The warning signs you should heed

- {{x.value}}

{{ twilioFailed ? 'SMS Code Failed to Send…' : 'Enter verification code' }}

{{ completedStep1 ? 'Authentication & Security' : content.trialHeading.replace('{0}', user.FirstName) }}

{{ content.upgradeHeading.replace('{0}', user.FirstName) }}

The email address you entered is registered with InvestSMART

Please login to continue

We have sent you an email with the details of your registration.

Looks you are already a member. Please enter your password to proceed

{{ upgradeCTAText }}

Updating information

Please wait ...

Your membership to InvestSMART Group recently failed to renew.

Please make sure your payment details are up to date to continue your membership.

Having trouble renewing?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

You've recently updated your payment details.

It may take a few minutes to update your subscription details, during this time you will not be able to view locked content.

If you are still having trouble viewing content after 10 minutes, try logging out of your account and logging back in.

Still having trouble viewing content?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

Please click on the ACTIVATE button to activate your Intelligent Investor 15-day free trial

Please click on the ACTIVATE button to finalise your membership

Unsuccessful registration

Registration for this event is available only to Eureka Report members. View our membership page for more information.

Registration for this event is available only to Intelligent Investor members. View our membership page for more information.

- You are already registered for this event.

- This event is already full.

- Please select a quantity for at least one ticket.

- {{ i }}

Forgotten password

Please enter your email address below to request a new password

- Indepth analysis of ASX listed shares

- BUY, Hold and Sell Recommendations

- Ideas Lab

- Special Reports

- Alan Kohler’s Weekend Briefing

- Interviews with CEO’s & top influencers

- Money Cafe and Talking Finance

- Super Advice and Q&A with Ask Alan

John Addis

The warning signs you should heed

The first time I saw someone pay more than $5 for a coffee was in 2000. Signs of the dotcom bubble were everywhere, including in the foyer of the old ASX building in Bridge St, Sydney, where punters would gather, transfixed by a big screen showing the ever-rising share prices of LibertyOne, Bourse Data and eCorp.

An enterprising young bloke had set up a coffee bar a few metres away, selling Kopi Luwak for $15 a cup. Yup, fifteen bucks.

This remarkable transformation of the hot beverage value chain was (and still is) made possible by the gut of the Asian palm civet, which eats coffee cherries and excretes them, conveniently, in the form of a Snickers-like chocolate bar. [The confectionary-curious can find the image here.]

An Asian palm civet on learning its poo can sell for up to $US80 a cup

Anyway, those day traders were sucking down the world’s most expensive coffee like they were going out of fashion, which of course they were. Within a few months the dotcom bust had emptied the foyer, except for a few harried souls who, like rubberneckers at a car crash, couldn’t pull themselves away from disaster.

Eleven years later, I stumped up $5.50 for a flat white in Perth. The iron ore spot price was threatening to breach $200 a tonne and coffee bean prices were through the roof, hitting $US300 a tonne (they’re now less than half that). Now, $5 coffees are common, one of the few things, along with energy costs, where prices are going up. Which is a kind of a good thing.

For many years, policymakers have worried more about deflation than inflation. Under deflation, you can buy more with the same amount of money over time. Under inflation, you can buy less. A little inflation is good because it encourages spending. Too much is bad, which is why central banks have inflation targets. But any kind of deflation is bloody awful.

Once people expect prices to fall they withhold spending, knowing that future prices will be lower. That pushes down consumption, output falls, prices and wages fall, workers are laid off, more people default on their debts and a deflationary spiral ensues.

Japan, Australia’s third largest trading partner, has spent 20 years trying to avoid this fate but hasn’t quite succeeded. Despite the Bank of Japan prioritising a 2 per cent inflation target over steady economic growth, it hasn’t had any impact. In June, annual Japanese inflation was just 0.4 per cent. The BoJ, meanwhile, has given up on setting a deadline for hitting its target. Having missed it for years, no one believes them.

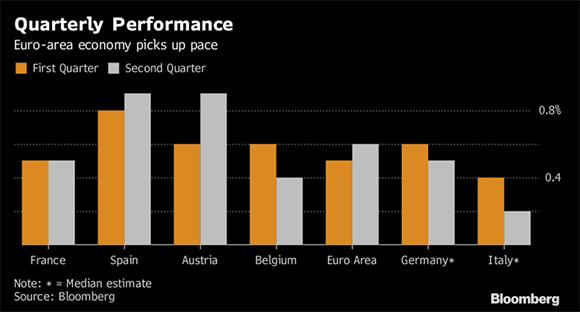

Elsewhere, though, deflationary concerns are easing. In Europe, GDP increased 0.6 per cent in the three months to June. The annual rate of GDP growth is now an impressive 2.3 per cent, higher than in the US. The Eurozone is “steaming ahead”, say Bloomberg.

And last week, Greece got away with issuing $US3.5 billion in five-year bonds at a mere 4.625 per cent. Not bad considering the country defaulted on its debt just five years ago. The hunt for yield is showing up in all sorts of odd places. Eurozone inflation, meanwhile, at 1.3 per cent, is below the ECB’s target of 2 per cent but there’s hope rising employment, higher corporate profits and growing output will eventually lead to price pressures. In the US, that appears to be already happening, to the point where inflation is now a concern, at least for some.

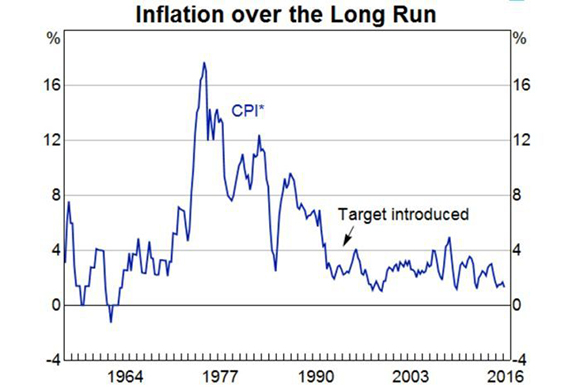

Back in January, Hayman Capital Management founder Kyle Bass, one of the few hedge fund managers to pick the US subprime crisis, said, “Global markets are at the beginning of a tectonic shift from deflationary expectations to reflationary expectations”. Bass expects “significant changes in global fiscal policies along with a continuation of the upward movement of general price levels for consumers and producers alike.” Higher rates, then, to combat higher inflation. This chart offers supporting evidence.

But it doesn’t appear to be playing out as Bass forecast. That dotted arrow heading to the sky has recently fallen back to earth.

Whilst core inflation hit 2.3 per cent in January (the above chart shows headline inflation) it has fallen every month since, hitting 1.7 per cent in May. Oh dear. Fed chair Janet Yellen isn’t worried, despite the fact that this means the Fed will almost certainly miss its 2 per cent inflation target for the sixth year in a row.

Sounds familiar, right? And it is, even here, where core inflation was again well below the RBA’s target of 2-3 per cent, hitting 0.5 per cent in the first quarter. In the last 40 years Australia and almost everywhere else has gone from too much inflation to nowhere near enough.

Source: Reserve Bank of Australia

That means local interest rates are likely to be on hold for a while, which is great news for those engaged in the nation’s leading sports activity – residential property speculation. This week, the Digital Finance Analytics blog unveiled its modelling of mortgage stress to the end of July, suggesting that over a quarter of households (820,000) were in stress and that almost 53,000 were at risk of default in the next 12 months. Gulp.

Recent Reserve Bank data to 27 July might support this finding, showing that the household debt-to-income ratio recently hit an all-time high of 190.4 per cent. The conclusion is obvious: Since the GFC, property investors and homeowners have used record low rates to leverage up even more.

And so, eventually, via a civet’s digestive tract, we get to the point.

This is an odd world in which we’re trying to invest; one where record low interest rates have pushed investors out of cash and bonds and into property and shares. The result is that Australian stocks are priced at a multiple about 20 per cent above their long-term historical average (in the US they’re almost twice the long term average) and households are more indebted than ever.

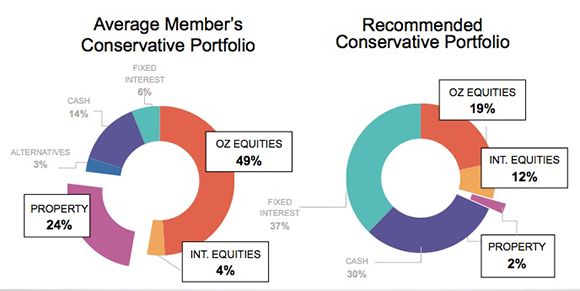

Meanwhile, perhaps because we haven’t had a recession in 25 years, no one seems particularly worried, which worries me. The market has absorbed shocks like Brexit, Trump, ballooning sovereign debt and record low interest rates to the point where volatility is at record lows. The result is an asset allocation that looks something like this:

These figures are from InvestSMART’s free portfolio manager, which maintains the portfolios of 60,000 investors. About 10,000 class themselves as “conservative”, but we’ll get to that. On the left you can see their average asset allocation; on the right InvestSMART’s recommended asset allocation.

The differences are eye-popping. The average member has a 24 per cent asset allocation to property. The recommended weighting? Two per cent. The recommended weighting to Australian equities is 19 per cent and to international equities 12 per cent. The actual weightings? 49 per cent and 4 per cent.

Of course, you can argue with those recommended numbers. But with some of the highest property prices in the world, and the highest personal debt in the world, having a quarter of one’s portfolio in property seems like a giant leap up the risk curve. As for investors actually classing themselves as growth-orientated, they have an average 44 per cent exposure to property.

It looks as though conservative investors are underweight cash, fixed interest and international equities and massively overweight property and Aussie equities. In fact, nearly 80 per cent of their assets are in property and local shares. Gulp again.

I don’t have hard data for the proposition that follows but in recent years I’ve spoken to Intelligent Investor members with 30, 40 and in one case, over 50 per cent of their equities portfolio in the big banks. I’m guessing that a reasonable proportion of that over-allocation to Aussie equities is tied up in the big four.

We’ve long maintained that the big banks should not account for more than 20 per cent of your equities portfolio and, for conservative investors, less than that. But it seems many investors can’t bring themselves to reduce their holdings. As the GFC and Westpac’s 1991 brush with bankruptcy showed, banks can be great investments for decades and then go wrong horribly quickly. That’s not to suggest a crash; merely to recognise the possibility of it and manage that risk accordingly.

This is what record low interest rates and a record-beating, recession-free run have done to conservative investors’ asset allocation. For me, it’s the biggest risk they’re taking and I’m not sure they realise it.

So, while you’re sipping on your five buck coffee this weekend, head to InvestSMART’s portfolio manager (it’s free), bang in your assets and run the portfolio health check to see if you’re really as conservative as you think you are.

Have a good weekend and stick with those Ethiopian beans.

This Week

Shane Oliver, AMP

Investment markets and key developments over the past week

- Share markets were flat to up slightly over the last week. While Apple drove the US Dow Jones index to a new all-time high, the S&P 500 along with Eurozone and Japanese shares were basically flat and Chinese and Australian shares saw modest gains. Global economic and earnings news was generally good but this was in part offset by noise around Trump, risks around US-China trade and with the rising euro weighing in Europe. Bond yields fell, commodity prices were mixed with oil down but iron ore up and the $US slipped a bit further. However, the Australian dollar pulled back a bit helped by RBA jawboning and a lower than expected trade surplus.

- Trump led US-China trade risk up another notch. As we noted a few weeks ago while the risk of a trade war between the US and China went into abeyance during the early part of Trump’s Presidency its now on the rise again partly in response to tensions around North Korea and reflecting a lack of progress in US-China trade negotiations so far. Initially the focus was on steel but it looks to be moving on to a review of China’s perceived violations of US intellectual property which has long been a sore point, which could end in tariffs. Our view remains that cool heads will ultimately prevail but it’s a risk worth keeping an eye on, and one that may escalate if Trump’s political woes continue to mount – even support for Trump amongst his core Republican base is starting to slip a bit so a ramped-up populist “make America great again” campaign around trade could create a useful distraction!

- Consistent with its comments over the last few weeks, the RBA has further ramped up its jawboning against the rise in the Australian dollar. It made no significant changes to its growth and inflation forecasts in its latest Statement on Monetary Policy – still seeing a shift to growth a bit above 3 per cent but with the timing pushed out a bit and revising its headline CPI inflation forecasts up a bit on the back of rapid utility price increases but making no changes to its expectation that underlying inflation will be around 2 per cent. However, it has clearly become concerned that the rising $A poses a threat to both its growth and inflation forecasts. We have been of the view that rates are on hold ahead of a rate hike late next year, but if the Australian dollar continues to trend higher (in contrast to our view for a move lower) it will deliver a further de facto monetary tightening and further push out the timing of rate hikes and may even put rate cuts back on the agenda. Of course, continued strength in Sydney and Melbourne property prices would work in the opposite direction but with the RBA constrained in raising rates to deal with this the pressure will simply fall back on APRA to deliver another round of measures to further tighten property lending standards.

- A couple of things stand out in the latest HILDA - household income and labour dynamics in Australia - report that has tracked roughly 7000 households since 2001. First, despite all the political noise, income inequality (allowing for taxes and welfare) as measured by the Gini coefficient has changed little since 2001. But the main driver of the building angst in recent years has been a stagnation in real median household income since 2009 – which in part can be traced to record low wages growth. When your own living standard is clearly on the rise as it was for most last decade you don’t worry so much about those better off than you are but when you feel like you are stagnating claims about rising inequality start to resonate. Second, homeownership rates for 18-39 year-olds have fallen by roughly 10 percentage points from 35.7 per cent in 2002 to 25.2 per cent in 2014. Of course, this partly owes to changed demographic trends where we start everything later in life (leaving home, leaving full time study, starting work, getting married, etc) and millennial scepticism about the benefits of home ownership and having a mortgage. But poor and ever worsening housing affordability is a big factor & must be addressed if we want to avoid rising social tensions – between the “haves” and “have nots” when it comes to owning a patch of the Australian dream. Trouble is that this issue has been brewing since early last decade and it’s only this year that governments have started to really take it seriously.

Major global economic events and implications

- US data was solid. Business conditions ISM readings slipped in July but along with the Markit PMIs remain solid, pending home sales rose and labour market indicators remain strong. Core inflation in June though remained well below target at 1.5 per cent year on year, keeping the Fed gradual, but at least the previous month was revised up from 1.4 per cent.

- US June quarter earnings results remain strong. Of the 413 S&P 500 companies to have reported 77 per cent have beaten earnings expectations and 68 per cent have beaten on revenue. Earnings look like coming in around 12 per cent yoy, which is almost double the initial expectation.

- Eurozone economic growth picked up in the June quarter to 2.1 per cent year on year, its fastest since 2011 and unemployment fell to 9.1 per cent - which is high but down from a high of around 12 per cent. Core inflation rose in July but only to 1.2 per cent yoy.

- Chinese business conditions PMIs were mixed in July - down slightly according to the official PMIs but with the Caixin manufacturing PMI up slightly and services PMI down slightly. But the moves are neither here nor there and their levels are consistent with GDP growth remaining around 6.5 to 7 per cent.

- Japanese industrial production bounced back in July and is up 4.9 per cent year on year, with business conditions PMIs pointing to reasonable growth ahead.

- The Reserve Bank of India cut its official cash rate by 0.25 per cent to 6 per cent, providing a reminder that major central banks globally are going in different directions with monetary policy. This is consistent with lower inflation. Indian business conditions PMIs also fell sharply in July, although this likely reflects distortions to the timing of spending and confusion associated with the July 1 start-up of the goods & services tax.

Australian economic events and implications

- Australian data was a mixed bag. Business conditions PMIs remained solid consistent with other readings of business confidence. Building approvals bounced strongly in June but this was mainly driven by volatile apartment approvals and a fall in new home sales to their lowest since 2013 suggests that the trend will remain down. Retail sales rose more than expected in June and real retail sales rose strongly in the June quarter providing confidence that GDP growth will bounced back from the softness seen in the March quarter. On the flip side though the trade surplus fell back sharply in June and net exports look to be a flattish contributor to June quarter GDP growth. The Melbourne Institute’s Inflation Gauge showed low inflation in July, whereas I would have expected a higher rise in headline inflation on the back of higher electricity prices, suggesting that underlying inflationary pressures remain very weak.

- Australian home prices continued to bounce back in July after their soft patch in April and May, particularly in Melbourne. While auction clearance rates and investor lending looks to have slowed it’s still not clear that the tightening measures announced earlier this year are having a big enough impact so, given the RBA’s inability to raise interest rates, further action by APRA may still be necessary.

- Finally, it’s too early to draw any conclusions from the start of the June half earnings reporting season as only a few companies have reported. But RIO’s result has confirmed a huge upswing in 2016-17 earnings on the back of the bounce in iron ore and other commodity prices and announced a large dividend hike. That said it came in a little below expectations, so the good news had already been discounted.

Dr Shane Oliver is head of investment strategy and chief economist, AMP Capital

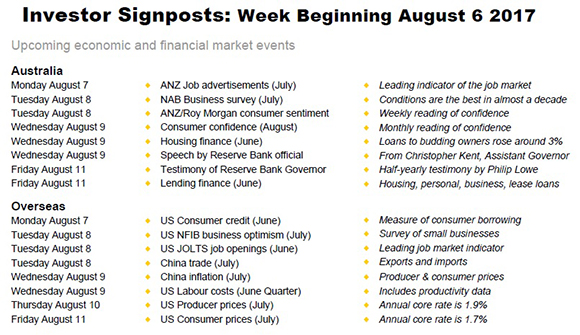

Next Week

Craig James, CommSec

Bevy of indicators set for release

- In Australia over the coming week, a bevy of indicators are set for release covering confidence levels, business conditions and lending. The testimony of the Reserve Bank Governor to the House of Representatives Economics committee on Friday is one of the highlights.

- The week kicks off on Monday with the release of job advertisements data – a key leading indicator of the job market. Job advertisements rose by 2.7 per cent in June to 175,091 ads – a near 6½-year high. Advertisements have been volatile in the past five months but are still up 10.5 per cent on a year ago. And while jobs are now filled through a variety of mechanisms, the job ads data remains instructive.

- Also on Monday there is a Bank Holiday in NSW.

- On Tuesday, NAB releases its July business survey. The business conditions index rose from 10.9 points to a 9½-year high of 15.1 points in June (long-term average 5.1 points). The business confidence index rose from 7.5 points to 9.3 points (long-term average 5.8 points).

- Also on Tuesday, the weekly consumer confidence data from ANZ and Roy Morgan is issued. Consumer spirits have recently been buoyed by the firmer Aussie dollar – raising the appeal of foreign travel and overseas purchases.

- On Wednesday, the Australian Bureau of Statistics (ABS) issues the June data on home loans. The number of loans (commitments) for budding home owners (owner-occupiers) rose by 1.0 per cent in May. And the value of all home loans rose by 1.3 per cent in the month.

- Based on the Bankers Association data, the number of loans may have lifted 3 per cent with the value of loans up 1 per cent. Still, it is important to track the loans actually advanced as cancellations have been rising.

- Also on Wednesday, Westpac and the Melbourne Institute issue the August monthly consumer confidence index. This release is more a check on the weekly confidence survey results.

- The Reserve Bank’s Assistant Governor (Financial Markets), Christopher Kent, also delivers a speech on Wednesday at The Bloomberg Address.

- On Friday, the ABS releases the lending finance data for June. These statistics cover housing, personal, commercial and lease finance commitments – in other words, the broadest measure of new lending in the economy. Total new lending commitments fell by 3.1 per cent in May to a 3-month low. Commitments were down 0.5 per cent over the year. Personal loans were especially weak, down 18.4 per cent on a year ago. In trend terms personal loans were at 14½-year lows.

- Also on Friday the Reserve Bank Governor, Philip Lowe, faces his customary bi-annual grilling from members of the House of Representatives Economics Committee. Depending on the quality of questions posed, the testimony could provide investors with great insights on the direction for monetary policy.

US and Chinese data share equal billing

- There is a good array of both Chinese and US economic data in the coming week with the spotlight largely focussed on inflation.

- In the US, the week begins on Monday with the release of the consumer credit figures – a key measure of household borrowing. In May, consumer credit rose by $18.4 billion – the biggest lift in six months.

- On Tuesday in the US, the National Federation of Independent Business releases its July survey of small business optimism. And on the same day the JOLTS job openings data for June is issued together with the weekly survey of chain store sales.

- In China on Tuesday the July international trade data is released. In June both exports and imports rose at a healthy annual rate. Exports were up 11.3 per cent with imports up 17.2 per cent.

- In China on Wednesday, the July data on consumer and producer prices are released. Producer prices are up 5.5 per cent on a year ago but are off recent highs. Meanwhile consumer inflation is being restrained by softer food prices. Non-food inflation actually stands at 2.2 per cent – a little higher than in other major advanced nations.

- In the US the quarterly data on labour costs and productivity is released on Wednesday.

- On Thursday, July data on producer prices is released with the weekly data on new claims for unemployment insurance. Economists are tipping a 0.2 per cent rise in the core measure of prices (excludes food and energy), keeping the annual rate near 2 per cent.

- And on Friday the July data on consumer prices is released. Similar to producer prices, a 0.2 per cent lift in core consumer prices is expected.

Sharemarket, interest rates, currencies & commodities

- The Australian earnings season cranks up a notch in the coming week. Amongst companies reporting results: SCA Property Group, Transurban, James Hardie and IOOF (Tuesday); Carsales.com, Skycity Entertainment and Commonwealth Bank (Wednesday); AMP, AGL Energy and Magellan Financial Group, Virgin Australia (Thursday); News Corp, REA Group (Friday).

Craig James is chief economist at CommSec.

Readings & Viewings

There’s no denying that the US stock market has rallied strongly since the election of Donald Trump in November. The Trump bump, as it’s known, has seen the Dow Jones hit a record high of 22,000 points – it was at 18,332 on November 8 last year. But as good as that sounds, it’s only the seventh best nine-month run for a US president. See which presidents have done better.

True to his word, Donald Trump has been looking around for better deals for the new Air Force One aircraft. He seems to have found one, in negotiating to buy two 747s built for the Russians.

Meanwhile, this week Boeing used a 787 Dreamliner to perform a unique task. Over 18 hours, pilots traced an outline of the aircraft by flying around the US.

As the US market continued to soar this week, there was one CEO in particular with a lot to lose. Apple chief Tim Cook is on the cusp of a $US44 million performance bonus. But it all comes down to what happens in the coming weeks.

The US IT sector is really powering the market, and even investors in the disappointing Snap IPO now have something to cheer about. And it turns out Google offered to buy Snapchat for $US30 billion last year, but was turned down. Lucky for Google.

Still in the online space, there was lots of news about Amazon this week. The global retail disruptor is hiring, big time. There are new jobs in Australia, and this week the company vowed to hire 50,000 people in the US. Once hired, new employees are being introduced to robots.

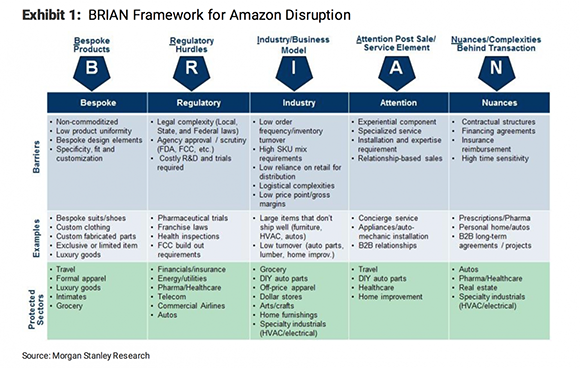

And what about things that don’t need the internet to make money? Investment bank Morgan Stanley wants everyone to meet BRIAN, a framework to gauge how safe industries are from Amazon disruption.

For everything else, there’s 14 Amazon shopping tricks everyone should know. Because, let’s face it, things aren’t always that cheap online, even with the higher Aussie dollar.

On to other things internet, Netflix is down $20 billion, but investors aren’t worried.

Anyway, the best things on the internet don’t make any money. Read this to believe it.

Telsla founder Elon Musk made a brave and unexpected revelation this week when he revealed his bouts of depression. When asked about his life, he tweeted: “great highs, terrible lows and unrelenting stress”.

We think we have a property problem. MarketWatch is educating Americans about why putting down a 20 per cent down payment on property “may be a good idea” — most first home buyers are putting down 5 per cent or less.

But here’s how a frustrated Auckland renter turned his property owning dream into reality, by moving to Melbourne.

As you know, the Australian Government is taxing foreigners who buy property here. But it seems Vancouver’s foreign buyers tax isn’t working.

Canadian alternative mortgage lender Home Capital is hoping Warren Buffett’s capital lifeline and investment magic will kick in very soon. The lender, which suffered a liquidity crisis in April, has just reported a loss of $C111 million from the three months to June 30.

Any ideas on the oldest billionaire in the world? You probably wouldn't guess who.

It was a sad week for the Costco family, with family patriarch Jeff Brotman passing unexpectedly.

This ones for your kids or grandkids. A new book casts doubt on all gifted and talented programs by debunking the idea of a gifted child. Most Nobel Prize laureates were unexceptional in childhood.

‘Designer child’ still conjures up a raft of ethical concerns, but scientists are pretty stoked to have successfully edited genes in human embryos for the first time this week. Despite being a long way from clinical use, human genetic engineering is no longer science fiction.

Wish you knew how to make your favourite dish from your favourite restaurant? Other scientists are working to make this happen, developing a technology that breaks down photos into recipes.

Lastly, we hope to offer a wide range of perspectives every week through these readings and viewings, as we wouldn’t want to be creating any filter bubbles. Like when you have several investment opportunities to assess, it’s important to look deeper into all, rather than just skim the surface.