Waiting for Janet, a play on rates

- {{x.value}}

{{ twilioFailed ? 'SMS Code Failed to Send…' : 'Enter verification code' }}

{{ completedStep1 ? 'Authentication & Security' : content.trialHeading.replace('{0}', user.FirstName) }}

{{ content.upgradeHeading.replace('{0}', user.FirstName) }}

The email address you entered is registered with InvestSMART

Please login to continue

We have sent you an email with the details of your registration.

Looks you are already a member. Please enter your password to proceed

{{ upgradeCTAText }}

Updating information

Please wait ...

Your membership to InvestSMART Group recently failed to renew.

Please make sure your payment details are up to date to continue your membership.

Having trouble renewing?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

You've recently updated your payment details.

It may take a few minutes to update your subscription details, during this time you will not be able to view locked content.

If you are still having trouble viewing content after 10 minutes, try logging out of your account and logging back in.

Still having trouble viewing content?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

Please click on the ACTIVATE button to activate your Intelligent Investor 15-day free trial

Please click on the ACTIVATE button to finalise your membership

Unsuccessful registration

Registration for this event is available only to Eureka Report members. View our membership page for more information.

Registration for this event is available only to Intelligent Investor members. View our membership page for more information.

- You are already registered for this event.

- This event is already full.

- Please select a quantity for at least one ticket.

- {{ i }}

Forgotten password

Please enter your email address below to request a new password

- Indepth analysis of ASX listed shares

- BUY, Hold and Sell Recommendations

- Ideas Lab

- Special Reports

- Alan Kohler’s Weekend Briefing

- Interviews with CEO’s & top influencers

- Money Cafe and Talking Finance

- Super Advice and Q&A with Ask Alan

John Addis

Waiting for Janet

Readers might recall studying Samuel Beckett's Waiting for Godot in their formative years. For me, it was a text I was happy to let slide into the hinterland of memory. But this week it re-emerged, thanks to US Federal Reserve chair Janet Yellen.

You may remember the setting. Two blokes are standing under a tree by a country road, waiting for a third bloke – Godot – who never shows. The play caught on because it was so sparse and empty of conventional narrative that meaning could be found whether viewed through a religious, philosophical, social or political lens. Or so I'm told.

Janet Yellen got me thinking about Beckett's play because the prospect of higher interest rates are a bit like Godot; heatedly discussed, subject to interpretation and imminent, maybe. Whether we're about to see a reversal in the 35-year trend to lower rates is the big question for investors.

Rather than higher corporate earnings, economic growth or improved productivity – all of which might justify higher valuations – cheap money has pushed up asset prices. Higher rates might represent a return to normality but they scare the bejesus out of investors worried that asset prices will tumble as soon as rates rise.

That's the situation wracking, or perhaps wrecking, the brains of central bankers, especially in the face of US 10-year treasuries jumping from 1.36 per cent to 1.62 per cent in the last few months. Is this the turning point, the moment when Godot enters stage left?

Deutsche Bank seems to think so. In a recent report it claimed that the next 35 years will be the opposite of the past, a world of lower real growth, higher inflation, lower corporate profits and negative real returns in bonds. Sounds great, right? Bond guru Jeff Gundlach of DoubleLine Capital put it more succinctly, telling Reuters to “sell everything because nothing here looks good”.

On the other side of the argument are people like Charlie Jamieson of Jamieson Coote Bonds, who told Livewire that this was just a healthy correction. “Are we really going into a period where central banks will materially hike interest rates? Absolutely not. Not a chance!"

This week Federal Reserve chair Janet Yellen lined up behind Charlie, voting to leave short-term interest rates unchanged. Called “one of the most divisive FOMC meetings in recent memory”, three of the 10 voting members dissented. That's to be expected. When the committee met last December it flagged four rate rises for the year. Now we're likely to get just one, in December. There were bound to be some hold-outs.

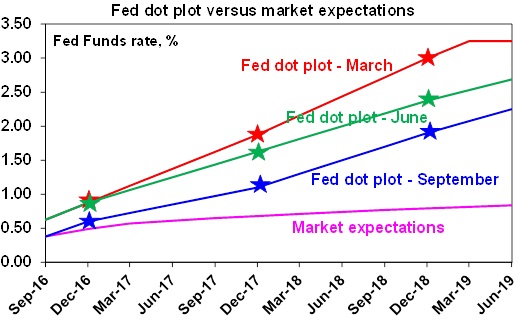

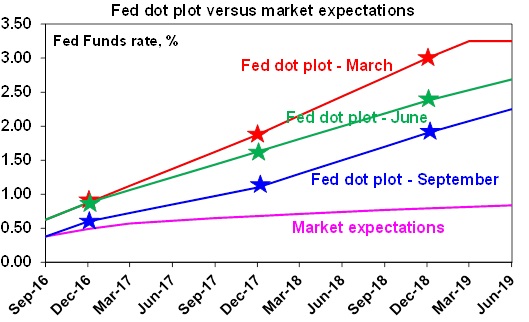

All the signs are that the Fed is sidling up to the market's hive mind. With US growth weak and inflation low, if US rates do rise it's unlikely to be by much. The Fed's ‘dot plot' chart, which marks the projections of each Fed member's view over time, shows how the Fed's expectations of future rates come closer to the market's with each passing quarter.

Economic conditions simply don't warrant much of an increase, despite a genuinely surprising US Census Bureau stat last week that saw a typical US household's income surge 5.2 per cent last year. If true, and there are doubts about its reliability, that's an encouraging reversal of a decades-long trend.

Elsewhere, rates are unlikely to rise at all. Europe remains, well, Europe and in Japan this week stocks jumped when the Bank of Japan said it would be keeping rates steady at minus 0.1 per cent. New Zealand officially cut rates to record lows in August with another cut expected in November. And in the UK the Bank of England has restarted quantitative easing.

About a quarter of the global economy now has negative interest rates, which has allowed countries like Spain, Ireland and Belgium to flog 50 and 100-year bonds, a quite amazing feature of an unprecedented period of economic history. This is an investing environment driven by central bank policy rather than fundamentals, which is why so much attention is paid to the question of if and when rates will rise.

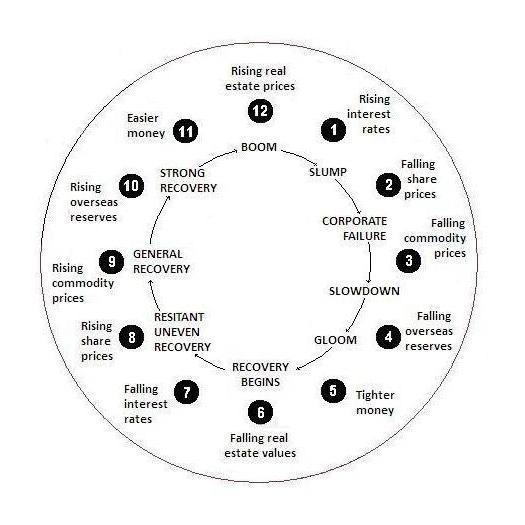

I for one can understand the obsession. When I first started investing 25-odd years ago the economic clock made a bit of sense. But take a look at it now and try and work out where we are in the cycle. Midnight? 7pm? 3am? 8pm? It's all over the place, which is a shame because it's the only thing I remember from three years at uni.

Why has the clock stopped working? Because the traditional boom-bust business cycle has been replaced by an asset price cycle, where the policy response to every looming crisis is lower interest rates. That triggers a reach for yield, lower capitalisation rates and a corresponding boost to asset prices. By now, this should sound familiar, especially to investors in Sydney Airport, Transurban and AREITs (Australian Real Estate Investment Trusts).

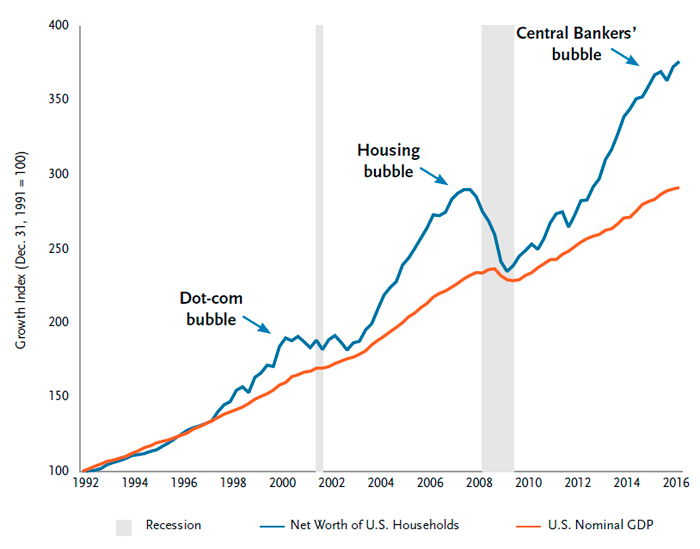

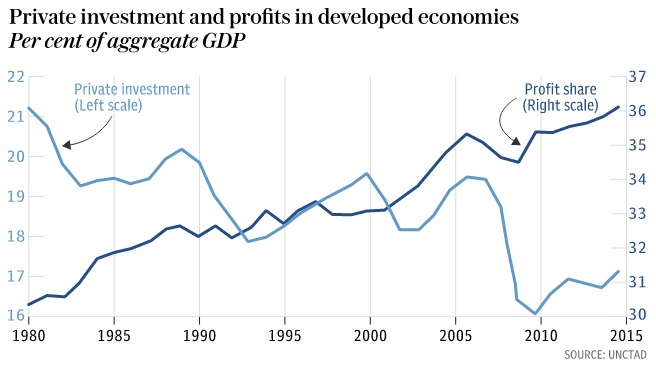

The approach is meant to restore confidence and get companies and consumers reaching into their wallets but that hasn't happened. Instead, we've had a series of asset price bubbles without much impact on GDP. This chart from Bloomberg and TCW shows the US experience but Australia's isn't much different.

It looks like central bankers are guilty of man-with-a-hammer syndrome, seeing no problem that cannot be solved by lower rates. But it no longer seems to be working, maybe because lower interest rates and quantitative easing have saved companies that would otherwise have failed, denying the opportunity for bad debt to be washed from the system. Instead, debt has increased and income stagnated.

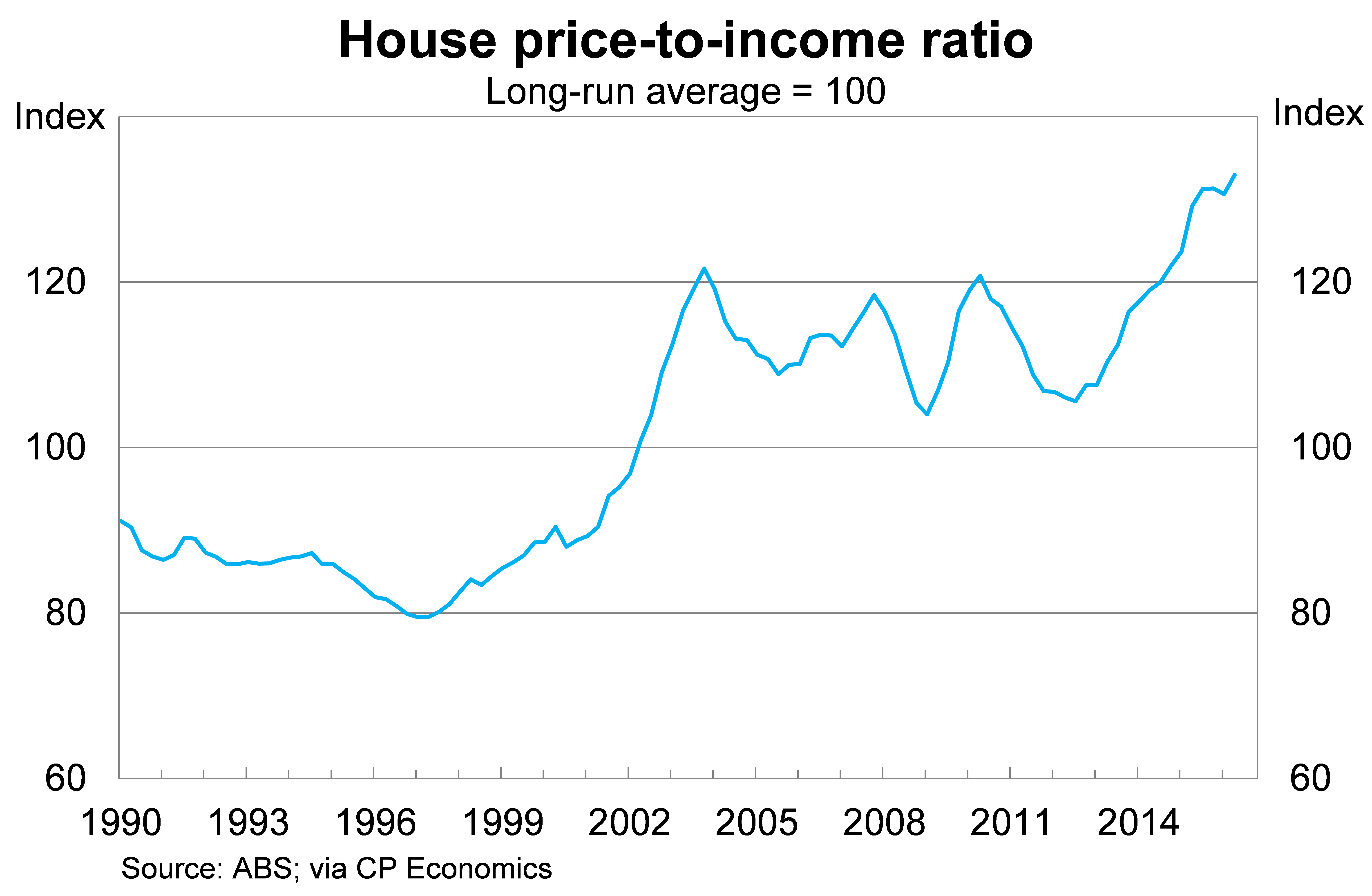

Nor is this a theoretical point. The chart below from Eureka Report economist Callam Pickering shows how Australia's house price-to-income ratio is at its highest ever level. Our kids are struggling to get on the property ladder because we have a tax system that encourages property speculation whilst historically low interest rates have pushed property prices beyond the reach of many.

Central bankers appear to be waking up to the shortcomings of this policy. On Thursday, new Reserve Bank chief Philip Lowe encouraged the Federal Government to take advantage of low rates and borrow up big time to fund infrastructure projects the country badly needs, going as far as to say the additional debt wouldn't impact the cost of borrowing too much. He's not alone in those pleas. Let's hope the worm is finally turning.

All this leaves investors in a bit of a bind. If like me you're sitting on some nice capital gains but want to hang on to them, what should you do? First, let's acknowledge that the interest rate effect has been as strong on share prices as it has property. There aren't many cheap stocks around. In fact, our Buy List features just 11 stocks, the lowest I can remember. Next week we'll be publishing a group of high-quality stocks at reasonable prices that we're happy for members to purchase. Whilst stocks aren't generally cheap, most are not excessively expensive either, especially when compared with the alternatives.

Second, whilst we might worry about the prospect of a local recession, I doubt bond yields are about to rise by much. The Australian economy is also performing pretty well. Resource exports are surging along with tourism and consumer spending. Even Chinese economic growth seems to have settled around 6.5 per cent. So I'm not paying too much attention to those scary media headlines. Like Godot, there's lots of talk around but that's no guarantee of an appearance.

Click here to read this week's Eureka Weekly Review PDF.

Readings & Viewings

Here's a concoction of news stories, interesting articles and videos from the last week.

Let's start with sport, of sorts. While his father, Ken, is known for his mastery of the tennis ball, BBY former chair Glenn Rosewall's preference for the crystal type may have contributed to the stockbroking firm's collapse.

Off the tennis court, and out of the legal courts, the latest set of Boyer Lectures on ABC Radio features Michael Marmot, a London-based health researcher. The Australian-born professor delivers a real eye-opener on how financial stress batters a person's health.

Talking about health, the retail world is the epitome of non-stop stress these days. Just ask Solomon Lew, who must be wondering why Premier Investments fell 8 per cent on Thursday for no apparent reason. But in the US, things must be on the up and up for Wal-Mart, which announced plans to expand with a $US3bn acquisition of retail Jet.com.

But Kmart in the US – unrelated to ours – is shrinking. It announced this week it is closing 64 stores across 28 US states.

In the equally tough political arena, according to US watchers, Seth Meyers is leading his peers on political satire this campaign season. Here's the Late Night host's take on Trump's ‘birther' turnaround.

Meanwhile, the talk among Washington pundits yesterday was about Hillary Clinton's appearance on comedian Zach Galifianakis' spoof-interview show.

And it's been a very tough week for Wells Fargo CEO John Stumpf, who's at the centre of a scandal in which the bank opened unauthorised accounts for thousands of customers. On Thursday Stumpf resigned from an advisory panel to the Federal Reserve.

To grasp a society's deepest tensions, look to its biggest, most popular art form – In India, that's Bollywood.

Citing the graph below, the UN fears the 'third leg' of the world's intractable depression is yet to come...

Google, the global search engine monolith and keeper of all things on the internet, has run into more potential tax troubles. This time, the bill is in the snail mail. Indonesia is set to bill Google for back taxes and fines.

Just when you thought it was relatively safe to do some land grabbing in some distant, third world country, where nobody would notice, think again. CEOs can now be tried for environmental crimes in The Hague.

But, if you do happen to grab some cheap land, say in Ireland, why not ship in a factory? While the shipping world reels from Hanjin's bankruptcy, GE is now shipping whole factories to the Emerald Isle.

We don't know if this is related to the above, but researchers have found a skeleton in the largest ancient shipwreck ever discovered, Greece's Antikythera Shipwreck .

Looking further afield, Elon Musk's SpaceX group says its new spaceship could go ‘well beyond Mars'. Meanwhile, Pluto's icy heart has now been explained.

And then we have Uber, which some in the taxi world would describe as having an icy heart. Now London's taxis are fighting back against Uber – but it's not the one in the UK, it's in Canada.

And happy 66th birthday to Bruce Springsteen, who will be touring Australia shortly. Someone here has supplied a list of his all 314 of his songs in ascending order, with YouTube links to clips. No surprises what's No.1.

Last Week

Shane Oliver, AMP Capital

Investment markets and key developments over the past week

With central bank announcements from the Bank of Japan and the US Fed out of the way and benign, share markets rallied over the last week, bond yields fell sharply particularly in Europe with German bond yields back below zero, commodity prices rallied and the US dollar fell. With the US dollar down and “risk on” the Australian dollar rose above US76c.

The past week has been all about central banks and the news was clearly far better than feared – certainly nothing to support the “out of bullets” fears of a couple of weeks back.

First up, while the BoJ's announcement lacked the “shock and awe” seen in the early days of Abenomics it dramatically ramped up the effort of getting inflation expectations up by committing to overshooting on its 2 per cent inflation target and expanding its monetary base (mainly via quantitative easing) until this is achieved. In other words it's now locked into quantitative easing indefinitely. And in an effort to help Japanese banks, it committed to preventing a flatter yield curve. The BoJ also stressed it's not out of options for additional action. I remain sceptical that without the adoption of “helicopter money”, the BoJ will continue to struggle to meet its inflation target, particularly with the yen remaining around 100 to the US dollar. But the BoJ's announcement was more aggressive than investors expected and is a long way from the central bank surrender that some had feared.

While the Fed was on hold as expected, perhaps the big surprise was that its comments were only mildly hawkish. On the one hand it judged that the case for a rate hike has “strengthened” and that the risks to the economic outlook are now “roughly balanced” and there were three dissents in favour of a rate hike. On the other it is still waiting for more evidence of progress towards its objectives, chair Janet Yellen repeated that the Fed can more effectively respond to rising inflation than to falling inflation as a reason for caution, the Fed continues to refer to only “gradual” increases in interest rates and the Fed's “dot plot” of Fed meeting participants' interest rate expectations continues to decline. The dot plot is now showing just one hike this year, only two hikes next year and expectations for the long run natural rate have fallen further to 2.9 per cent (from 3 per cent in June).

Source: US Federal Reserve, Bloomberg, AMP Capital

Our base case remains for the Fed to hike at its December meeting, but this will require more consistently positive economic data from the US over the next three months. For sharemarkets the Fed remains broadly supportive, although volatility will no doubt increase again as we get closer to the December meeting.

In Australia, new RBA Governor Philip Lowe and the Treasurer have recommitted to a medium term inflation target of 2-3 per cent by enhancing the flexibility around the target and referencing the importance of guiding expectations. Inflation targeting has been good for Australia and lowering the target as some have suggested would have just lowered its credibility. Meanwhile, emphasising the flexibility around the target highlights that the RBA does not have to mechanically keep cutting just because inflation is below target but by the same token the reference to guiding expectations highlights that inflation needs to come back to target within a reasonable time frame. These two adjustments probably just cancel each other out in terms of what it means for monetary policy in the months ahead. On this front the Minutes from the RBA's last Board meeting and Governor Lowe's Parliamentary testimony were pretty neutral on the outlook for rates. The outlook for low inflation, the upside risks to the Australian dollar as a result of ongoing global monetary stimulus and Fed delays and the need to manage inflation expectations supports our expectation for another rate cut but the solid economic growth outlook and the risk of financial instability, related in particular to the housing sector, argue against another move. So we continue to regard our outlook for another cut as a close call. With Lowe saying that whether another rate occurs is going to depend, among other things, on “what the next inflation data look like”, the September quarter inflation release in late October will clearly be critical ahead of the RBA's November meeting. When asked if the RBA is running out of policy options Governor Lowe responded “not at all”. That said I don't think he will have to ease policy much more anyway.

Finally, the Reserve Bank of New Zealand left official rates unchanged at 2 per cent but retained a clear easing bias and the Bank of Indonesia cut again and remains dovish.

The bottom line is that it's basically more of the same from central banks. They want higher growth and more inflation. More help from governments is desirable but it will take a while. They don't want to upset things given uneven and fragile global growth. Global monetary policy is set to remain easy for some time yet. Which means the broad environment (i.e. beyond short-term event risks) remains positive for shares and growth assets.

Major global economic events and implications

It was another mixed week for US economic data with falls in housing starts, existing home sales and the Conference Board's leading economic indicator but gains in the National Home Builders' Association housing conditions index, home prices and manufacturing conditions in the Kansas region and another fall in jobless claims. It's worth noting though that the weakness in housing starts was all due to the South and weather related and the weakness in existing home sales looks supply related.

Chinese property prices surged again in August. In response many cities are announcing policies to slow it down again. China's MNI business conditions indicator rose in September adding to confidence that Chinese growth has stabilised.

Australian economic events and implications

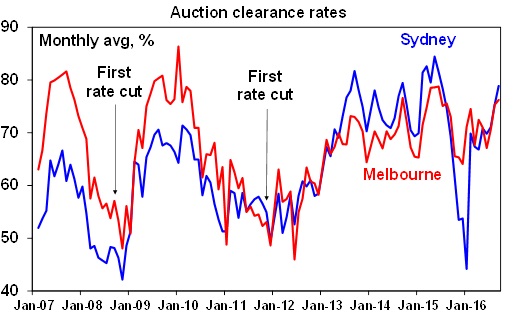

- Australia economic releases were largely second-order over the last week. ABS data showed a further moderation in home price growth over the year to the June quarter to 4.1 per cent, but June quarter growth was 2 per cent plus (or 8 per cent plus on annualised basis) in Sydney and Melbourne which indicates these cities remain too hot. A surge in auction clearance rates suggests they may have become even hotter lately. There is not much the RBA can do, but it is an issue for APRA to keep an eye on.

Source: APM/Domain, AMP Capital

- Meanwhile Australia's population popped 24 million in the March quarter. While population growth has slowed to 1.4 per cent year on year from a peak of 2.1 per cent in 2008 it appears to have stabilised, remains strong compared to most other advanced countries, will help drive reasonable potential economic growth and continues to underpin long term housing demand.

Shane Oliver is head of investment strategy and chief economist at AMP Capital.

Next Week

Craig James, CommSec

Household wealth, job vacancies

The 'top shelf' indicators are still off the agenda in Australia in the coming week. In China the purchasing managers' indexes are released on Saturday. And in the US, a number of key indicators will be released with home prices and economic growth in particular focus.

The week kicks off in Australia on Tuesday, when the ANZ/Roy Morgan weekly consumer sentiment survey is released. Sentiment levels softened in the past week although the four-week average index was down from three-year highs. Overall confidence levels are healthy and no doubt being supported by the improvements in household budgets – all supportive of an improvement in retail activity in coming months.

On Wednesday, the Australian Bureau of Statistics will release figures on engineering construction for the June quarter. Reserve Bank Assistant Governor Malcolm Edey also delivers a speech.

On Thursday the Bureau of Statistics releases the quarterly Financial Accounts. The accounts detail findings such as the cash positions of groups like super funds and families, household wealth levels, foreign holdings of shares and bonds and the value of housing assets (land and dwellings).

In the March quarter total household wealth (net worth) fell by $44.1 billion to $8640.6bn, easing from the record high $8653.8bn in the December quarter.

Also on Thursday, one of the forward-looking indicators of the job market – job vacancies – is also released.

And on Friday, the Reserve Bank releases the financial aggregates publication, a report that includes data on lending (private sector credit) and the money supply. In July private sector credit (lending) rose by 0.4 per cent to stand 6 per cent higher than a year ago. And it is likely that credit rose by a further 0.4 per cent in August, once again driven by owner-occupied housing and business lending.

Overseas: US interest rates hog the spotlight

There is plenty to watch in the US over the coming week. And while there are also key readings on the Chinese manufacturing and services sectors, they aren't released in China until Saturday.

In the US, the week kicks off on Monday, with the release of new home sales data. After the outsized 12.4 per cent lift in new home sales in July, economists expect a 9.1 per cent retracement in August.

On Tuesday the Case Shiller home price index is released in the US together with consumer confidence, and the Richmond Federal Reserve Manufacturing index. Home prices were likely flat in July but should still be up around 5.1 per cent on a year ago. Consumer confidence may have dipped from 101.1 to 99.8 in September.

On Wednesday in the US durable goods orders – a key measure of business spending – is released alongside the regular weekly mortgage finance data. Orders for durable, or long-lasting, goods may have fallen by 1.5 per cent in August.

On Thursday, Federal Reserve chair Janet Yellen participates in a panel discussion. Also, revised US economic growth figures for the June quarter are released. There are three iterations of the economic growth figures each quarter – the advance, preliminary and final estimates. The final estimates for the June quarter are expected to confirm that the US economy grew at a 1.2 per cent annualised pace. The early estimates for the September quarter suggest that the economy picked up to a 2.9 per cent annualised pace.

Also on Thursday, advance readings for US wholesale inventories and trade are released as well as pending home sales. The latter is expected to have eased by 0.3 per cent in August.

On Friday, the University of Michigan's final estimate of consumer sentiment for September is issued, while personal income and spending figures are also released. The final reading on confidence may have lifted from 89.8 to 90. And both personal incomes and spending may have lifted by 0.2 per cent in August.

In China, the official purchasing managers' indexes for both the manufacturing and services sectors are released on Saturday.

Sharemarket, interest rates, currencies and commodities

Over the past two months, oil prices have proved volatile, swinging through a 20 per cent range. In early August the Nymex price dipped below $US40 a barrel to $US39.51. But in mid-August, Nymex crude was pushing up to near $US50 a barrel, settling at $US48.52. Similar – albeit, less extreme – moves have also occurred over September.

In simple terms the world is well supplied with oil. Technological advances have led to a fall in the production costs of what are generally considered higher-cost sources of oil such as shale oil and oil sands. Estimates suggest that operating costs for Canadian producers have fallen by 17 per cent in recent years with costs for some oil-sands producers down by 30 per cent.

Based on estimates from the International Energy Agency and oil analysts, it is estimated that non-OPEC supply will lift by 2.2 million barrels per day in 2016 and a further 1.2mbd in 2017.

In response OPEC producers and notable non-OPEC producers such as Russia are hoping to discuss measures to limit production on the sidelines of an industry conference in Algeria from September 26-28. OPEC Secretary General Mohammed Barkindo has reportedly been quoted as saying there was potential for an oil freeze deal to last at least one-year.

Savanth Sebastian is an economist at CommSec.