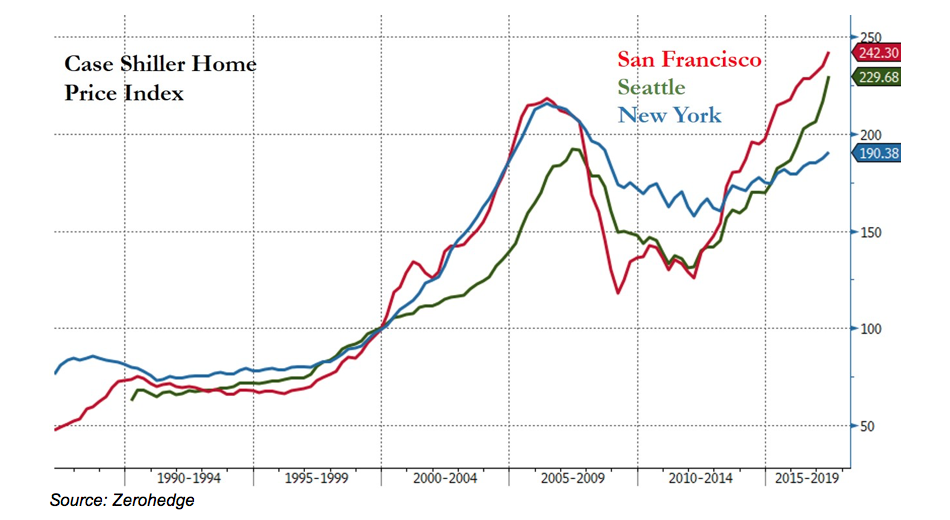

Finally, let's take a quick trip across the Pacific to Seattle, where Loftium is taking advantage of sky-high house prices and rents in the city. The company's business model is premised on a giant misattribution by customers.

Loftium targets potential homeowners that can't scrape together a deposit, which would be almost everyone in Seattle under 40. It contributes $50,000 to a home deposit on the proviso that one room is rented out on AirBnb for 357 days a year, for up to three years after purchase. In return, Loftium takes 30 per cent of the rental, but does provide nice toiletries for guests. Very thoughtful.

Let's pretend this kind of business model has nothing to do with the excesses of pre-GFC USA and look instead at where the misattribution occurs.

The young buyers, many of whom may not recall the last housing market crash – or believe it's different this time because of, err, Amazon – think they're getting a leg up into a rising housing market, the price of which is a tourist in the spare room. Fair enough.

But what they're really getting is a home equity loan at an absurd interest rate that helps a finance company skirt the regulations which were implemented to reduce the risk of another housing market crash.

It's a darkly brilliant model that could be a real winner with the money launderers recently shut out of Commonwealth Bank's intelligent teller machines. Ian, there's an opportunity here somewhere. Get on it.

Enjoy your weekend. Have a bubble tea on me.

Investor Signposts

Rate hikes ahead?

- The Reserve Bank Board meets on Tuesday amidst a number of ‘top shelf' indicators. Some analysts believe that the Reserve Bank could lay the groundwork for a surprise November rate hike. However most believe that rate increases are some way off. The text of the rate decision will determine what outcome is most likely.

- The week kicks off on Monday with the release of home price data – the CoreLogic Home Value index for September. Home price increases have slowed in most capital cities except Melbourne. On current indications the measure of capital city prices may have edged up just 0.2 per cent in September.

- Also on Monday both CommBank and Australian Industry Group will release their surveys of manufacturing activity.

- On Tuesday the Reserve Bank Board meets for the third last time in 2017. No change in rates are expected, But as usual the text of the decision will be closely watched. There are whispers of another Melbourne Cup Day move in rates. But the Reserve Bank Governor continues to stress that a rate hike is still “some time” away.

- On Tuesday, the Australian Bureau of Statistics (ABS) releases the August building approvals data – an important leading indicator of home building. ANZ releases the September job ad count also on Tuesday while the Housing Industry Association releases data on new home sales for August.

- ANZ and Roy Morgan are expected to release the weekly consumer confidence report also on Tuesday.

- On Wednesday both Australian Industry Group and CommBank plan to release their surveys on activity in the services sector.

- On Thursday the Federal Chamber of Automotive Industries releases the September data on new vehicle sales. In the year to August vehicle sales were at record highs, underpinned by sales of sports utility vehicles (SUVs) and utes.

- Also on Thursday the ABS releases both international trade and retail trade data for August.

- In July the trade surplus narrowed from $888 million to $460 million. But the rolling 12-month surplus rose from $12.2 billion to $14.4 billion (biggest surplus in 6 years). And exports to China hit a record $96.2 billion in the year to July. In August the trade surplus may have widened to $1200 million.

- Meanwhile retail trade was unchanged in July after posting average gains of 0.6 per cent a month in the previous three months. Despite the flat result, retail trade stands 3.6 per cent over the year, well above the rate of inflation. And non-food retailing fell 0.5 per cent in July after averaging gains of 0.8 per cent a month in the previous three months. Non-food retail spending is now up 3.4 per cent on a year ago. In August, we expect that bottom-line retail sales rose by 0.4 per cent.

Overseas: US employment data hogs the limelight

- There is the usual raft of statistics for release in the US in the coming week. As usual for the first week in the month, the highlight is the non-farm payrolls (employment) data on Friday.

- In the US, the week kicks off on Monday with the release of both the ISM manufacturing index and data on construction spending. Any reading for the manufacturing index above 50 signifies growth in the sector. In September the manufacturing gauge may have eased from 58.8 to 57.5. And a modest 0.1 per cent increase in construction spending is expected in August.

- On Tuesday, new vehicle sales data for September will be issued alongside the ISM New York index and the usual weekly data on chain store sales. Vehicle sales may have lifted from a 16.14 million annualised rate to 16.16 million in September.

- On Wednesday the ADP national employment measure of private sector payrolls will be released together with the ISM services gauge. Economists tip a more modest 172,000 lift in jobs in September, down from the 237,000 gain in August. The services gauge may have eased from 55.3 to 54.6 in September. The weekly data on housing finance is also issued on Wednesday.

- On Thursday there are a number of indicators set for release. International trade figures are scheduled together with the Challenger series of job layoffs, factory orders and the usual weekly data on claims for unemployment insurance. The trade deficit may have edged up from US$43.7 billion to US$44 billion in August.

- And on Friday, the non-farm payrolls data for September is set for release. While economists tip only a modest down-tick in job creation, down from 156,000 to 140,000 in the month, there is more than the usual uncertainty associated with the data due to the hurricane activity in the month.

- The unemployment rate is expected to be unchanged at 4.4 per cent while wage growth (average earnings) may have lifted by 0.2 per cent in the month. Federal Reserve policymakers will be especially interested in the wage data as another tepid 0.1 per cent increase would reduce the chance of a December rate hike.

- Also on Friday in the US, data on consumer credit and wholesale sales & inventories are scheduled for release.

Craig James is Chief Economist at CommSec

Readings & Viewings

Trump released his tax reform blueprint to much applause in the USA. Two big ticket items were a 15 per cent reduction in the corporate tax rate and a reduction in the top individual tax rate. However, the tax treatment for Trump's greatest friends and enemies – the mega rich – is still yet to be specified. Here's a brief history of how tax cuts for the wealthy have affected the US economy.

It was champagne showers at the top end of town in Silicon Valley, the Nasdaq waking from its slumber to shoot higher on the news. Tax cuts couldn't get former fan favourite Tesla going though, which was battling a left-field attack from British inventor James Dyson. Another thing for Elon Musk to worry about, in addition to working out just how in the world humans will survive on Mars.

Feeling like you have a lot more to say or complain about these days? Now Twitter is giving its users more wiggle room. This can't be good for US-North Korea tensions, and it looks like it's BAU on the Twittersphere for Trump.

Speaking of attacks, Deloitte has become the latest victim of a cyberattack. And after this month's major hack, the SEC is hiring more cybersecurity help after a breach where hackers may have profited from stock trades.

It's pay day for Barack Obama as the former US President turns his luck to Wall Street. Meanwhile, Trump's former communications director is hoping there's money in media as he starts up The Scaramucci Post.

Just do it? Nike just isn't doing it these days, according to analysts, with the company's Jordan brand losing traction. Maybe Nike should lose its tick – ‘ecobranding' multinationals like Nike and the rest of them could be a simple solution to some big problems.

On the matter of problems, whether we're facing a China crisis or not, China's recently released Beige Book is definitely a warning of a ‘darker story' ahead for the economy. It doesn't help that China's anti-pollution drive could also be running out of gas.

“Shocking and illegal” are the words London Mayor Sadiq Khan used to describe his city's pollution levels. Central London commuters who are polluting the most will be slapped with a new tax in October.

There's set to be less cars in the city anyway, with Uber losing its London licence last week. Now Uber is leaving Montreal and winding down one of its core businesses.

Lucky there's only a couple of diamond miners on the ASX considering a 1109-carat diamond was just sold at a huge discount.

Jamie Dimon's JPMorgan Chase is making headlines again, for the wrong reasons. The investment bank has been ordered to pay $US4 billion to the widow of an American Airlines executive.

And lastly, this might be a good weekend read for your millennial daughters.