Two sides to the Super Guarantee coin

Summary: A war of words has reignited over lifting the Superannuation Guarantee levy from 9.5 per cent to 12 per cent.

Key take-out: The Grattan Institute says lifting the SG will largely benefit higher-income earners, but ASFA says anything else will be condemning Australians to poverty in retirement.

One of superannuation's universal truths seems to be imploding. Looks like it might tear completely off the bone, like a season-ending ACL injury.

The notion that the nation needs to move towards a national Superannuation Guarantee (SG) rate of 12 per cent is under fire.

In the past, the idea has been supported by both sides of politics: the "industry" and, generally, institutions backing workers in looking after their retirements. (Not surprisingly, it has rarely been supported by major employer groups). Now the Grattan Institute, a left-leaning think tank, has produced research that says a lift in the SG rate would do little to increase the retirement incomes of low-income earners, and would largely only benefit higher-income earners – a move that would cost the federal budget billions into the future.

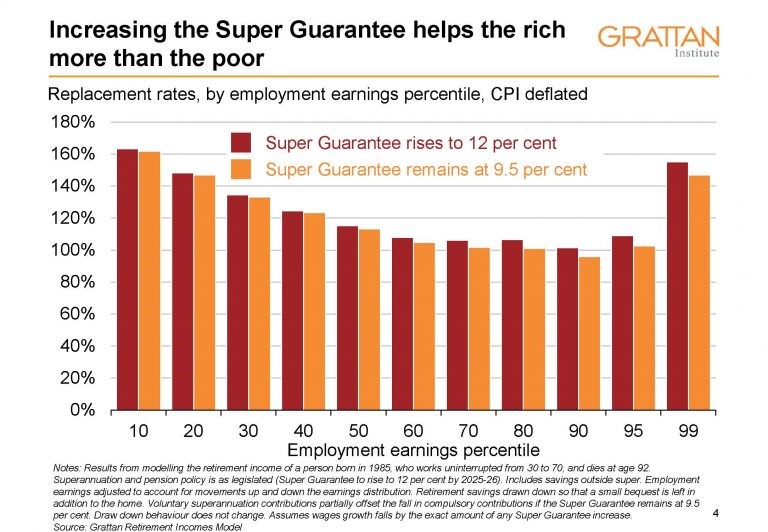

Grattan has illustrated this point with the below graph:

Grattan's research says that Australians who receive compulsory SG contributions for 40 years will actually receive a pay increase in retirement from current superannuation settings, with draw downs from superannuation balances added to age-pension payments and providing more than they received at the end of their working lives.

"If politicians really want to help low-income earners, the planned increases should be scrapped," the institute says.

The planned increases are those that are scheduled to see the current 9.5 per cent rate of SG rise to 12 per cent between now and 2025.

But the Grattan claims have been quickly attacked by the Association of Superannuation Funds of Australia, which says the institute's "aversion to self-sufficiency in retirement posed a danger to current and future generations of Australian retirees.

“This is just another contrived assault by Grattan on our world leading superannuation system. The fact is that the system is delivering significant increases in retirement living standards for all Australians, including low income earners.”

Once the legislated increase in the superannuation guarantee to 12 per cent of salary is introduced, ASFA projects that 50 per cent of Australians will be living comfortably in retirement by 2050, just over double the current proportion.

The end in sight?

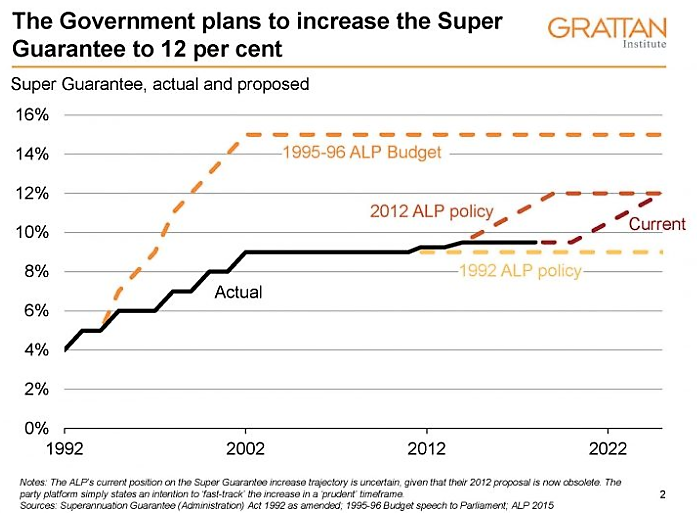

The Rudd/Gillard Governments had set a timetable for that increase that was due to be reached by 2019-20, which was modified/delayed by the Abbott Government. The end target of 12 per cent by 2025 (adopted by Abbott) saw the increases back-ended.

What is currently legislated is that SG will rise from 9.5 per cent to 10 per cent in 2021, then will rise 0.5 per cent a year, to its maximum of 12 per cent, in 2025. And, potentially, leaving it for a future government to further delay. Or cancel completely.

The decision to raise SG to 12 per cent was most likely driven by Treasury, rather than politicians. The ‘argy-bargy' over the timing was politics. Clearly, Treasury wanted to see it lifted to 12 per cent.

In recent weeks, we've also had Financial Services Minister Kelly O'Dwyer, say that increasing the SG rate would be detrimental to worker's wages.

The argument that was rarely spoken of in the 90s, when it came to increases from the original 3 per cent SG rate to the 9 per cent rate that hung around for more than a decade, was that that 6 per cent increase had to be funded by employers, which was no doubt partly funded by lower wage growth over the period.

It now seems to be far more widely accepted that 3 per cent increase in the SG rate from 9 per cent to 12 per cent would probably be offset, at least partially, by lower wages growth over the same period. (Unless, of course, an argument was accepted that a cut in the company tax rate from 30 per cent to 25 per cent would help partially fund that increase.)

This during a time of low overall wages growth. And nothing, in the near future, looking likely to spark it.

He said, she said

So, where does this now sit?

The seed seems to have been planted. By both sides of politics. It may take a while for the seed to germinate, but it is now completely foreseeable that the planned increase in the SG rate might be pushed out further, by a future government, or canned completely.

The Grattan Institute, which comes from the side of politics that you would normally associate with an argument that employers should pay for their workers retirements via SG contributions, is now claiming that an increase to 12 per cent would rob workers of an increase in their salaries of 3 per cent over the next decade. And 3 per cent in their pocket is more important.

What about SMSF owners?

For many self-managed super fund owners, and higher-income earners, the question is a bit of a moot point. SMSF operators are, in the main, more likely to be self-employed and are therefore likely to have control over the level of super contributions they make. And are more likely to make higher than minimum contributions. And are more likely to make catch-up payments, if they can, when they can.

The Grattan Institute argues that a lift to a 12 per cent SG rate would cost $2 billion a year to the federal government's coffers, in reduced tax.

Those that never question the "imperative" of increasing SG from 9 per cent to 12 per cent are, unsurprisingly, the financial services industry, which benefits increasingly from higher funds under management in this legislated sector.

A family affair

Meanwhile, the Government has announced it will increase the maximum number of members of a SMSF. It will probably be formally announced as soon as the Federal Budget next week.

The current maximum number of members of an SMSF is four. About 90 per cent of SMSFS have only one or two members. O'Dwyer has said the number will be lifted to a maximum of six.

While there are some obvious benefits of allowing this, there are also some drawbacks that would come from it also.

If SMSFs were allowed a maximum of six members, then most families would be able to have all of their children join the fund. In some families, mum and dad might be able to invite two kids and their spouses. There would be some cost savings in being able to have bigger SMSFs.

But there would be downsides also. If mum and dad were joined by three or four children, the kids, and potentially their spouses, could outnumber the parents on a vote.

This could be a particular problem when it comes to paying death benefits where there is no binding death benefit nomination in place. If dad dies and wanted mum to receive a reversionary pension, or to be paid the death benefit, a vote could become an issue.

This could, of course, occur under the current rules, where a parent dies and there are two children and the other parent left. But increasing the number to six would potentially exacerbate the likelihood.

Anyone considering this as an option will need to wait until the legislation comes into force. They will probably need to update their trust deeds to allow for it - most SMSF trust deeds will probably only allow for a maximum of four members in the fund.

And in some cases, further legislation might be required by individual states to back this.

The information contained in this column should be treated as general advice only. It has not taken anyone's specific circumstances into account. If you are considering a strategy such as those mentioned here, you are strongly advised to consult your adviser/s, as some of the strategies used in these columns are extremely complex and require high-level technical compliance.