Market Watch, Nov. 6

- {{x.value}}

{{ twilioFailed ? 'SMS Code Failed to Send…' : 'Enter verification code' }}

{{ completedStep1 ? 'Authentication & Security' : content.trialHeading.replace('{0}', user.FirstName) }}

{{ content.upgradeHeading.replace('{0}', user.FirstName) }}

The email address you entered is registered with InvestSMART

Please login to continue

We have sent you an email with the details of your registration.

Looks you are already a member. Please enter your password to proceed

{{ upgradeCTAText }}

Updating information

Please wait ...

Your membership to InvestSMART Group recently failed to renew.

Please make sure your payment details are up to date to continue your membership.

Having trouble renewing?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

You've recently updated your payment details.

It may take a few minutes to update your subscription details, during this time you will not be able to view locked content.

If you are still having trouble viewing content after 10 minutes, try logging out of your account and logging back in.

Still having trouble viewing content?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

Please click on the ACTIVATE button to activate your Intelligent Investor 15-day free trial

Please click on the ACTIVATE button to finalise your membership

Unsuccessful registration

Registration for this event is available only to Eureka Report members. View our membership page for more information.

Registration for this event is available only to Intelligent Investor members. View our membership page for more information.

- You are already registered for this event.

- This event is already full.

- Please select a quantity for at least one ticket.

- {{ i }}

Forgotten password

Please enter your email address below to request a new password

- Indepth analysis of ASX listed shares

- BUY, Hold and Sell Recommendations

- Ideas Lab

- Special Reports

- Alan Kohler’s Weekend Briefing

- Interviews with CEO’s & top influencers

- Money Cafe and Talking Finance

- Super Advice and Q&A with Ask Alan

Being the first ’full week’ of the month, this is one of the biggest release weeks for economic data. Central banks meet, purchasing manager indices are published, and manufacturing and construction numbers are ready for print.

However, it’s also ’35 days’ since the end of Q3, which means quarterlies such as GDP and employment are also due for release across the world.

Zoning in on Australia, Tuesday’s Reserve Bank of Australia meeting and Friday’s Statement of Monetary Policy (SoMP) are key fixtures of the data deluge. Internationally, all eyes should be on China’s trade balance, which will impact our local market, currency and economy.

RBA meets

The consensus is no change to the official cash rate. The RBA’s view on US rates and economic outlook will inform its view on the currency. Our central bank should also present its view on China’s economy, commodity pricing and net exports. Last, but certainly not least, we’re expecting an outlook for GDP, inflation and housing.

If the Board determines there’s a real slowdown in the last two points – inflation and housing – expect the RBA’s current ‘neutral’ stance to possibly shift to a dovish position.

SoMP release

We’re at the tail end of the data drop for this calendar year. Could the next data releases shift inflation and GDP expectations for 2018 and 2019?

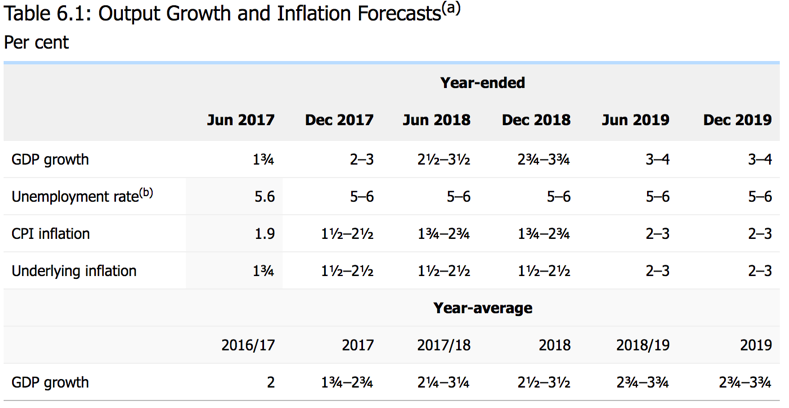

Below is the summary of the previous estimates for inflation and GDP going forward, from the August SoMP release. Note this release marked a downgrade for both GDP and inflation expectations by 25 basis points, or 0.25 per cent.

Source: RBA

The inflation read for Q3 that was released last week, coupled with signs of a slowdown in housing, has been a large backstop of core inflation over the past three years. It wouldn’t be a surprise to see the forecasts slip another notch on Friday.

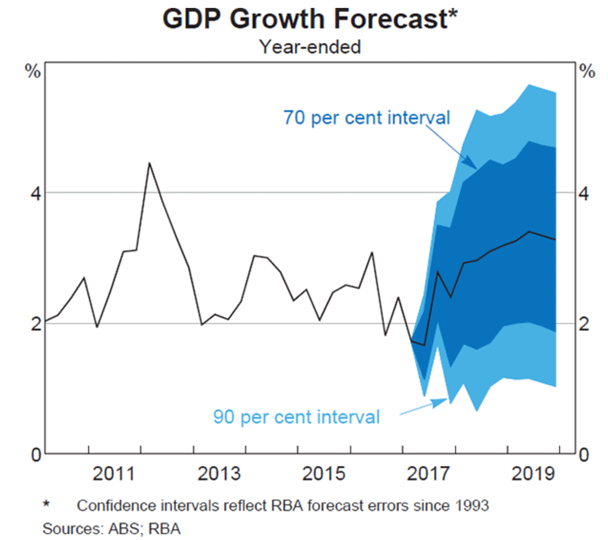

Focusing on GDP, below is the expected GDP growth for Australia out to 2019. Growth has shown signs of green shoots, globally and domestically. The movements in employment and exports lead to an increase in estimates on a sectoral level. Will this allow the macro estimates and the confidence percentiles to shift back to the April levels?

Sources: ABS, RBA

Chinese trade balance

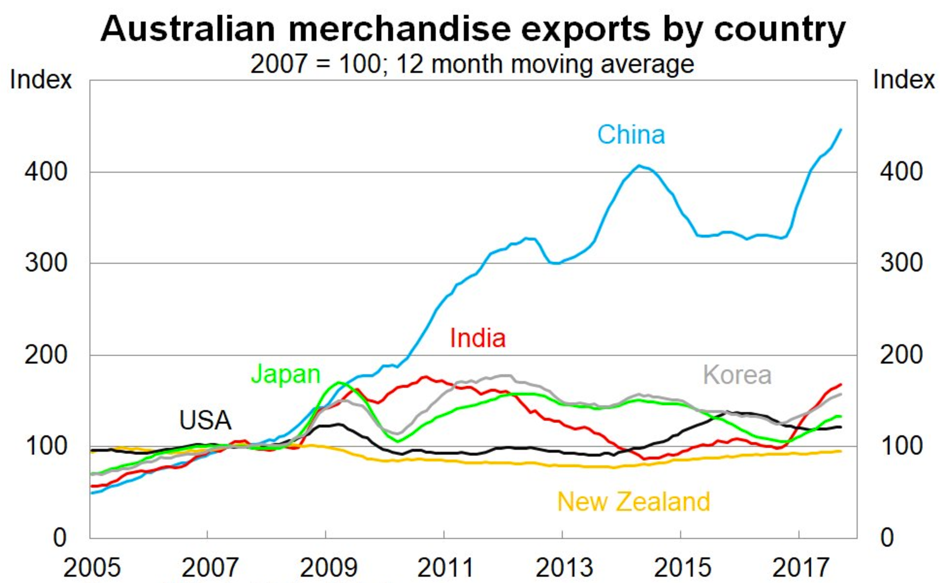

The chart below presents a solid representation of Australia’s relationship to China. The expansion of Australian exports to China over the past 12 years tells that any slide in Chinese imports will filter into Australian GDP and trade forecasts.

Source: ABS

China’s trade balance is forecasted to expand by $US30 billion in this Wednesday’s release. One could assume this increase month-on-month will boil down to a ‘normalisation’ of imports, which in Chinese yuan terms expanded 19.5 per cent versus exports of 8.1 per cent in the month of September.

From the end of September, there were signs a slowdown in trade was well underway. The timing of the National People’s Congress (NPC) caused investment decisions to be halted and there was a concerted effort to slow imports.

The Australian dollar will be the first to react to the headline China trade balance figure. A weaker import figure should cause a slide in the Aussie. However, come Thursday, when the full detail is released, look to the import ledger on a value basis for numbers around iron ore, coal and copper – these figures will filter into the materials sector on the ASX.