Market Watch: Markets chaos explained

- {{x.value}}

{{ twilioFailed ? 'SMS Code Failed to Send…' : 'Enter verification code' }}

{{ completedStep1 ? 'Authentication & Security' : content.trialHeading.replace('{0}', user.FirstName) }}

{{ content.upgradeHeading.replace('{0}', user.FirstName) }}

The email address you entered is registered with InvestSMART

Please login to continue

We have sent you an email with the details of your registration.

Looks you are already a member. Please enter your password to proceed

{{ upgradeCTAText }}

Updating information

Please wait ...

Your membership to InvestSMART Group recently failed to renew.

Please make sure your payment details are up to date to continue your membership.

Having trouble renewing?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

You've recently updated your payment details.

It may take a few minutes to update your subscription details, during this time you will not be able to view locked content.

If you are still having trouble viewing content after 10 minutes, try logging out of your account and logging back in.

Still having trouble viewing content?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

Please click on the ACTIVATE button to activate your Intelligent Investor 15-day free trial

Please click on the ACTIVATE button to finalise your membership

Unsuccessful registration

Registration for this event is available only to Eureka Report members. View our membership page for more information.

Registration for this event is available only to Intelligent Investor members. View our membership page for more information.

- You are already registered for this event.

- This event is already full.

- Please select a quantity for at least one ticket.

- {{ i }}

Forgotten password

Please enter your email address below to request a new password

- Indepth analysis of ASX listed shares

- BUY, Hold and Sell Recommendations

- Ideas Lab

- Special Reports

- Alan Kohler’s Weekend Briefing

- Interviews with CEO’s & top influencers

- Money Cafe and Talking Finance

- Super Advice and Q&A with Ask Alan

It’s the final week of what has been a ‘tale of two halves’ year: a strong bullish start and a volatile bearish end.

This week marks the final ‘full week’ of trading for 2018 and, as luck would have it, three of the top five largest central banks are meeting for the final time this year – the Bank of England, the Bank of Japan and the one that I believe will impact markets the most over the coming 12 months, the US Federal Reserve.

In the past nine to 10 weeks the “perma-bears” would have us believe something in the US and global economy has fundamentally changed – growth is ending a recession is coming.

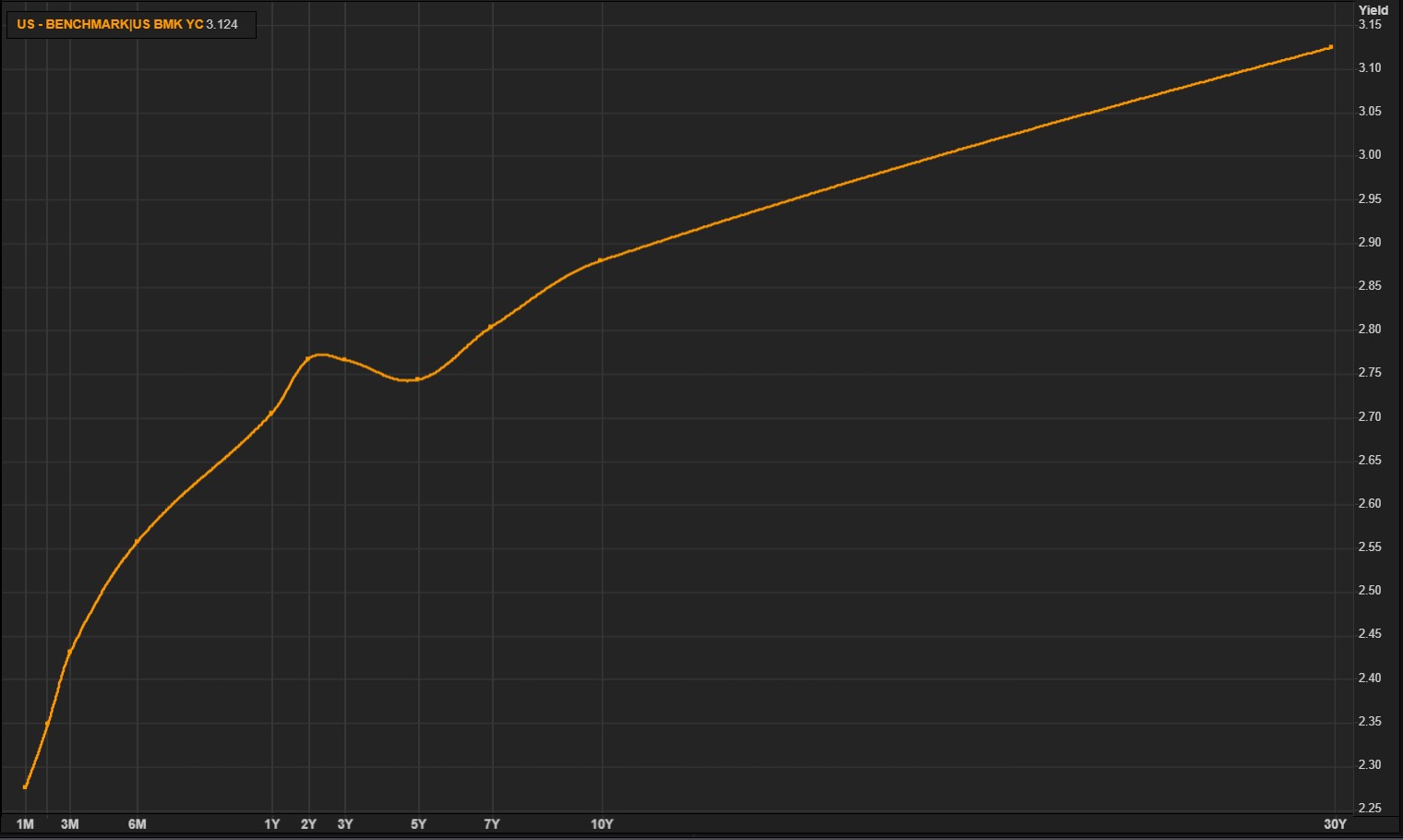

Their justification for this stance is reflected in this chart:

Chart: US Treasury Yield Curve

(Source: Reuters)

That ‘kink’ in the curve is the inversion between the 2-year and 5-year bond yield (this is where the 2-year yield is higher than the 5-year yield) - it is a strong warning sign for markets and recession watchers alike. For the first time in nearly six years, the 2-year-5-year spread has inverted – risk is coming.

However, the real recessions warning sign is the 2-year vs 10-year yield inversion. When this inverts, a recession is coming - history shows a 2-10 year inversion has predicted a US recession every time over the past 40 years. Note, however, that it hasn’t inverted yet but at 15 basis points (0.15%), it’s not far off at all.

This table from Macquarie illustrates what the average time frame is for a US recession once the 2-year-10-year inverts.

(Source: Macquarie)

Thus, where does this leave the Fed, and its rate hike trajectory? Will the spreads in the bond and corporate debt markets make the ‘data dependent’ Fed pause?

I would argue that is unlikely and believe that this Thursday is still a lock for a 25-basis point rate rise.

Here is why:

- Chairman Jerome Powell (Neutral): “Interest rates are still low by historic standards, and they remain just below the broad range of estimates of the level that would be neutral for the economy — that is, neither speeding up nor slowing down growth.” Speech on November 28

- Governor Lael Brainard (Traditional Dove): “The gradual path of increases in the federal funds rate has served us well by giving us time to assess the effects of policy as we have proceeded. That approach remains appropriate in the near term, although the policy path increasingly will depend on how the outlook evolves.” Speech on December 7

- Vice Chairman Richard Clarida (Perma-Dove): “What I want to emphasize... is, at least from my perspective, we’re at point now where we really need to be especially data dependent. The economy is doing well. We’re looking for signals from the labour market, from inflation, to get a sense of both the pace and the destination for policy.” Interview on CNBC on November 16

- Vice Chairman for Supervision Randal Quarles (Neutral): “There’s a range of views on the FOMC about… [the] spread of terminal rates … [which we believe is] somewhere between 2½ and 3½ percent – we are approaching that range. But it is a – it is a range. And where we will end up in that range will depend on the data that we receive and our assessment of the performance of the economy over the course of the next year.” Discussion on December 4

- New York Fed President John Williams (Hawk): “I do expect further gradual increases in interest rates will best sponsor a sustained economic expansion.” Press conference on December 4

All voting members are still of the same opinion. Data is strong, we are not at the neutral rate yet, and there isn’t any indication that rates have become restrictive. The market can be as chaotic as it wants; the data says hike.