Kohler's Week: Why I'm optimistic about 2015 (and why I could be wrong) plus Quickstep and Pro Medicus

- {{x.value}}

{{ twilioFailed ? 'SMS Code Failed to Send…' : 'Enter verification code' }}

{{ completedStep1 ? 'Authentication & Security' : content.trialHeading.replace('{0}', user.FirstName) }}

{{ content.upgradeHeading.replace('{0}', user.FirstName) }}

The email address you entered is registered with InvestSMART

Please login to continue

We have sent you an email with the details of your registration.

Looks you are already a member. Please enter your password to proceed

{{ upgradeCTAText }}

Updating information

Please wait ...

Your membership to InvestSMART Group recently failed to renew.

Please make sure your payment details are up to date to continue your membership.

Having trouble renewing?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

You've recently updated your payment details.

It may take a few minutes to update your subscription details, during this time you will not be able to view locked content.

If you are still having trouble viewing content after 10 minutes, try logging out of your account and logging back in.

Still having trouble viewing content?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

Please click on the ACTIVATE button to activate your Intelligent Investor 15-day free trial

Please click on the ACTIVATE button to finalise your membership

Unsuccessful registration

Registration for this event is available only to Eureka Report members. View our membership page for more information.

Registration for this event is available only to Intelligent Investor members. View our membership page for more information.

- You are already registered for this event.

- This event is already full.

- Please select a quantity for at least one ticket.

- {{ i }}

Forgotten password

Please enter your email address below to request a new password

- Indepth analysis of ASX listed shares

- BUY, Hold and Sell Recommendations

- Ideas Lab

- Special Reports

- Alan Kohler’s Weekend Briefing

- Interviews with CEO’s & top influencers

- Money Cafe and Talking Finance

- Super Advice and Q&A with Ask Alan

Last Night

Dow Jones, up ~0.56%

S&P 500, up ~0.77%

Nasdaq, up ~0.81%

Aust dollar, US82.3c

Back Again

When I wrote my final Saturday letter for 2014 a few days before Christmas, and did my last spot on the ABC for the year, the All Ordinaries was 5312.7, having just scrambled back above 5,300 that afternoon. Yesterday it dipped below 5300 again for the first time since then.

I've come back from holidays not very tanned because my daughter was out from London and we couldn't spend much time at the beach (she had things to do, people to see, in Melbourne, you understand) but more optimistic than when I left the office before Christmas, partly because of all the superficial, mostly irrelevant ructions that have been shaking investment confidence lately. We are in a weird spot right now: the fundamentals are still good but there are a lot of bad things happening. I'm still a buyer on the dips.

Having said that, there is no reason to suspect 2015 will be smooth sailing. There hasn't been a correction greater than 7-8% for about four years, and Wall Street has increased in each of the past five years, which has only happened once before. Another year, making it six in a row, has never happened at all.

The Australian market looks less stretched and has really done nothing much since the end of the rally of late 2012, early 2013 – but that's mainly because of the commodity crash. The resources index has fallen 25% since mid-August and 50% since the peak of April 2011. Banks are exactly where they were in November 2013, plus dividends of course, and Aussie industrials have been grinding higher since mid-2012, apart from a 10% correction in the second half of last year when retail sales softened and the dollar rallied a bit.

But since you and I last communicated, our attention and thoughts have been overtaken by two subjects: the deepening, and now widening, commodity price collapse and Islamist terrorism – the Sydney siege, the Paris murders and the horrific activities of Boko Haram in Nigeria. The second of those subjects obviously has a less direct impact on our investments than the first, which is the key issue for us all in 2015, but it is having a significant impact on sentiment and is worth focusing on to some extent. Terrorism is, in effect, amplifying economic uncertainty and political discourse is being dominated by the dual issues of finance and security.

Jihad

Some people wrongly assert that what's happening is a war between Christianity and Islam. There is a war going on, but it's between modern secularism and some Muslims, and within Islam itself. Over the centuries Christianity and Islam have had plenty of wars and invasions both ways (more by Christians on Muslims than the other way around). Charlie Hebdo staff died defending the secular principles of satire and free speech, not a religion. They knowingly took a risk and paid the price. The four people who died in their kosher supermarket while shopping for the Sabbath, merely for being Jews, is an entirely different, and much more disturbing, matter and Jews across Europe are very worried about a possible new rise of anti-Semitism. A lot of them are now heading to Israel to live.

Europe is in a state of war because, as George Friedman of Stratfor points out, there is no way to distinguish Muslims who might kill for their beliefs from those who won't. Of course not all Muslim are jihadists; those who are killers represent a very small minority, but which is which? The French Prime Minister has called for a war on radical Islam, but as Friedman says: "Calling for a war on radical Islamists is like calling for war on the followers of Jean-Paul Sartre. Exactly what do they look like?” The result is that it tends look more like a war against all Muslims, and for some people at the fringe, it is.

Europe's problem arises from the immigration that followed the collapse of Europe's colonisation of North Africa and the Middle East, combined with Europe's need for cheap labour. A similar phenomenon has been going on in North America, where the cheap labour comes from Mexico.

But whereas the US is still deeply religious, so that the equally religious Mexicans fit right in, the complication in Europe is that it is no longer even Christian, let alone Muslim, but is now mostly secular and “multicultural”. Religion is a private matter and totally excluded from public life and has been that way, more or less, since Napoleon. What's more, Muslim immigrants have no intention of becoming secular Europeans. They came to France get a job and money, not to become French.

Charles Gave of the GaveKal investment newsletter writes: "the question must be asked whether Western nations are nursing a small minority of individuals who want to impose a system of Sharia law that opposes everything the majority holds dear? And, if so, and if that minority is large enough, do we risk more blood on our streets (whether in Paris, Sydney, Ottawa, Toulouse…). The question that then emerges is what can Western nations do about it without compromising the values they hold dear?”

What indeed. This is a strange war and a difficult one for an investor to deal with because there's no beginning or end to it. The ‘battles' are brief, horrific spasms that are called ‘terrorism' rather than strategic, comprehensible warfare. It certainly has a long way to run: the Islamic world is not about to embrace secularism and Muslims are no more able to deal conclusively with their murderous minority than the Australian or French police are, despite the lecturing that Muslims get from various quarters telling them to do so.

As recently as yesterday morning, Belgian police raided an apartment in a town near the German border and killed two people as part of an “anti-terrorism operation”. At the same time, satellite images have emerged of the latest Boko Haram atrocity in northern Nigeria, in which 2000 souls seem to have been murdered, and about which the government of Africa's largest economy seems helpless.

I don't know what to do about all this, except to hold my nerve and not to allow my investment strategy to be swayed by the anger or distress I feel. If market volatility is worsened by terrorism, then it should bring buying opportunities. Unfortunately this war could last a long time yet and there could be many more spasms.

Commodities

The commodity collapse, which started with iron ore, extended to oil and has now roped in copper, also seems a complex and difficult matter to deal with, but is actually quite simple and positive, on balance. In fact, I don't think it is much more complicated than: “producers lose, consumers win.”

Some describe it as the bursting of a bubble, but that's wrong in my view. Bubbles occur when an asset is greatly overvalued by herd psychology and it bursts when reality intervenes and the herd stampedes in the other direction. That is definitely NOT what is happening with commodity prices, although of course there is a fair bit of speculation in the various futures markets, as we saw with the big short-covering rally in oil on Thursday.

The other difference with a bubble is that assets are generally used as loan collateral, so that when a bubble bursts, banks also go bust. To some extent oil reserves have been used as collateral for loans, but this is not a significant factor and while some banks might lose some money, we will not see bank runs and collapses as we did in 2008 after the collapse of the US housing bubble. It was the banking crisis that caused the recession, not the fall in house prices itself.

The question to be answered by hindsight is whether $US50 is the new price floor or a new ceiling of a much lower trading range. There are opinions both ways but only time will reveal the answer because while we can make educated guesses about demand, the actions of OPEC, Saudi Arabia, Russia and the American frackers cannot be foretold. At the moment they are producing flat out, but will they keep doing that?

Commodity prices were driven higher by Chinese demand until 2010 and the economic boom in Europe and the US that ended in 2008. There was a supply response to the higher prices, including the discovery of fracking in the United States, and at the same time Chinese and European demand has declined. So prices fell. And they will stay down until supply is curtailed AND demand picks up. Both are required and it will be a slow process, notwithstanding the short-covering rally in oil and gas prices over the past few days. Oil was oversold and bounced as the shorts got caught, that's all.

Obviously if you own iron ore miners, energy suppliers, and now copper miners, the situation is pretty simple, and dire: you lose. If you own businesses that are engaged in building mines and processing plants, you also lose because nothing will be built for a while. If you own businesses that supply the operations of mines and oil and gas wells, you won't lose for some time because the operators will be maintaining, and probably increasing, their output to preserve cash flow and to survive. That will have the further effect of keeping the prices down and probably causing more falls.

That's what is happening with oil and iron ore. Some producers are engaged in price wars to opportunistically get market share up, while others are pumping out material simply to stay alive. Either way, supply is not going to be choked in a hurry.

On the demand side, global economic forecasts are being reduced. As the World Bank observed this week, the world economy is running on one engine – America – and it seems to be sputtering as well.

Australia as a whole is a commodity producer so this country's situation is also pretty simple: we lose. Countering that, the currency has been falling, which is lifting manufacturing, and there is also an apartment construction boom on. Housing starts rose 12.5% in the September quarter on the back of a 31.3% rise in apartments (houses were flat). In November apartment approvals jumped another 16.7% on top of a 30% rise in October.

The Australian dollar has further to fall, partly because the terms of trade haven't finished declining and partly because the US dollar hasn't finished rising, not by a long way. Manufacturing and construction employ more people than mining, so if they continue to recover that should offset the employment effect of the mining and energy bust. If not, the Reserve Bank will cut interest rates again, and keep cutting.

A negative will be the predicament of the Australian government: its budget is in strife so fiscal policy is likely to be a drag on the economy, although maybe not if nothing can be got through the Senate. The backdown on the Medicare rebate this week is another sign of how tough it is these days for spending to be cut, and for taxes to be raised. Perhaps all that will happen is a deficit blowout, which would be good for the economy in the short term, but bad in the long term and very bad for the re-election prospects of the Coalition.

Swiss Jeez!

Switzerland shocked markets on Thursday by abandoning the 1.2 exchange rate peg (franc to euro) and cutting interest rates from -0.25% to -0.75%. That's right – minus. You pay them to hang onto your money and keep it safe. And enough bankers want to do that for the franc to suddenly go from 0.83 euros to parity, in one jump on Thursday. Markets took it pretty badly because this was just another piece of unexpected dislocation. Enough! Can we just get a bit of calm please?

In fact it does nothing to change the outlook for share markets, and if anything is positive because another significant central bank is cutting interest rates, on top of the Bank of India's 25 basis point cut this week, and another government bond is yielding near zero, helping to further pull down the global interest rate structure.

Swiss watches just became more expensive and all those going to Davos for the World Economic Forum will get a severe case of sticker shock when buying drinks (or rather their expense accounts will).

It will also make no difference to whether the ECB has a crack at quantitative easing, having ruminated so hard and long on the matter. If and when this happens soon, share markets should get a solid boost because there is too much uncertainty about it for this to have been priced in.

Deflation

The US CPI for December came out last night – minus 0.4%, the largest drop in prices since the crash and recession of 2008. For 2014 as a whole consumer prices in America grew by 0.8%, the second smallest increase in five decades. Core inflation, which excludes the 4.7% fall in energy prices, was zero.

Meanwhile European prices have fallen for the first time on record. New figures out last night showed that prices across the EU as a whole fell by 0.1% in December.

So … deflation right? All hell must be breaking loose. Well, no. There's a bit of a mess in Switzerland, but that's not about deflation – it's about safety. Swiss banks are safer than other ones, so money goes there and pushes up the currency, resulting in a form of Dutch disease (which is where a strong currency kills industry).

In fact there was an interesting statement in a piece on the European CPI this morning by a Wall Street Journal reporter: “Among many economists and central bankers, there is a widespread belief that falling prices by themselves don't constitute deflation. For that chronic condition to take root, consumers and businesses have to cut back on spending because they expect prices to fall further – the outcome being a decline in output and employment that pushes prices even lower.”

There you have it. It's not really deflation that we're seeing. Deflation is being redefined, or at least classified into good and bad deflation, which is understandable I suppose. Economists and central bankers have been so worried about deflation that when it turns out to be OK, they can't just abandon everything they have believed. They have to say that what they're worried about is the chronic version – you know, the one that leads to unemployment.

So will deflation as it's now being experienced in the US and Europe lead to collapse, recession and unemployment? No, of course not. Energy prices are falling and so are other costs as a result of technology. That's all good.

Interest rates

So what about interest rates? Surely with prices falling, there's no need to put them up, right?

Wrong. The president of the St Louis Fed, James Bullard, gave a speech and Powerpoint presentation last night and one of the slides said: “The level of inflation is not so low that it can alone justify a policy rate of zero.”

How come? “An important tenet of modern central banking is that a central bank must protect its credibility with respect to its inflation goal.” Does that mean what I think it means? That even though inflation is well below the Fed's target of 2%, the Fed has to pretend that the target is realistic to protect its credibility? OMG, as they say on Twitter.

I wrote late last year that I think there's a chance that US rates won't be increased this year after all, and I haven't changed that view, even though the Fed has continued to get the markets ready for a hike. That doesn't mean it will happen. At most the Fed's discount rate will be raised to 0.5%, if only to get the zero out of the official policy rate (it's currently 0-0.25%).

As for Australia, there is a developing consensus that the official policy rate in Australia will be cut, probably twice, this year. This is a pretty remarkable turnabout from a year ago, when the forecasters were unanimous that the next move would be up. The change has been brought about by the commodity price crash, of course, but the global picture is still pointing to lower rates as well. Last week India and Switzerland were cutting, and the European Central Bank is surely going to do some QE before long, especially with deflation happening there. China is easing monetary policy in the midst of weak inflation as well.

To sum up, I don't think interest rates will be the headwind for share markets this year that we might have thought as recently as six months ago. Disinflation, and in many places actual deflation, is entrenched by lower commodity prices and automation. Neither of those things is about to change in a hurry, so there will be no reason for central banks to raise interest rates to deal with the reality of inflation.

The only reason they would do it is to deal with the phantom of inflation, via the NAIRU, which is the acronym for non-accelerating inflationary rate of unemployment. The belief that unemployment cannot go below about 5.5% without causing inflation has underpinned central banking for 50 years. Maybe it was right 30 years ago, but not anymore. The US unemployment rate is 5.6% – basically right on the NAIRU. What if the unemployment rate falls to 5% in 2015, which it probably will, and there's still no inflation? Will the Fed raise rates just in case, because the NAIRU says it should? I doubt it.

Oh, and then there's the matter of credibility, according to James Bullard.

Quickstep Holdings

The first of this week's CEO interviews is Tony Quick, chairman of Quickstep (no relation). The company makes carbon fibre parts for planes and cars, and has a contract to supply parts for the US Joint Strike Fighter, of which the American government has ordered 3000 and we've ordered a few as well. Now Bob Gottliebsen reckons these planes are absolutely hopeless, but Tony Quick, who, it turns out, designed 10% of the JSF, naturally disagrees. More importantly, he says whatever you think of the JSF, the US government is sticking with it no matter what and his company's contract is therefore 100% secure.

Apart from that, it's all about getting more carbon fibre into cars to comply with the demand for reducing weight and thereby reducing fuel consumption and emissions. Carbon fibre is much more expensive than steel, but Quickstep's patented process for making the stuff is cheaper than the normal method, so it's more likely to be successful in replacing some of the body panels and chassis.

Meanwhile Quickstep's board has just appointed a new operationally focused CEO who starts next month, relieving Tony from his temporary executive duties.

This is a really interesting interview and well worth watching. Do it!

Click here to watch it.

Pro Medicus

The second CEO interview is with Sam Hupert of Pro Medicus, the radiology software and e-health vendor, and it's also really interesting, and well worth watching (do I ever do boring interviews? I ask you!)

Five years ago Pro Medicus bought an American radiology software business at a rock bottom price, and renovated it. Now Sam and his team are using it as a beachhead for the US market and are getting some early wins – a big US hospital and clinical system has signed a six-year contract (would you believe he can't name them) and there have been a few smaller contracts signed since then that he can, and does, name.

This an 80% margin business in which this little Aussie operator based in Swan St in Richmond, Melbourne (I drive past it on the way home every night) is taking on and beating the American giants. This is a wonderful Australian success story which has obviously only just begun its journey.

However, the shares are NOT cheap. Having doubled in a year, the price is now 90 times last year's net profit and more than 50 times this year's expected profit, so a lot of the success is already in the price. As to whether the stock is worth $1.33 and would repay investment at this price over the long term, I couldn't say, but I really like the company, and the way Sam is going about it.

By the way, he and his co-founder Anthony Hall own 30% each of the company, and they're not getting any younger. I actually think it's probably a takeover prospect – at some point Sam and Anthony will get an offer from one of their American competitors that they can't refuse.

Watch the interview here.

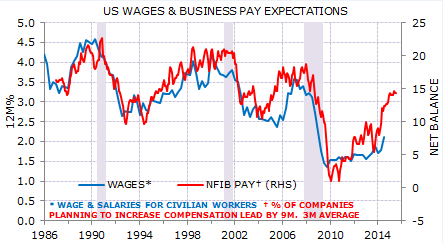

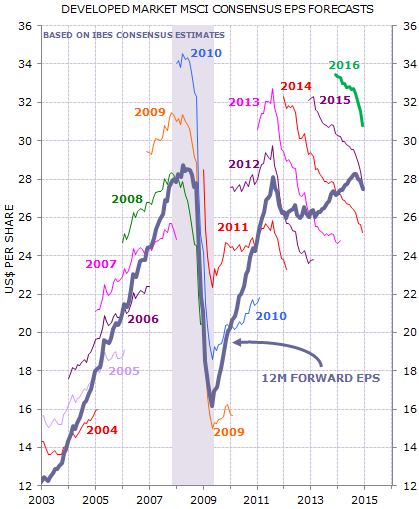

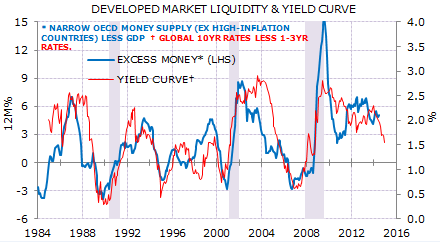

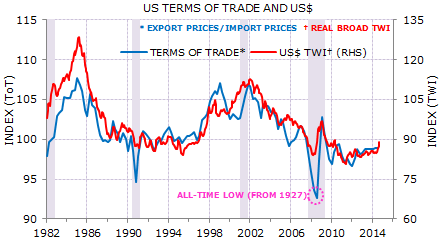

Minack's five graphs

Here are the five graphs that Gerard Minack says he'll be watching this year:

The Fed is the only central bank likely to raise rates this year. If and when it does will be determined by this chart – wages and pay expectations.

Analysts are cutting EPS forecasts for developed equity markets. The forecast is now no higher than 2012, or 2008.

QE in Europe and Japan will not offset the prospect of tighter US policy. Rate markets are starting to reflect that change. Also, the yield curve has a perfect record in predicting recessions. When it goes inverse (that is, short-term rates are higher than long-term rates) there is always a recession. Developed economies' average yield curves are flattening.

If the dollar keeps rallying without supporting terms of trade improvement it is a signal that financial forces are at work. One likely force is stress on foreigners who have borrowed dollars over the past five years. Put another way, a rising US dollar unsupported by the terms of trade is a bearish augur.

Finally, credit markets could again be the early warning sign in this cycle, as they were in the last. Zero rates have arguably created more mis-priced risk in debt markets than equity markets. A shift in monetary policy therefore could be felt first in credit than in equities.

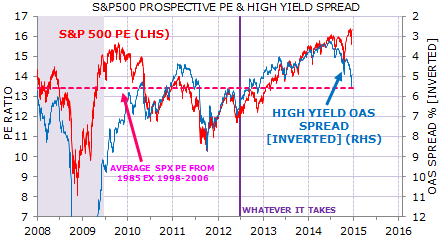

This year already saw a narrowing in asset returns. Exhibit 5 shows the recent, widening divergence between US equity valuation and performance of high yield credit. My base case is that US equity valuations will fall through 2015, following the lead from the de-rating in other risky asset markets. However, I am alert to the risk that investors funnel into Wall Street, and US equities see a final valuation surge. Exhibit 5 is a warning that the correlation between equities and credit can break, at least for a time that matters, to many investors.

And here are 10 things to watch in 2015,

… from the economics team at ANZ:

1. Worldwide wages watch: Slower wages growth would imply a greater degree of fragility for the global economy and will see central banks retain a stronger bias towards lower rates.

2. China deleveraging – it's all about the speed: Deleveraging pressures to date remain localised within the markets or regions in which they have occurred. We expect this to persist, but there are clearly risks.

3. AUD – more than a shock absorber? While domestic factors will remain central to the currency's fate, the market's reaction to the divergent paths of the three major central banks will be key.

4. ‘Animal spirits' – a key swing factor: Against a backdrop of weak national income growth, can Australian business and consumer confidence lift significantly without a supporting exogenous factor?

5. Labour market partials: Look to developments in job advertising as a critical indicator of labour demand and a cross-check on the official unemployment data.

6. Housing market policy: The official response has been very measured so far. Hard policy targets, if implemented, could drive a more substantive slowdown in investor housing finance and house prices.

7. Flatter and lower curves: There is potential for a significant fall in Australian term rates. Australian 10-year government yields could fall as low as 2% over the course of the year.

8. Iron ore – absorbing higher than normal supply: A key factor will be the supply discipline from high-cost Chinese capacity.

9. Oil – waiting for supply cuts from US shale: Investors are still adjusting to the structural change in the market, and the risk is for further liquidation in the first half of 2015 amid swollen inventories.

10. Structural reform – a year of opportunity: Bold decisions are needed to lift Australia's long-term growth potential.

Separate bedrooms

Our theory for the newly renovated house was that the menagerie – Sam, Maisy and Steve – would all sleep in the laundry, which we made big enough to accommodate them. Yes, well, that was the theory. Steve, however, has had a tantrum and made it clear he can't possibly share a bedroom with snoring, farting dogs! What were we thinking! He'd rather sleep in the garden, thanks very much, which is what he seems to be doing.

When I get up in the morning I let Maisy and Sam out of the laundry, then open the back door and Steve emerges from under a bush for a bowl of milk. Oh well. He seems happy enough, although maybe he'll have to put up with the snoring in winter.

brightday webcast

As you may know, the commercial team at Eureka Report has been busy creating a new superannuation platform called brightday, in partnership with listed provider OneVue. I think this is a fine extension to the work we've been doing for 10 years at Eureka Report, so you might be interested in tuning into a webcast on the subject, to learn a bit more. Click here to register.

Readings & Viewings

Wow, this is incredible: a bracelet that projects a computer screen onto your forearm. Forget tablets and smartphones – it's all about skin!

Speaking of smartphones ... eight years ago this month, Steve Jobs stood on stage and introduced the iPhone in an extraordinary performance that changed the world. Here it is.

And this bloke reckons they will still be most disruptive technology over the next five years.

George Friedman's top five events of 2014

2014 in data from Euromoney.

The impact of lower oil prices on exporting countries. Summary: not good.

An analysis from Callam Pickering of the Swiss government's stunning foreign exchange moves on Thursday.

Why are commodity prices falling?

The Australian dollar could fall below US70c, according to Blackrock. I agree.

It's been asked whether Medicare will survive the Abbott Government, but it might now be more pertinent to ask whether Tony Abbott will survive Medicare.

An autopsy of that dead Medicare policy.

George Soros: a new policy is needed to rescue Ukraine.

If the US stock market closes higher this year, it will do something it has never done before.

There have been millions of words published about the attacks in Paris. Here are just a few pieces I think are worth reading:

* George Friedman's essay in full.

* Signs of shrinking freedoms already, with Muslims, unsurprisingly, bearing the brunt.

* Blasphemy and the law of fanatics.

* From the New Yorker – Charlie Hebdo and the clash of civilisations.

* The Charlie Hebdo editorial meeting days after the attack.

* Ayaan Hirsi Ali: our duty is to keep Charlie Hebdo alive.

* And finally this was a wonderful interview on ABC's 7.30 with Ayaan Hirsi Ali. Well worth spending 8:20 on.

Joseph Stiglitz: Europe's lapse of reason.

Why pigs are crucial to understanding China's low inflation (yes – pork is getting cheaper).

John Authers in the FT on the virtues of deflation.

This is one of the all-time great newspaper editorials. Make sure you notice the first letter of each new paragraph.

A history of hair dye.

The internet is not killing culture -- it's always been hard to make a living in the arts, and it still is.

The United Nations, while hailed as a collective body of world leaders, is in reality little more than a collection of brutal dictators, benign and malicious autocrats and theocrats, and corrupt bureaucrats. And so on.

Fascinating piece on the business of being James Patterson, the best-selling author. He “writes" 14 books a year.

A bit of fun with Wall Street analysts' stock market predictions.

Six minutes of looking out of the window of a space station, back at Earth. Beautiful.

A great, scary video on the future of technology - “Humans Need Not Apply”.

My piece during the week on the same subject:

Happy Birthday Paul Keating, 71 tomorrow. Here's a collection of his best insults.

Last Week

By Shane Oliver, AMP Capital

The ‘risk off' tone in markets continued over the past week with mixed US economic data and earnings results along with a continuing fall in oil prices maintaining downwards pressure on US, Japanese and Australian shares and bond yields continuing to slide. However, European shares were boosted by expectations for ECB quantitative easing and Chinese shares also gained. While the Euro continued to slide against the $US, the $A was little changed helped by a strong jobs report.

While US shares remain under pressure, European shares have been outperforming reflecting expectations for the ECB to announce a widening in its quantitative easing program at its January 22 meeting. Expectations on this front were boosted by an opinion from the European Court of Justice that ECB sovereign bond buying does not violate EU treaties and by the Swiss central bank (SNB) abandoning the 1.20 currency floor for the Euro against the Swiss Franc.

Switzerland is a small country so it's hard to get too excited by the surge in the Swiss Franc and fall in Swiss shares (unless you were the wrong side of those moves) that resulted from the SNB's action. That said there are some global implications. First, it provides a reminder that such exchange rate fixings are hard to sustain. Second, it demonstrates there is more scope for negative interest rates in the face of deflationary pressure globally with the key SNB interest rate being cut to -0.75%. Third and related to this, it highlights that other small countries may be forced into further monetary easing if ECB QE pushes their currencies higher. Finally, it likely reflects SNB expectations that the ECB is about to expand its QE program.

For Australia, the Swiss gyrations underline the problem that outside the US lots of countries would like to get their currencies down making it harder for the $A to fall on a trade weighted basis which in turn means it will have to fall further against the $US.

Shock, horror the World Bank revises down its global growth forecasts - but nothing new! Over the last few years organisations like the World Bank, IMF and OECD have been forecasting a pick-up in global growth to around 4% or so only to revise down to around 3-3.5%, usually well after smart investors had already allowed for it. The World Bank kicked off the process again for this year, shaving its 2015 global growth forecast to 3.6% (against our own view of 3.5%) and continuing to expect a bounce to 4% in 2016 (which is probably again too optimistic). There is nothing new in this. In fact I prefer a world of constrained and uneven growth because the opposite of strong and synchronised global growth would only mean an increased risk of overheating, inflation and monetary tightening.

But while there is no reason for alarm at the latest World Bank revisions, the plunge in bond yields is worth keeping an eye on. US 10 year yields are now zeroing in on their 2012 lows and in other countries they have fallen below 2012 levels to record lows. This includes Australia. While the bond markets could be over-reacting again like they did in 2012 and setting up for a sell, which is my base case, they are also providing a reminder that deflation is more of a threat than inflation.

Source: Global Financial Data, Bloomberg

Major global economic events and implications

US data releases were pretty mixed with a further rise in job vacancies and stronger conditions amongst small business and New York region manufacturers, but weaker conditions in the Philadelphia region and much softer than expected December retail sales. Most of this looks like noise though and in particular December quarter retail sales were strong once lower consumer prices are allowed for. There is nothing to change the Fed's view in all of this.

The US December quarter profit reporting season kicked off with a good beat by Alcoa, but some mixed bank results. So far 86% of results have beaten earnings expectations, but only 49% have beaten on sales. But its early days as only 35 S&P 500 companies have reported so far.

Chinese trade data rebounded in December helped by the end of APEC related shutdowns but money and credit data was mixed. While credit bounced back this looks temporary with a downtrend in annual credit growth likely to remain in place. We continue to expect further PBOC interest rate cuts this year.

While Russia and Brazil look poor (causing a rethink of the BRIC concept) India is looking good with industrial production strengthening and inflation falling, with the latter allowing the Reserve Bank of India to cut its key interest rate by 0.25% to 7.75%. Expect further cuts this year as inflation continues to moderate.

Australian economic events and implications

In Australia, the highlight over the last week was another booming jobs report. December jobs growth was far stronger than expected for the second month in a row pushing the unemployment rate down to 6.1%. While great news, it's hard to believe nearly 100,000 new jobs were created over the last 3 months. Very weak hours worked also call into question the reliability of the jobs data. Given usual volatility and recent data problems the jobs data is best treated with caution. Rising job vacancies tell us employment growth should be okay, but nowhere near as strong as has been reported over the last few months.

Meanwhile, a surge in dwelling starts in the September quarter points to a rebound in housing investment in the December quarter but this may slow this year as housing finance is clearly losing some momentum.

Given the various cross currents – strong jobs, a lower $A/$US rate and the boost to spending from lower fuel prices versus inflation threatening to break below target, a still too high $A on a trade weighted basis and sub-par growth overall – the RBA is likely to sit on its hands at the February Board meeting, but is still likely to cut the cash rate once more in the months ahead.

Next Week

By Craig James, Commsec

Focus on state economies and inflation

There is a spattering of new economic data and surveys to digest in the coming week.

The week kicks off Monday with release of the CommSec State of the States' economic performance survey. The report covers eight indicators including retail spending, unemployment and economic growth.

In terms of economic data, due for release on Monday is the latest inflation gauge from TD Securities and the Melbourne Institute. The key question is how low can inflation go?

Also due on Monday are the December figures on new car sales from the Bureau of Statistics (ABS). The industry data has already been released and the ABS data will merely recast the figures in seasonally adjusted and trend terms.

The industry data showed that sales in December were a record for any December month.

On Tuesday, the ABS releases December figures on the imports of goods. The data is one of the timeliest measures of economy-wide spending.

Also on Tuesday, Roy Morgan and ANZ release the weekly consumer confidence index. Confidence is just OK at present, but despite that consumers are still spending freely. The good news for retailers is that the latest estimate on whether it was a good time to buy a major household item was at 5-month highs.

On Wednesday, the weekly consumer confidence figures will face some validation from the monthly consumer confidence reading complied by Westpac and the Melbourne Institute. The value of this survey now is in the questions posed quarterly on the wisest place to put new savings.

And on Thursday there are two indicators to watch. The first is the detailed job market data for December. This report includes results such as unemployment by region and estimates on employment trends for demographic groups.

The second indicator is the new home sales figures for November from the Housing Industry Association. For the past seven months, home sales have been travelling sideways in a zig-zag fashion.

Overseas: Chinese economic data takes centre-stage

With only largely ‘second-tier' readings expected in the US, investors will spend more time concentrating on Chinese economic data. Still the International Monetary Fund release economic forecasts on Tuesday.

The week begins on Sunday when data on Chinese home prices for December are expected. Currently house prices are 3.7% down over the year.

On Tuesday, Chinese economic growth (GDP) figures for the December quarter – and for 2014 as a whole – will be released. The economy is probably growing at a 7.2% annual pace. On the same day the usual monthly activity readings are expected, covering retail sales, production and investment.

On Tuesday in the US, the National Association of Home Builders index is expected to show a modest gain.

On Wednesday, housing starts data is due in the US with annualised starts tipped to lift from 1.028 million to 1.04 million in December. New building permits are also expected to have edged higher in the month. The usual weekly data on mortgage finance is also released.

On Thursday in the US, the Federal Housing Finance Agency issues its November data on home prices. Home prices are currently 4.5% higher over the year. The Markit “flash” readings on manufacturing activity are released in the US as well as Europe and China. And the usual data on claims for unemployment insurance is issued in the US.

And on Friday, there are two indicators that bear watching – existing home sales and the leading index. Existing home sales are expected to have lifted from a 4.93 million annual pace to 5.05 million in December. Meanwhile the leading index may have lifted 0.4% in December.

Sharemarket, interest rates, currencies & commodities

The US earnings season has begun – the time when companies report their quarterly profits or earnings. In October last year, the consensus estimates compiled by S&P Capital IQ suggested that fourth quarter earnings (December quarter earnings) would be up 11.5% on a year ago. Currently analysts believe that annual growth will be closer to 4.6%. While expectations have been pared across the board, substantial downgrades have been issued for the Energy and Materials sectors.

Amongst companies scheduled to report on Tuesday are IBM, Baker Hughes, Halliburton and Morgan Stanley.

On Wednesday earnings are expected from American Express, eBay and US Bancorp.

On Thursday, profit results are slated from E*TRADE, Altera, Starbucks and Verizon Communications.

And on Friday, General Electric, Bank of New York Mellon, State Street and Kimberly Clark are amongst those expected to report earnings data.