Kohler's Week: US Jobs, Water, Oil, Oz GDP, RBA, Azure

- {{x.value}}

{{ twilioFailed ? 'SMS Code Failed to Send…' : 'Enter verification code' }}

{{ completedStep1 ? 'Authentication & Security' : content.trialHeading.replace('{0}', user.FirstName) }}

{{ content.upgradeHeading.replace('{0}', user.FirstName) }}

The email address you entered is registered with InvestSMART

Please login to continue

We have sent you an email with the details of your registration.

Looks you are already a member. Please enter your password to proceed

{{ upgradeCTAText }}

Updating information

Please wait ...

Your membership to InvestSMART Group recently failed to renew.

Please make sure your payment details are up to date to continue your membership.

Having trouble renewing?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

You've recently updated your payment details.

It may take a few minutes to update your subscription details, during this time you will not be able to view locked content.

If you are still having trouble viewing content after 10 minutes, try logging out of your account and logging back in.

Still having trouble viewing content?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

Please click on the ACTIVATE button to activate your Intelligent Investor 15-day free trial

Please click on the ACTIVATE button to finalise your membership

Unsuccessful registration

Registration for this event is available only to Eureka Report members. View our membership page for more information.

Registration for this event is available only to Intelligent Investor members. View our membership page for more information.

- You are already registered for this event.

- This event is already full.

- Please select a quantity for at least one ticket.

- {{ i }}

Forgotten password

Please enter your email address below to request a new password

- Indepth analysis of ASX listed shares

- BUY, Hold and Sell Recommendations

- Ideas Lab

- Special Reports

- Alan Kohler’s Weekend Briefing

- Interviews with CEO’s & top influencers

- Money Cafe and Talking Finance

- Super Advice and Q&A with Ask Alan

Last Night

Dow Jones, down ~1.6%

S&P 500, down ~1.4%

Nasdaq, down ~1.1%

Aust dollar, US77.1c

US Jobs

Wow. American firms hired a net 295,000 people in February against a median Wall Street forecast of 235,000. The US dollar index surged more than 1 per cent on the news and the Australian dollar dropped from US78.4c to US77.1c, and this morning it looks set to go below US77c for the first time in six years.

Employment in the US has now increased for 12 straight months, the longest streak since 1995, and the pace of growth is the strongest since the late 1990s. The unemployment rate fell from 5.7 per cent to 5.5 per cent, the lowest level since 2008.

It wasn't all positive news, though. Wages rose only 0.1 per cent, and is stuck at 2 per cent annual growth – about the same as in Australia. Labour force participation was only 62.8 per cent, down from 62.9 per cent in January: the share of working age adults who were either employed or looking for a job was only 66.1 per cent, so a lot of people have given up. That suggests that there's more slack in the US labour market than the employment figure would suggest.

Nevertheless there's now a universal view that it won't be long before the US Federal Reserve starts raising interest rates, and Richmond Fed President Jeffrey Lacker added to this by telling a radio station this morning that he thought June would be a good time.

Here's what happened to the Australian dollar this morning.

Happy Birthday Bull Market

On Tuesday it will be exactly six years since the ASX 200 hit an intra day low of 3120.8. It's now 5898.8. That's a compound annual capital growth rate of 11.2 per cent (dividends get it to 16 per cent).

The S&P 500's 2009 low was 666.79 on March 7, so today is the US bull market's birthday. It's now 2100.9. That's a compound annual growth rate of 21.8 per cent. Damn.

Water

I want to tell you about what Chris Corrigan is up to now, partly because it's also a fascinating story about water trading and investment in Australia, in what has become the world's most sophisticated water market.

Chris, you'll recall, was CEO of BT Australia and then Patrick Stevedores, where he cleaned up the waterfront through the 1998 waterfront dispute and then made a fortune selling the company, unwillingly, to Toll Holdings. He then moved into another stevedoring business called Qube Holdings, which is one of our analyst Simon Dumaresq's favourite companies. Qube's share price has gone from 50c to close to $3 in five years, outperforming the market five-fold, and Simon believes it has more to go.

Chris's next project is a listed company called Webster Ltd, which grows walnuts. Under his guidance (he owns 15 per cent and is on the board) Webster is doing three things more or less at once: it bought a 46,000 hectare property on the Murrumbidgee River called Kooba for $116 million; it bought a farming business called Bengerang, which is the remnants of a company called Prime Agriculture (Corrigan himself is one of the vendors of that) and it has made a takeover offer for a cotton business called Tandou Ltd.

At the end of this process, Webster will own entitlements to 230,000 megalitres (ML) of water. That's about half of Sydney Harbour, and will probably make the company either Australia's largest owner of water rights or very close to it.

Chris Corrigan told me yesterday that for him Webster is a “five-year project”. The plan is to be a significant owner of water and then to add value to the water through both permanent and annual cropping, the former starting with more walnut planting, which Webster already makes a decent cash flow out of, and the latter largely through cotton. In 2014, by the way, Webster made $8.7 million in profit from $55 million in revenue, entirely from walnuts, mostly exported.

Chris says listed agricultural companies in Australia have not had a great track record, although there are plenty of very rich farmers around who know how to manage Australia's water system and turn it into crops.

Tandou is one those listed ag businesses with an ordinary track record: at 44c before the bid from Webster was announced, the stock was trading at exactly the same price as it was 20 years ago. The offer is 1 Webster share for every 2.25 Tandou shares, which makes it worth 58c a share or $114 million.

Tandou's chairman Rob Woolley told me yesterday that they just couldn't close the gap between the share price and the NTA, which is 59c. The company started as a cotton farming business, which it still is, and became a water trader. Its entitlements portfolio sits at about 80,000ML and it has also been trading allocations, but it hasn't been getting value for these assets in its share price, so the board has been looking for another plan. Chris Corrigan proposed one: merge with Webster and become part of a much larger water play.

The way to think about water trading is that the entitlements are like the shareholding and allocations are like dividends. Each year the government gives water allocations to entitlement-holders and they can be traded or used to irrigate the farm. Entitlements are also tradable and in fact a lot of farmers sold theirs to the government for cash to pay off debts and are now on a treadmill of buying allocations every year to keep the farm going, and are hostage to the price fluctuations.

Chris Olszak at the research firm, Aither, tells me that the current price for high reliability entitlements (that is, where there's decent storage nearby, such as Eildon Weir on the Goulburn River) is about $1,800 a megalitre, up from $1,200 two years ago, while the more volatile allocation price has surged from less than $10 two years ago to $120 today.

The water market was established about 20 years ago, after caps were put on how much water farmers could take from the Murray Darling system. It took a long time to mature and settle down as a market, and there was a lot of politics along the way, but it is now orderly -- to the point where investors have now entered it.

As far as I can tell, there is just one vehicle for small investors to gain exposure to water entitlements. It's a listed investment company called Blue Sky Alternatives Access Fund (ASX:BAF), which has $60.9 million invested, of which $16.17 million is in a water fund. Here's a link to its most recent monthly report.

Webster is also now a water play, although it's really a farming business that owns a lot of water, rather than simply a water investment.

I also spoke yesterday with Cullen Gunn who runs a wholesale water investment fund (for “sophisticated” high net worth investors and big super funds only) called Kilter. He says water is a "great asset class". "It's like commercial property except there's no problem with impairment or messy tenants. The yield is sold, about 5-8 per cent and if someone doesn't pay you just take the asset back, instead of having to apply to have a tenant evicted."

"Also, it's clear to me that climate change means there is going to be less water in future, so the economic value of it will increase."

Looking at the price growth of water entitlements, I estimate that the compound annual growth rate has been about 10 per cent over 25 years, on top of the yield. Not exactly CSL, but certainly better than either residential property or the ASX 200.

Chris Olszak cautions that allocations can be a volatile market because, as Dorothea Mackellar wrote:

I love a sunburnt country,

A land of sweeping plains,

Of ragged mountain ranges,

Of droughts and flooding rains.

In the past 10 years or so, the price of water allocations has fluctuated from $500/ML during the drought, to $5/ML during flooding rains, so it's a market that requires a strong stomach.

Nevertheless, Australia is a dry place and the key to success in agriculture, and many other things, is water so long term it's probably a good investment.

Finally, I have not done any detailed analysis of Webster or modelled its future, either with or without the three acquisitions mentioned, so this is definitely not a recommendation to buy it. I just thought you might like to know what Chris Corrigan is up to, perhaps as a thought-starter on the subject of water.

Oil

One of the most important issues for our time, apart from whether Australia's Guy Sebastian will win the Eurovision song contest, is what's going on with oil. Maybe it's THE most important issue. Will the oil price bounce back, will it stay where it is, or will it keep falling? On these three questions hang much of our future. It's particularly pointed for Australia, and for you and I, because the central question is whether oil, and commodities generally, were in a bubble that has now burst, or whether what we are seeing now is a temporary setback.

The crude oil price has fallen more than 50 per cent, which has only happened once before since the first oil shock that followed the Yom Kippur war of 1973. That was in 2008 when the global economy was falling apart, which is not the case this time.

This time demand is weak for other reasons than a global economic bust and supply has increased dramatically because of US fracking technology, and the performance of commodities over the past few years does bear some similarities with the creation and bursting of a price bubble.

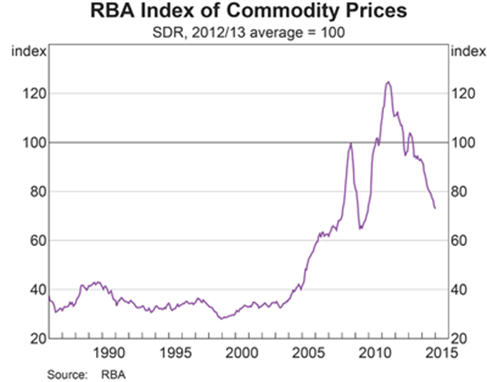

Here's the RBA index of commodity prices:

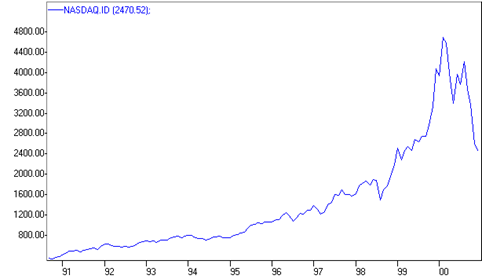

…and here's the Nasdaq between 1992 and November 2000.

The rise in the Nasdaq was 525 per cent in five years; the RBA Commodity index rose 320 per cent in 7 years.

Of course, whether something is a bubble is not simply determined by the extent of the price rise. The Nasdaq is back at 5000 this week, but this time it's not a bubble.

It's also a matter of whether the price increase is supported by fundamentals in some way. Changing fundamentals don't count: it's all about markets getting carried away. And commodity markets, led by oil, did get carried away. There was a huge spike in retail participation via exchange traded funds in what is usually a professional futures market supported by a misguided belief in “peak oil” (that the price could never go down because we're running out of oil).

Louis-Vincent Gave of GaveKal Research raises an interesting idea for one reason for the implosion of the oil market: the crackdown on Chinese corruption. When it began most observers thought this would last six to nine months and peter out, having gotten rid of Xi Jinping's political rivals. But 18 months on and it's still going strong.

“Meanwhile we have lost count of the number of PetroChina executives now behind bars or under house arrest. Which brings to mind Charlie Munger's putty observation: show me the incentives and I will tell you the outcome.”

“For years executives at PetroChina and other state owned enterprises were tasked with finding commodities deals outside of China's borders with little regard for the price paid. Is it a stretch to think that some deals were done on non-economic terms?

“But change the incentives from a few tens of millions in kickbacks in a Swiss/Singapore/BVI bank account to house arrest -- or even worse a bullet to the back of the head -- and all of a sudden the willingness of Chinese SOE management to do foreign commodity deals melts like this winter's California snow.”

In other words there was a hidden incentive for Chinese executives to push the commodity bubble higher (corruption) which has now disappeared.

If that's right, the question becomes – what changes from here? The continuing crackdown on corruption combined with SOE consolidation in China on top of the slowing economy (the government again reduced its growth target this week to “about 7 per cent”), as well as record-high US inventories, points to a complete absence of pricing pressure for the foreseeable future.

On the supply side, meanwhile, the big question concerns Saudi Arabia's intentions, and on that subject the Saudi Oil Minister Ali Al-Naimi gave a seminal speech in Berlin this week. Here are some excerpts:

"We have a long-term view. We try to avoid knee-jerk reactions to short-term market movements. Over the past eight months, though, with the market in surplus, it is Saudi Arabia that is called upon to make swift and dramatic cuts in production. This policy was tried in the 1980s and it was not a success. We will not make the same mistake again. Today, it is not the role of Saudi Arabia, or certain other OPEC nations, to subsidise higher cost producers by ceding market share.”

"This new oil supply growth – much of it coming from the US – is a welcome development for world oil markets and the global economy over the past several years. These new supplies, along with Saudi Arabia's own efforts, have helped offset outages from other oil producing countries. Without them, a still vulnerable global economy could have faced much higher energy prices. Saudi Arabia has consistently welcomed new unconventional supplies, including shale.”

"Ladies and gentlemen. Over the long term, the facts are indisputable. The world's population is increasing, the global middle class is expanding, and the demand for energy will rise accordingly. Access to reliable and stable energy supplies will help improve global living standards, increase educational levels and boost economies worldwide. In this, I believe all nations are in agreement. We have a shared responsibility to create the conditions that can make this happen.”

"A period of lower oil prices incentivises companies to take a more disciplined approach and focus on implementing production efficiencies. This is certainly true for our national oil company, Saudi Aramco.”

These are not the words of someone who wants to see the oil price go back up, and as Dennis Gartman observed this week, his attitude to fracking seemed anything other than hostile, but seemed instead to be even tangentially supportive.

This will seriously undercut those who have been thinking that Saudi Arabia and OPEC will move this year to cut production to get the price back up. Al-Naimi was, in effect, telling Russia, Iran and Venezuela: “Sorry boys, you're buggered. Get used to 50 dollar oil.”

So should you.

Oz GDP

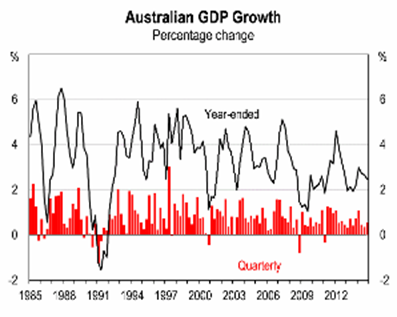

The December quarter national accounts confirmed that economic growth is stuck in low gear. Just eyeballing the graph you can see that growth used to default to about 4 per cent a year, except when there was an external shock, as in 1972, 1991, 2000 and, of course, 2008. Since the GFC, the “default” growth rate is about 2.5 per cent, which is what it was in the year to December 2014. There was a brief spike to 4 per cent growth in 2012 because of the final death twitches of the commodity boom, but apart from that growth has been what economists call “below trend” and what you and I would call ‘crappy'.

The two big drags on growth are mining investment, down 17 per cent year-on-year, and government austerity, leading to a 1.1 per cent fall in public demand. Household consumption rose 2.8 per cent year-on-year, and dwelling investment 8.1 per cent, but in general the pace of growth in the non-mining economy is weak and not enough at this stage to offset the decline in the resources sector.

I'm often asked: will there be a recession? You probably want to know the same thing. Well, of course I wouldn't have a clue, but I can't think of any reason seriously to forecast a recession, and therefore to base your investment strategy on it. The most likely scenario is for continued slow recovery in confidence, consumption and investment, although various national leaders – both here and overseas – often find innovative ways to stuff things up.

Specifically, a significant risk is another tight, chaotic budget in May, which would further reduce public demand and erode confidence. Given the fragility of the economy right now, Joe Hockey could actually cause a recession in spite of the Reserve Bank's best efforts to counter it with lower interest rates.

The guilty RBA

And by the way, I largely blame the RBA for getting us into this pickle. In 2009/10, after the US Federal Reserve had cut the Fed funds rate to 0-0.25 per cent and left it there, the RBA raised the cash rate here from 3 per cent to 4.75 per cent. The spread between the US and Australian cash rates therefore jumped to 4.5 per cent and between the US and Australian bond rates to 2.5 per cent.

This was a shocking blow to Australian businesses. The exchange rate soared from US64c to $US1.10, mainly, it's true, because of the spike in commodity prices in 2010/11 caused by the final spurt in Chinese demand, but while that was out of our control, the interest rate differential, which was under the RBA's control, made things worse.

I reckon those interest rate increases by the RBA in 2009 and 2010 were a bigger mistake than the two rate hikes that were Jean-Claude Trichet's final act as president of the European Central Bank in 2011, or even the ECB's rate hikes in 2008, and that's saying something. The ECB had to quickly reverse its strategy, and rates there are now negative, as they try to get the euro down.

The RBA mucked things up in 2010 by raising the cash rate to 4.75 per cent and then didn't go far enough in reversing it, or move quickly enough. It cut the cash rate gradually over two years to 2.5 per cent and then left it there for 18 months.

Meanwhile the car industry closed down and businesses around the country laid people off. Unemployment went from 5 per cent to 6 per cent and then 6.4 per cent. During this whole time, RBA governor Glenn Stevens said the exchange rate was too high and was hurting Australian industry, but he didn't do anything about it! Finally he's cutting rates again, although he was persuaded by the Sydney housing boom to hold off this week.

Maybe I'm missing something, and I'm sure my economist friends will tell me it's very complicated, but it seems pretty simple to me: if the exchange rate is too high, and leading to rising unemployment, you do the one thing you can do, which is cut the interest rate differential. Yes, house prices would rise – so clamp down on property lending and negative gearing in other ways, and properly, not like the pathetic warning from APRA in December that property lending growth should not be greater than 10 per cent.

I mean, really! Unemployment is 6.4 per cent and economic growth is stuck at 2.5 per cent because the RBA is worried about Sydney house prices! Give me a break.

Intergenerational Report

This is not a very good document, although like the previous three, it's thorough and presents three sets of plausible, well-researched 40-year forecasts of government spending and receipts.

The problem is the 40 years: the three scenarios are meaningless. Apart from the fact that they are 40-year forecasts when even four-year forecasts are always wrong – as the report itself says: "the projections in this report are very unlikely to unfold over the next 40 years exactly as outlined”. And two of the scenarios are based on policy assumptions that are no longer valid. Specifically, the one they want us to focus on – called “proposed policy”, which gets the budget into surplus in four years – “shows fiscal projections based on the full implementation of the policies of the government”.

Except that many have been dropped by the government, including the GP co-payment, or rejected by Parliament. Presumably the May budget will present new policies on which this Intergenerational Report can be based.

Also, there are some rather dodgy economic assumptions. The key one is productivity, which is projected to grow at an average annual rate of 1.5 per cent for 40 years, which was the average for the 2000s, and that unemployment falls to 5 per cent and stays there. GDP is forecast to grow at 2.8 per cent a year for the next 40 years, up from 2.7 per cent in the 2010 IGR because the rate of population growth has been increased from 1.2 per cent to 1.3 per cent. (Real growth in per capita GDP is projected to stay at 1.5 per cent.)

On the question of productivity, the report says: “reforms to enhance productivity over the next 40 years will be crucial if we are to achieve the growth in living standards we have enjoyed since the mid-1970s”.

So the whole thing is based on productivity reforms that haven't yet been thought of, let alone implemented, and which will still result in lower, and stable, unemployment.

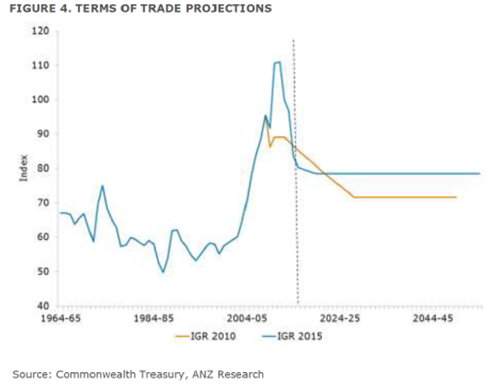

Also, ANZ produced a graph comparing the terms of trade projections in the 2010 and 2015 IGRs:

So not only does this report forecast higher commodity prices, by about 10 per cent, forever, because of the spike in the terms of trade that occurred since 2010, but it assumes that the terms of trade won't go back to the long-term average of 60 that prevailed for 50 years after WW2. Why won't it? Because that would be quite inconvenient.

As you can tell, I think the whole thing is a bit of a waste of time, and designed purely to soften up the Senate cross-benchers to pass the 2015 budget. The danger is that the forecasts on which it is based are so dodgy that it will be counterproductive.

Azure Healthcare

After my interview with Robert Grey of Azure Healthcare this week, he said: “Phew! That was OK. I thought you were going to give me a hammering!”

I hate it when they say that. I think: bloody hell, I should have been tougher on him. I thought I was pretty tough. The thing is when I interviewed him last August, Azure's share price was 40c. It's now 35c, having crashed from 45c to 25c after what was seen as a profit downgrade at the AGM last year. Also, Robert sold a third of his stake, from 30 per cent to 20 per cent. The market was disgusted. Me? I filled my pockets at 25c, thanks very much. This is well-run company with a good product that's selling well in the United States. The stock was suddenly cheap for the wrong reasons, which Simon Dumaresq told you about at the time.

The problem with this company is that Robert insists on expensing all capital expenditure against the P&L, rather than capitalising it. So when he decides to increase the investment in the US, as he did last year, it means a lower profit in the short term, even though he is building an asset.

Is it a good policy, or bad? I don't know. It's short-term bad, long-term good because returns are higher later. The main thing is that Azure's nurse call hardware and software is in 8500 hospitals and clinics and that number is growing strongly. Client retention is about 85 per cent, and Azure will soon start selling other products, like HR systems, to those hospitals.

Oh, and the other main thing is that it's a classic takeover target. Hills Industries approached last year but was rebuffed. More likely is a bid from a big US healthcare firm, and Robert, still with 20 per cent, will get to decide on the sale price.

You can watch my latest interview with Robert here.

Readings & Viewings

Video of the Week 1: some German comedians have a written a very funny song about Greek Finance Minister Yanis Varoufakis (and also about Germany).

Video of the week 2: an oldie but a very goodie. Possibly the greatest music video of all time.

You've heard of artificial intelligence (AI). Well, try AEI – artificial emotional intelligence.

Lessons on manufacturing from the ancient Athenians.

In the Silicon Valley, a new elite is forming that wants to determine not only what we consume, but also the way we live. They want to change the world, but they don't want to accept any rules. Do they need to be reined in?

The founder of Alibaba, Jack Ma, explained that “one of the secret sauces for Alibaba's success is that we have a lot of women”. Women hold 47 per cent of all jobs at Alibaba and 33 percent of senior positions.

John Daley of the Grattan Institute: the Intergenerational Report should be serious. This year's is like Harry Potter.

Annabel Crabb: Finally, the Great Autumn Budget Inoffensive has begun.

Given we've seen improvements in the very demographic problems the Intergenerational Report was created to address, why does this week's report still point to a fiscal challenge?

Reuters photo of the year – a stunning image.

Jim Cramer says he was itching to recommend eBay, but this story about its mobile payments business, Venmo, has him worried.

Paul Krugman: Politics and the BMI, or the correlation between obesity and voting Republican.

In Ferguson: “Just for the record, I am so over being teargassed.”

In Russia: another dead democrat.

In Washington: Netanyahu's unconvincing speech to Congress.

Enough of 4G already – Europe pulls together a plan for 5G – carved mostly from dreams.

The challenge of surplus capital.

Does the eurozone need Greece more than Greece needs the eurozone?

The arrival of negative interest rates has changed the attractiveness of being in the eurozone.

Varoufakis: we have a Plan B. Draghi: No, No No.

Greece Vs Germany: two competing national narratives.

A rare glimpse inside a Saudi Arabian prison – where ISIS terrorists are showered with perks and privileges.

Living the Saudi dream.

The lure of the Caliphate.

Managing the ISIS crisis.

Theologically the most interesting place in the world today is Silicon Valley. Its religion, and the ones coming out of Syria and Iraq, will take over the world.

If you've heard of Snapchat, you might think it's a just for sexting, but actually it's a giant threat to Facebook, Google and TV. This is a very interesting article.

The BBC documentary on Indian rape was banned, according to this Indian writer, because it showed that “we have the most sickening patriarchal mind-set in the world. We are offended by our own ugliness”.

The futility of always pushing yourself to be more, while at the same time trying to be content.

This is one crazy music video (it's the same group as the one responsible for Video of the Week No 2 above).

This is quite funny – about five seconds long.

A review of Bob Dylan's new album, Shadows in the Night. “Might suit people who like early Tom Waits”.

Here he is doing The Night We Called it a Day, from that album.

And for comparison purposes, here's some early Tom Waits, doing Waltzing Matilda, would you believe, in 1977. Nothing like Dylan, but amazing.

Some Saturday morning music: Elle King: To Be A Man.

Have you seen the Katering Show? These are two talented satirists, worth checking out. This is the sustainable, ethical episode: being vegan is clearly insane.

Last Week

By Shane Oliver, AMP

Investment markets and key developments over the past week

While European shares continued to power ahead over the past week helped by continued good news out of Europe, most major share markets saw a bit of profit taking push them slightly lower. This included Australian shares which after almost touching the 6000 mark for the ASX 200 fell back, partly in response to the RBA leaving interest rates on hold. Bond yields generally rose, commodity prices were mixed with the iron ore price falling below $US60/tonne and the $US continued to drift higher, which weighed on the $.

While the US is gradually moving towards a rate hike and Brazil hiked its official interest rate to 12.75 per cent over the last week, the predominant trend remains towards global monetary easing with India and Poland cutting interest rates hot on the heels of China. In fact two thirds of the world's population saw an interest rate cut in the last week. Brazil's counter trend rate hike reflects the mess its economy has sunk into after years of populist policies that have led to chronic inflation and poor productivity.

China's announcement that its growth target for this year is “about 7 per cent” was hardly surprising. This in fact was already our own forecast and the IMF's forecast is 6.8 per cent. The Chinese Government is simply managing a downshifting in growth to a more sustainable pace. Don't forget though that 7 per cent is still world beating growth and given the rapid growth in the Chinese economy in recent times 7 per cent growth is equivalent to around 14 per cent growth about ten years ago in terms of China's demand for global resources.

In Australia, the latest Intergenerational Report provided a yet another reminder of the need to boost productivity growth and bring the budget deficit under control before the aging population really starts to blow the deficit and net debt out (to 6 per cent and 60 per cent respectively of GDP by 2055 on unchanged policies). However, it really tells us nothing that the first IGR in 2002 didn't. The sad thing is that since the first IGR (which had similar deficit and net debt projections over 40 years) we haven't really made a lot of progress in either boosting productivity or controlling the budget despite immense help in relation to the budget from the mining boom. Hopefully, we will start to see more progress out of Canberra, but this is likely to require a political consensus for change that currently appears to be lacking.

While the RBA left interest rates on hold, its post meeting Statement indicated a clear easing bias stating “further easing of policy may be appropriate” and with economic growth remaining sub-par we expect it will act on this bias in either April or May.

Major global economic events and implications

US economic data was messy with softer readings for the ISM manufacturing conditions index, construction spending and vehicle sales but good reads for the services conditions ISM and PMI and employment. The overall impression remains that the US economy is solid but not taking off. This gives the Fed plenty of time regarding the first rate hike, with Fed policy makers now wavering between June and September.

The strength of the US financial system is evident from the Fed's latest bank stress tests which found that all 31 banks tested had sufficient capital to survive a prolonged economic downturn.

Good news continues to flow out of Europe. While Greek funding remains a bit of a short term issue, eurozone economic data continues to improve with strong January retail sales, a slight fall in unemployment and some lessening in deflationary momentum. Thanks to lower oil prices, the lower euro and QE even the ECB is starting to feel more upbeat and in fact has raised its growth forecasts for this year and next to 1.5 per cent and 1.9 per cent respectively. They could even be too pessimistic.

India saw some more good news with a Budget focussed on infrastructure spending in the context of ongoing fiscal consolidation, the formal adoption of inflation targeting for the Reserve Bank of India and another interest rate cut. While Indian shares seem to be always expensive its impressive fundamental developments and strong earnings growth help support this. India remains attractive compared to Brazil (which is suffering from a return to traditional Latin American populism) and Russia (which has shot itself in the foot, on purpose it seems).

Australian economic events and implications

Australia saw a data avalanche, with the key message being that growth remained sub-par at 0.5 per cent quarter on quarter or 2.5 per cent year on year In the December quarter. On the one hand the Australian economy has not had the recession some feared following the end of the mining boom and non-mining activity has accelerated led by home construction with record high building approvals in January indicating that there is more to go. On the other hand growth is clearly sub-par with mixed PMI readings and some loss of momentum in retail sales indicating that more help – from lower interest rates and a lower dollar – is needed. Fortunately inflation remains benign according to the TD Securities Inflation Gauge and February house price data from RP Data shows that house price gains are concentrated in Sydney with other cities seeing far more modest gains – all of which suggests that the RBA has plenty of flexibility on rates.

One stat caught my attention as interesting over the last week. Despite the collapse in export prices the current account deficit at 2.4 per cent if GDP is about as low as it's ever been since the early 1980s. This is a good sign that the slump in commodity prices has not made the economy vulnerable to a withdrawal of foreign capital. In fact it seems to be becoming less vulnerable.

What's happened to Australian petrol prices? Yes the bounce in the Tapis crude oil price to $US63/barrel (from a January low of $US47/barrel) has justified a bounce in the petrol price but even when allowing for the Australian dollar around $0.78 my calculations suggest the petrol price should be around $1.18/litre not the $1.32/litre I have been seeing in Sydney this past week. Something slippery going on here.

Next Week

By Craig James, Commsec

Variety of indicators for release in Australia

A bevy of economic indicators are scheduled for release in the coming week. Arguably the employment figures on Thursday are the stand-out, but all indicators are relevant in guiding the Reserve Bank's deliberations on interest rate settings.

The week kicks off on Monday when ANZ releases data on job advertisements for February. In the past the data was useful as a lead indicator on employment and the broader health of the job market. But some of the predictive power has been lost in recent years with budding job seekers now using social media, company websites and employment agencies more often to find positions. Still, job ads have risen for the past eight months, giving some sense that the job market is improving.

Also on Monday, holidays are observed in ACT, South Australia, Victoria and Tasmania.

On Tuesday the NAB business survey is released. The Reserve Bank has been a vocal critic of Corporate Australia, believing that companies should be less conservative, and instead lift spending, invest and employ rather than hoarding cash. So the NAB survey will be watched for signs of improvement in business conditions and confidence.

Also on Tuesday weekly data on consumer confidence is released. This will be the first survey to show how consumers have reacted to the Reserve Bank decision to leave rate settings unchanged in March.

On Wednesday, data on home loans (housing finance commitments) for the month of January is issued. The Bankers Association survey suggests that new loans for owner occupation (loans for people building or buying homes to live in) may have fallen 4.5 per cent in January. But the value of loans (investors and owner occupiers) may have eased only by 1 per cent in the month.

Also on Wednesday the Westpac-Melbourne Institute monthly survey of consumer confidence is released. This survey is now more a check on the weekly survey. But the survey is also useful each quarter for the special survey question on the wisest places to put new savings. At present Banks and Real Estate are favoured as the best places to put your money.

On Thursday the Bureau of Statistics (ABS) releases the February job market data. The ABS data has been criticised in recent months, but as always the trend data is best to watch as it smooths volatile monthly figures. We expect that jobs lifted by 18,000 in February after falling by 12,000 in January. And the jobless rate may have eased from 6.4 per cent to 6.3 per cent.

Also on Thursday, the Reserve Bank releases January data on credit and debit card lending. Consumers are using credit cards more often but paying off outstanding balances by the due date. And on Friday, broader lending finance data is issued, covering personal, business, housing and lease loans.

China economic data for February

Chinese New Year holidays are now a distant memory. The focus now is on the monthly download of economic data.

The week begins on Sunday when Chinese trade data for February is released. The trade surplus soared to US$60 billion in January, largely because of a slowdown in imports.

The procession of Chinese economic statistics continues on Tuesday with inflation data – producer and consumer prices. Inflation is low with consumer prices only up 0.8 per cent on a year ago. And on Wednesday, data on retail sales, production and investment is released. Investors will be watching for continued evidence of a transition from production to household spending.

In the US, the market-moving economic data is not released until later in the week. On Monday, the employment trends index is released while on Tuesday the JOLTS series on job openings is issued together with wholesale sales & inventories, weekly chain store sales figures and the NFIB survey of small business optimism.

And rounding off the first half of the week, on Wednesday the monthly data on the Federal Budget is issued together with the weekly report of mortgage finance commitments.

On Thursday, the ‘top shelf' indicators finally appear on the data calendar. February figures on retail sales are issued together with the usual weekly data on claims for unemployment insurance as well as data on export and import prices and business inventories. Economists expect that sales rebounded by 0.5 per cent after a 0.8 per cent decline – a decline driven by lower gasoline prices. Excluding autos, sales may have lifted by 0.4 per cent.

And on Friday, data on business inflation (producer price index or PPI) is issued together with consumer sentiment. The core PPI measure may have lifted 0.1 per cent in February after a 0.1 per cent fall in January. And consumer sentiment may have moderated further from 11 year highs, dropping from 95.4 to 94.5 in February.

Sharemarket, interest rates, currencies & commodities

Longer-term bond yields are a useful guide on economic conditions, especially inflation. Clearly a main concern for an investor looking to squirrel money away for a long period is the potential for value to be eroded by inflation.

On February 3, 10-year bond yields hit a generational low of 2.39 per cent (lowest since the 1950s), but have since lifted to 2.57 per cent. But whichever way you cut it, financial markets believe low inflation is here to stay.