Week in Review: July 6, 2018

The trade skirmish, and a mixed bag of Australian data.

Investment markets and key developments over the past week

- Trade war fears continued to cause nervousness over the last week, weighing on Chinese, Japanese and Asian shares generally, but US and Eurozone shares rose partly on hopes for a resolution. They were also helped by good data. Australian shares also pushed higher helped by a rebound in Telstra. Bond yields were generally flat-to-down except in Italy where they rose. Iron ore and metal prices fell, as did the oil price due to a rise in oil stockpiles and President Trump's pressure on Saudi Arabia to get prices down. Trump is clearly focused on the mid-term elections and sees Saudi Arabia as owing him a favour given the return of US sanctions on Iran. The US dollar and the Australian dollar were little changed.

- Trade skirmish escalating, and it will likely get worse before it gets better, but still expect a negotiated solution before it gets too bad. The scheduled 25 per cent tariff on $US34 billion of imports started up today, on July 6, and a similar-sized Chinese retaliation on US goods will likely follow. Of course, this along with the tariffs on steel and aluminium still only amounts to tariffs on less than 3 per cent of total US imports – a long way from the 20 per cent Smoot Hawley tariff on all imports in the 1930s. That said, it's not over yet, with much more still threatened, including US tariffs on another $US16bn of imports from China proposed to be implemented soon, two additional $US200bn tranches on Chinese goods, and Trump even threatening to put a tariff on most Chinese imports if China keeps retaliating, along with a 20 per cent tariff on auto imports from the EU.

- However, much of this still looks like a negotiating stance, otherwise, all the tariffs would already have started up by now. And Trump knows the costs to US workers (from soybean farmers to Harley Davidson workers) and consumers will escalate as more and more tariffs are imposed and this could become a problem for him if it's not resolved by the mid-term elections. There are also some signs that Europe (or at least Merkel) might be open to negotiating by cutting current EU tariffs on auto imports. Our base case remains that some form of negotiated solution will be reached, but things are likely to get worse before they get better. So far, the Australian share market has proved quite resilient in the face of trade war fears, partly because Australia is not directly affected. However, it will become vulnerable should trade wars pose a threat to global growth as that would reduce demand for our exports.

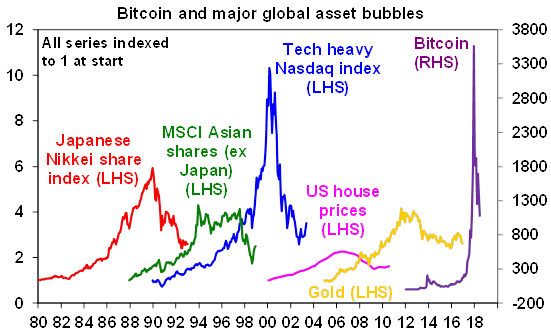

- Bitcoin bubble bath. Remember the obsession with bitcoin and the other cryptos late last year? Whatever happened to it? Well, as with many such manias, the bitcoin price peaked last

December at $US19,500 just when everyone including my dog was asking about it and lots jumped on board (my dog tried but I cut off her financing!). Since then it has seen a 70 per cent plunge, almost rivalling the tech wreck, and providing another classic reminder to be wary of the crowd. Sure, blockchain technology has a bright future but how it's priced into Bitcoin and other cryptocurrencies was always a separate issue.

December at $US19,500 just when everyone including my dog was asking about it and lots jumped on board (my dog tried but I cut off her financing!). Since then it has seen a 70 per cent plunge, almost rivalling the tech wreck, and providing another classic reminder to be wary of the crowd. Sure, blockchain technology has a bright future but how it's priced into Bitcoin and other cryptocurrencies was always a separate issue. - I know Brexit-related negotiations are continuing, but I have tended to ignore it because it's a bit of a soap opera and it doesn't have much impact on global markets. It's really just a UK issue. While British Prime Minister Theresa May could be getting close to a plan (proposing a free market with the EU in goods, but not in services and people) it still has a long way to go within the UK, and it's not clear the EU will support dividing up its cherished ‘four freedoms' – in terms of the free movement of goods, capital, services and people. So, there is a long way to go yet and the Irish border issue also remains a big one. Therefore, it's too early to say the British pound is out of the woods.

- For a really cool mix of Elvis doing Burning Lovewith the Royal Philharmonic Orchestra check here. 1970s Elvis was the best.

Major global economic events and implications

- US economic data remains strong, with the ISM manufacturing and non-manufacturing indices surprisingly rising to very strong levels, construction spending continuing to rise, and jobs data remaining very strong. Meanwhile, the minutes from the US Federal Reserve's last meeting confirmed it remains on track for more rate hikes with strong growth and rising inflation still having the upper hand over trade worries. The Fed is clearly keeping a close eye on the threat to global growth from a trade war, but at this stage it still sees it as a risk rather than its base case. Unlike in 2016 when it delayed rate hikes in the face of global uncertainties, the strength of the US economy today also means the hurdle to slow monetary tightening is much higher now.

- German factory orders rose solidly in May after four months of falls providing some confidence that the slowdown in Eurozone growth may be bottoming out.

- The Japanese June quarter Tankan survey showed continuing strong business conditions and solid capital spending plans, but expectations for inflation continue to run well below the Bank of Japan's 2 per cent inflation target. Meanwhile household spending remained weak in May, while wages growth spiked higher (although it's done this a few times without being sustained).

- Like China's official PMIs for June, the Caixin manufacturing PMI fell slightly but the services PMI rose very strongly. That resulted in a solid gain overall. It's hard to see much of the feared slowdown here, although manufacturing export orders have fallen possibly on trade concerns.

- Meanwhile, India's manufacturing and services PMIs both rose strongly in June pointing to a possible acceleration in growth.

Australian economic events and implications

- Australian data was the usual mixed bag with stronger than expected May retail sales and continuing robust business conditions PMI readings. However, home prices continued to slide in June, building approvals fell again in May, we saw a weak reading for ANZ job ads, and the trade surplus came in smaller than expected with the April surplus getting revised down. There are a few points to note here. First, both the fall in building approvals and the rise in retail sales look to have been exaggerated by volatile components. Second, trade looks to be on track for a flat growth contribution this quarter after the March quarter boost, but fortunately, the consumer looks likely to have perked up in the current quarter, which will help keep the economy growing albeit not as strongly as the RBA is expecting. Finally, we continue to see more downside in home prices, particularly in Sydney and Melbourne where we expect 15 per cent or so top-to-bottom falls spread out to 2020 with a nationwide decline of around 5 per cent.

- Meanwhile, the RBA provided no surprises in leaving interest rates on hold for the 23rdmonth in a row. There are various crosscurrents affecting the economy. We have stronger investment, infrastructure and export volumes, but are still seeing weakness in housing, the consumer, inflation and wages, while banks are also tightening their lending standards. On hold is where wages are likely to remain for a long while yet. We see no RBA rate hike before 2020 and still can't rule out the next move being a cut.

Shane Oliver is the Chief Economist at AMP Capital.

Share this article and show your support