Week in Review: June 22, 2018

Global shares down on trade tensions, but Aussie shares reach a 10-year high.

Investment markets and key developments over the past week

- The past week saw geopolitics continue to cause gyrations in markets with political tensions around immigration in Germany, and Trump, upping the ante on trade with China. This saw most major share markets fall, particularly in Europe and China, and at the same time emerging markets remained under pressure. Emerging markets were not helped by the rising US dollar which fuelled fears about a dollar funding crisis. Australian shares bucked the global trend though. Safe haven demand saw bonds mostly rally, except in Italy where worries resumed. Oil rose, but metals and iron ore fell, not helped by trade worries. This also saw the Australian dollar break below 74c as the US dollar continued higher.

- Despite the trade war threat, Australian shares rose more than 2 per cent over the last week. The ASX made it to its highest level since early 2008, but is it sustainable? Australian shares have been boosted by a rebound in financial shares, which had become oversold the previous week. Bargain hunters snapped up financial shares for their dividends. We saw a boost to consumer stocks from the passage of the Government's income tax package. We also saw strong gains in defensives and yield sensitive REITs. This has left the ASX 200 on track for our year-end target of 6300 points, assuming our base case of no major trade war is correct. However, the road between now and year end is likely to be rough, with a high risk the trade skirmish gets worse before it gets better. There are worries around Trump, Fed rate hikes, China, emerging markets, and Australian property prices. This is all likely to cause a rough ride. Given that China takes one-third of our exports, the local market would be vulnerable should the trade war escalate significantly.

- Emerging markets under pressure but this is not 1997-98 all over again. From their highs early this year, EM shares and currencies are down around 10 per cent. The plunge reflects a combination of country-specific problems (e.g. Turkey, Brazil and South Africa), concerns that the rising US dollar will cause a dollar funding crisis for emerging countries with significant US dollar debt, and worries they will be adversely affected by any global trade war. Plus, there are concerns about a repositioning, with investors having previously loading up on EM assets – there was a 65 per cent rally in EM shares from early 2016 to early this year. The weakness could have further to go as many of these concerns remain, but it's unlikely to be a rerun of 1997-98, or even 2015, as EM fundamentals around growth and external balances are arguably stronger now and the rebound in the US dollar is likely to be limited.

- Trump's further ramping up of the trade skirmish with China. This means tariffs on $US50 billion of imports, plus another $US200 billion should China retaliate, then another $US200 billion if China retaliates to that. This has significantly increased the risk of a full-blown trade war between the US and China – with a more significant economic impact. So far the bulk of the tariffs are just proposed so there is still room for a negotiated solution, which remains our base case. That is what the US is seeking and China would prefer – otherwise the tariffs would have been implemented already. But there is now a high risk that some of the tariffs go into force before a negotiated solution is reached (which would be a short-lived negative for share markets), even though we still see the risk of a full-blown US-China trade war with deeper share market downside as being low at around a 10-20 per cent probability. Key to watch is the restart of US-China negotiations ahead of July 6. It was noteworthy that central bankers Powell, Kuroda, Draghi and Lowe all raised the threat of a trade war as a significant risk to the outlook, and as a potential downside to interest rates as an implication of that.

- Expect measures to strengthen the Eurozone at its summit on Thursday and Friday, but will it be enough? Progress in this direction has been given a big push by French President Macron and German Chancellor Angela Merkel supports many of his proposals. Expect progress on a banking union, measures to strengthen the European Stability Mechanism, possibly a start to a Eurozone budget, some agreement on an unemployment stabilisation fund, and a strengthening of European Union border control enforcement. Solving the immigration issue is critical if Merkel is to head off a potential split with her Interior Minister, who leads the Bavarian Christian Social Union (CSU), and is threatening border controls around Germany and to keep Italy onside. A split with the CSU would unlikely spell the demise of Merkel or the German coalition Government as Merkel could get support from the Greens. However, Merkel and her party would prefer to retain support from the CSU. A more integrated Europe would be positive for Eurozone assets, including the Euro, but no progress would be bad.

- The Australian Government got a big win with the Senate passing its personal income tax package. However, the impact on consumer spending is likely to be trivial as the tax cuts for low and middle income earners don't kick in until after taxpayers do next year's tax return, following June 2019. They only weigh in around $10 a week, which maybe buys two cups of coffee. Plus, the tax cuts for middle to higher income earners won't be of any significance until next decade and just give back some bracket creep. So a surge in retail stocks on the news may have got a bit ahead of itself.

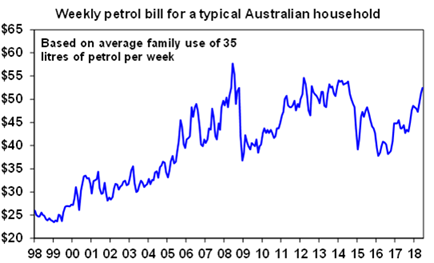

- Along with slow wages growth and falling house prices in Sydney and Melbourne, there are two other drags on Australian households. The drags are rising petrol prices and potentially higher mortgage rates. The rise in petrol prices to around $A1.50/litre has pushed the typical Australian household's petrol bill up by around $12 a week over the last two years.

Source: AMP Capital.

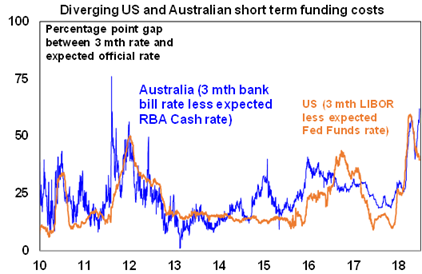

- Short-term bank funding costs continue to rise in Australia pointing to potential upwards pressure on some borrowing costs. While US short-term funding costs have come down, they have risen further in Australia. The reason for the divergence remains unclear but may be related to a desire to lock in funding ahead of the financial year end (after the squeeze into the March quarter end), the Westfield takeover, and regulatory reforms (including the impact of the Royal Commission). Whatever the reason, the longer it's sustained the more it will pressure Australian banks to raise some mortgage rates as banks source 20 per cent of their funding from this source.

Source: Bloomberg, AMP Capital.

Major global economic events and implications

- US economic data remains mostly solid. The Philadelphia regional manufacturing conditions index fell in June but remains very strong. Existing home sales fell but home builder conditions remain strong, housing starts and home prices rose, the leading index rose and jobless claims remain ultra-low suggesting unemployment will head down further towards 3 per cent.

- Japanese core inflation (i.e. ex-fresh food and energy) fell further in May to just 0.3 per cent YoY highlighting the Bank of Japan's ultra-easy monetary policy has a long way to run yet.

- China is cutting taxes to help boost consumption (with 80 per cent of urban workers to benefit), and the State Council signalled cuts to bank required reserve ratios to boost lending to small business.

Australian economic events and implications

- Sydney and Melbourne both slowing. Private sector surveys point to weakness having continued through this quarter. Our assessment remains that Sydney and Melbourne property prices have more downside spread over the next 2-3 years as tighter bank lending standards, rising supply, and deteriorating capital growth expectations impact. Prices are likely to see a total top-to-bottom fall of 15 per cent. Perth and Darwin prices are likely at or close to the bottom; the boom in Hobart may have a bit further to go; and Adelaide, Canberra and Brisbane are likely to see moderate growth. While a house price crash is a risk, continued strong population growth in Australia of 388,000 people last year (led by Victoria) is one reason why this is unlikely.

- Meanwhile, skilled vacancies fell for the third month in a row in May. This suggests employment growth may be slowing (other indicators don't point to this though) and the minutes from the RBA's last meeting added nothing new. Our assessment remains the RBA will be on hold out to 2020, at least. Weak home prices (along with sub-par growth), uncertainty around consumer spending, and low inflation and wages growth are the major reasons for this.

Shane Oliver is the Chief Economist at AMP Capital.

Share this article and show your support