Kohler's Week: US, Europe, Australia, Magellan, Ardent Leisure

- {{x.value}}

{{ twilioFailed ? 'SMS Code Failed to Send…' : 'Enter verification code' }}

{{ completedStep1 ? 'Authentication & Security' : content.trialHeading.replace('{0}', user.FirstName) }}

{{ content.upgradeHeading.replace('{0}', user.FirstName) }}

The email address you entered is registered with InvestSMART

Please login to continue

We have sent you an email with the details of your registration.

Looks you are already a member. Please enter your password to proceed

{{ upgradeCTAText }}

Updating information

Please wait ...

Your membership to InvestSMART Group recently failed to renew.

Please make sure your payment details are up to date to continue your membership.

Having trouble renewing?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

You've recently updated your payment details.

It may take a few minutes to update your subscription details, during this time you will not be able to view locked content.

If you are still having trouble viewing content after 10 minutes, try logging out of your account and logging back in.

Still having trouble viewing content?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

Please click on the ACTIVATE button to activate your Intelligent Investor 15-day free trial

Please click on the ACTIVATE button to finalise your membership

Unsuccessful registration

Registration for this event is available only to Eureka Report members. View our membership page for more information.

Registration for this event is available only to Intelligent Investor members. View our membership page for more information.

- You are already registered for this event.

- This event is already full.

- Please select a quantity for at least one ticket.

- {{ i }}

Forgotten password

Please enter your email address below to request a new password

- Indepth analysis of ASX listed shares

- BUY, Hold and Sell Recommendations

- Ideas Lab

- Special Reports

- Alan Kohler’s Weekend Briefing

- Interviews with CEO’s & top influencers

- Money Cafe and Talking Finance

- Super Advice and Q&A with Ask Alan

Last Night

Dow Jones, down ~0.3%

S&P 500, down ~0.18%

Nasdaq, down ~0.4%

Aust dollar, US78.1c

US GDP

The Commerce Department came out with its second estimate of fourth quarter, 2014, GDP growth last night – 2.2 per cent, down from the first guess of 2.6 per cent. It means that for 2014 as a whole, growth was 2.4 per cent, slightly better than the 2.2 per cent growth recorded in 2013.

So it turns out the 5 per cent and 4.6 per cent growth reported for the second and third quarters respectively were unsustainable, and not sustained. No real surprise there. Not much surprise about this morning's data either – Wall Street was expecting 2 per cent so, if anything it was a bit better.

Nevertheless the market fell a bit at first, no doubt as a result of the old perverse logic that better means worse because of the impact on interest rates.

The main takeaways from this morning's report are that the revision is mainly due to lower inventories, which is no big deal, and that consumer spending held up while business investment was better. That's why the eventual response from the market will be positive.

US Rates

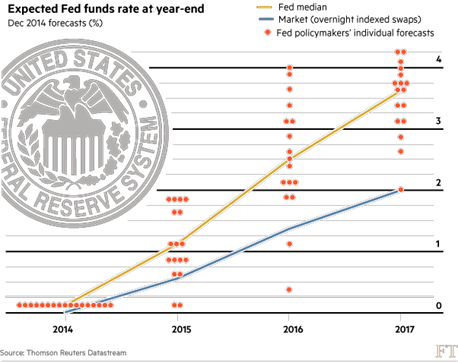

This chart sums up the US interest rate situation better than any others I've seen. Each dot represents a forecast from a voting member of the Federal Open Market Committee and the orange line is the median point of their opinions. The blue line represents the market's view, as shown by overnight indexed swaps, whatever the hell they are.

Two key points:

1. Everyone, except two FOMC members, thinks US interest rates will start rising this year;

2. The market disagrees with the Federal Reserve about how much rates will go up and how quickly.

Does it matter? Well, yes, because as Hamish Douglass says in my interview with him this week (see below), “macro" matters at the moment, and it is very difficult for share markets to rise when interest rates are going up. Markets won't necessarily fall, because the reason for rising interest rates is that the economy is doing well, but rising interest rates, especially the long bond rate, are a strong headwind.

Since mid-2013 the US economy has been firing on all cylinders. As we start 2015, the labour market is buoyant, credit conditions are easing, energy and credit costs are both at historic lows, and as a result, both business and consumer confidence are strong. Against that, US GDP growth, while still solid, lost some momentum in the December quarter because of the strong rise in the US dollar and weak economic conditions everywhere else in the world.

In her testimony to Congress this week, Fed chair Janet Yellen talked down the inflation/deflation problem, saying she was confident that inflation would return to normal over time – because of the surveys about inflation expectations and because of the outlook for growth.

Thus it was breathlessly reported that Ms Yellen “shifted her language”. She said that any modification to the Fed's language should not be taken as meaning that rates would start rising straight away, or words to that effect. This was taken to mean that the word “patience” is about to be extracted from the Fed's guidance.

Aha! “Patience” is about to go! The word rippled up and down Wall Street. Models were updated, calculators punched. What does it mean? Nobody actually has any idea.

So we end the week little wiser. As alert readers will be aware, I am negative about the prospects for inflation to resume normal transmission any time soon, so I would err on the side of interest rates taking longer to go up in the US. But really, anyone who says they know what's going to happen is having a laugh. The Fed is “data dependant”, as they say, which means it has no idea either.

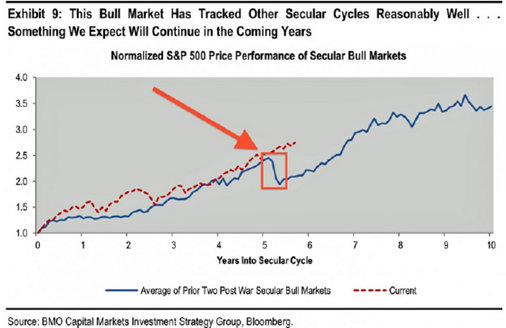

Correction potential

In that context, this chart is relevant:

Bull markets are not smooth, and the last two had a big correction roughly in the middle, which, according to this chart, is right about now.

I suppose it is just a reminder that you can unexpectedly lose a lot of money when you commit your savings to the share market. What causes such a fall? Usually nothing at all, sometimes something surprising.

For guidance on this matter, we turn first to Gerard Minack:

"First, markets face an asymmetric risk: they are increasingly betting that the Fed delays. Risk markets would presumably get some benefit if a delay is confirmed, but there seems more downside risk if Ms Yellen's testimony implies a mid-year tightening remains the FOMC's base case.

Second, if the Fed does still plan to tighten, despite the reasons/excuses not to, it suggests that it is partly motivated by concerns about the financial risks of maintaining zero rates. That would mark an important shift from prior policy.

Third, any hit to bonds from Fed tightening would be short-lived, in my view. The globe remains locked in low rates, and rising US yields would find buyers. Equities look more vulnerable. Equities are now expensive, and always de-rate when the Fed tightens (Exhibit 8).

Fourth, while other central banks will maintain easy policy, investors live in a dollar-dominated world. Fed tightening – particularly if it led to a higher dollar – would tighten global financial conditions.

Fifth – and most importantly on a long view – the peak in rates in any tightening cycle will likely be very low. Economies recovering from big crises tend to be fragile, and inordinately sensitive to policy tightening. For markets there is no precedent to judge the impact of ending six years of zero rates. A six-year king tide has probably encouraged a lot of naked swimming; if the Fed does tighten then that tide will start to recede.”

And speaking of naked swimming, we turn also to Jim Grant, editor of Grant's Interest Rate Observer. In a recent letter he refers to the rebirth of subprime lending in the United States, mainly for motor vehicles, or “non-prime” as it's called now (today's investment bankers shy away from the term subprime).

Says Jim Grant: “Could defaults exceed expectations?” asks Marty Fridson in a characteristically thoughtful analysis issued through S&P Capital LCD. “Yes indeed,” he replies in so many words, “and by a factor of three to four.”

Abundant liquidity has forestalled defaults. Grant: “Companies that would have missed an interest payment except for easy money didn't miss. The Federal Reserve wouldn't let them”.

Will another subprime debacle hit the markets? Eventually, yes, but as Jim Grant points out, any investment banker who decided to withdraw from the residential mortgage business in 2005 would have lost his job. It's true that they are once again refashioning less than high quality loans into marketable securities, but as we saw a decade ago, the music can play for longer than you expect.

Europe

Now that the immediate future of Greece has been resolved (but possibly not for very long), markets can focus on the upcoming European version of quantitative easing, due to kick off next month.

It will have two key effects:

1. The ECB will buy €45 billion per month of 2-year to 30-year government bonds, which is more than twice the aggregate supply of new bonds created by fiscal deficits (by contrast, the Fed's QE never exceeded bond issuance by US Treasury). That will reduce the risk of sovereign default to almost zero, and in turn will encourage a rebirth of cross-border investing – not just in sovereign bonds but a range of assets.

2. GaveKal Research explains that it will also act to reverse fragmentation of financial markets, when lenders retreat to their home markets, and therefore lead to a big drop in bank lending rates in Italy and Spain – which are currently about double those of France and Germany.

These things, plus the fact that Alexis Tsipras appears to be willing to at least bend, and possibly break, election promises in order to keep Greece in the euro, greatly reduce the risk that Europe will be the spark of the 2015 share market correction.

Australia

As is now sung around campfires and written into school textbooks, Australia came through GFC relatively unscathed. But it now seems to be our turn to do poorly while the rest of the world does well. Not that we are likely to have a local version of a GFC, thanks to our gimlet-eyed and purse-lipped bank regulators, but the performance of our currency does appear to reflect the relative performance of our economy.

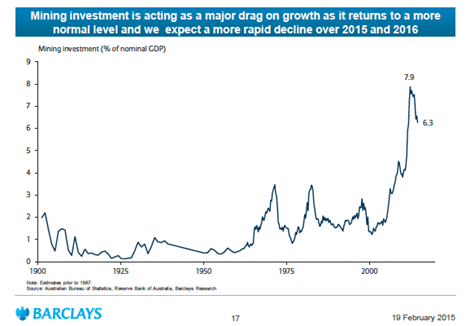

The latest exhibit is capital expenditure on Thursday, which showed an overall fall of 2.2 per cent. This was not so unexpected or problematic; it was the expenditure expectations for 2016 that caused concern.

Thursday's data implies a 15 per cent decline in capex in the 2016 financial year, versus 2015. All industries showed falls: mining down 20 per cent, manufacturing down 21 per cent (!!) and “other” down 7 per cent.

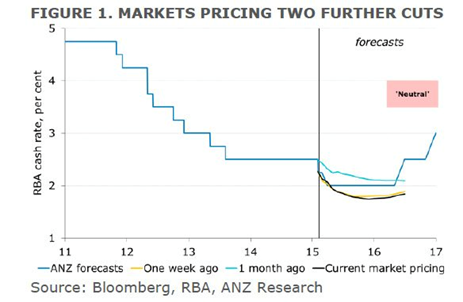

A pick up in non-mining investment is the foundation on which all improving forecasts of the Australian economy, particularly the RBA's, are built. After Thursday's capex data, forecasts were hurriedly lowered and the prospect of a rate cut next week were raised. It now appears to be 50/50 whether the RBA will cut on Tuesday.

I was asked by a lunch companion the other day (a mid-cap CEO) what my odds on a recession were. I replied “30 per cent” and then quickly amended that to 20 per cent. He was still shocked. It's getting on for a quarter of a century since we've had one – surely they have been abolished? Afraid not.

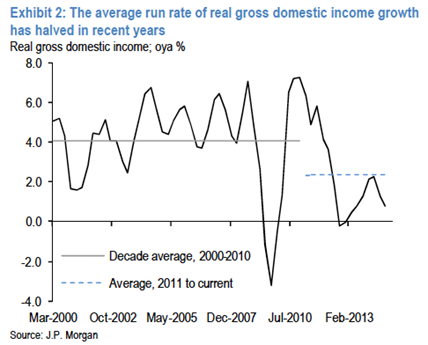

Mind you, it depends what you're measuring. Gross domestic income is already close to recession (see graph below), while gross domestic product, which is used for the definition of recessions, is being held up by the lower currency.

Here are a few charts that summarise where we are at:

Interview 1: Magellan

Hamish Douglass's international fund has been one of the best performing for years. This week Magellan launched what's called an Exchange Traded Managed Fund (ETMF), which is sort of an open-ended listed investment company. LIC's are closed-end, which means when you buy them, you have to buy units from someone else and you have to sell them to another buyer. With an ETMF, shares are issued or withdrawn to meet demand, so the price closely matches net tangible asset (NTA), instead of responding to demand supply for the stock itself. It means you can invest in Magellan “off platform” – that is, not through an adviser, which suits many SMSFs. Anyway Hamish explains all this in the interview. Here it is.

He's always worth listening to on the markets and global economy generally as well. A few choice quotes:

“Macro actually matters here in positioning yourself.”

"It's very difficult for markets to perform well when long-term interest rates are going up.”

"The reason rates will go up is because economies of the US are improving, so I think you want to be leveraged to the improvement in the US economy, like Lowe's and Home Depot.”

"I think the shape of the yield curve in two years to three years' time in the United States is the biggest unknown.”

Interview 2: Ardent Leisure

The market gave Greg Shaw a smack last week when he reported Ardent Leisure's results. The share price fell from $2.77 to $2.43 on that day (Wednesday) and then kept going, bottoming at $2.15. The price is now $2.41.

Since I'd spoken to Greg just last December, and some of you might have bought shares on the strength of that, as well as Matthew Kidman's strong recommendation, I thought I'd better get him back on to explain himself.

The shares were crunched because of poor performance in the company's health clubs. The Main Event business in the US is going fine but there are problems in the Australian gyms – they are being hit by competition from the new wave of 24/7, low-cost gyms. In a way it's a classic case of industry disruption.

Greg's got a plan to deal with the problem, which he explains in the interview, and more importantly he's building plenty of Main Event centres in the US, each of which makes $2 million cash profit (earnings before rent, interest, depreciation and amortisation) per year on a $7 million building cost. It is, in short, a gorgeous business.

As always, this is not a recommendation to buy the stock, merely a recommendation to watch the video. Here it is.

My portfolio

In the interests of full disclosure, here are my current asset allocations. To be honest, I thought my cash percentage was higher, but I wasn't including unlisted investments, which are now included (at cost):

Unlisted investments – 26.4 per cent

Listed investment companies – 17.1 per cent

Listed domestic shares – 30.4 per cent

International shares – 13 per cent

Cash – 13.1 per cent

My share portfolio may be inspected here, although there are two recent subsequent changes not yet on that list: I have sold Mesoblast and made a small investment in a speculative business called 3D Medical (ASX:3DM), which is a spin off from Capitol Health devoted to 3D printing technology as it applies to medicine.

The LICs are Thorney Opportunities, Ellerston Global and Bailador. The unlisted investments are the fractional property platform called DomaCom, which is expected to list later this year, a social media aggregation service called Stackla, now run from the US, and a collection of sports blogs called Fans Unite.

Quote of the Week

“In investing, what is comfortable is rarely profitable.”

- Rob Arnott

(thanks to Shane Oliver)

Politics

And finally, this is all you need to know about Australian politics at the moment:

Readings & Viewings

Video of the Week: this goes for 50 seconds and it's one of those videos where you think: is this real? If it is, it's incredible; if not, how the hell did they do it?

One of the dynamics at work in Janet Yellen's Congressional testimony this week, apart from her guidance on interest rates, was the ongoing attack on her and the Fed from the right wing of the Republican Party. Here is an impassioned, articulate defence of her from an independent economist (it's a PDF).

Five key quotes from Janet Yellen's report to Congress.

Ukraine's currency is totally collapsing. They'll halt trading in it any minute.

From the Oscars – Patricia Arquette's speech and the reaction to it: "The notion that Meryl Streep and Jennifer Lopez – literally some of the wealthiest and most powerful people in the world – should be cheering on yet another wealthy person about their struggle with low wages is hilarious."

And by the way, the host of the Oscars was shockingly unfunny.

“This is the greatest damn thing about the universe. That we can know so much, recognize so much, dissect, do everything, and we can't grasp it.” – Henry Miller.

Investors who held their nerve with Greece reaped the best bond returns.

What the FTSE closing at its highest level in 15 years means.

The Reserve Bank of Australia's claim that the Australian dollar is overvalued is not only wrong, it's disingenuous.

I've been quoting graphs from this fantastic speech by Andy Haldane, the chief economist of the Bank of England, but it's worth reading the whole thing if you have time.

The worst political interview ever – the UK Greens' Natalie Bennett on LBC radio. Oh it's so awful – gruesome listening.

John Fraser's first speech as Secretary to the Treasury. It was delivered yesterday to CEDA.

The Greek bailout may hinge on pursuing tycoons.

In the United States, just three out of ten workers are needed to produce and deliver the goods we consume. The rest of them spend their time planning what to make, deciding where to install the things we have made, performing personal services, talking to each other, and keeping track of what is being done, so that they can figure out what needs to be done next.

How might America look in 2060.

What the metadata thing is all about.

Beware of giving white collar crime agencies access to the metadata

How Samsung won the smartphone war, and then blew it.

Credit supply and the housing boom.

Why isn't the Fed more worried about inflation expectations?

The myth of Britain's housing crisis.

Krugman: explaining different recovery performances in Europe. By the way, it's his birthday today – many happy returns, Paul!

You might have heard about Twitter's meltdown yesterday about a dress that seemed to be either white and gold or black and blue. This piece in New Statesman explains it.

And the two women behind the dress definitively reveal its colour.

Antarctica's retreating ice may re-shape Earth.

Haruki Murakami on writing novels and Bob Dylan

Albert Einstein's incredible work ethos: lessons on creativity and contribution.

Google and tech's elite are living in a parallel universe.

Today is the 1547th anniversary of the death of Pope Hilarius. Funny guy.

Last Week

by Shane Oliver, AMP

Investment markets and key developments over the past week

Share markets rose over the last week helped by a combination of good news on Greece, benign comments from Fed Chair Yellen and reasonable economic data and profit results, capping off a strong month. Bond yields generally fell, but particularly so in Europe ahead of ECB QE starting up. Spanish 10 year bond yields are now just 1.28 per cent. Commodity prices were mixed and the Australian dollar fell slightly.

Good news on Greece as it received approval for a four month extension of its current loan program. The negotiation of a longer term program will have its ups and downs but ultimately see agreement reached around allowing Greece to run a lower budget surplus after interest payments.

Investors should allow that the constant commentary of doom and gloom regarding the Eurozone is misplaced and Europe is on the mend. ECB President Draghi rightly reinforced the latter with his comment that the "outlook [for Europe] is more positive that it was a few months ago". This is evident in Greek risks subsiding again, rising bank lending and rising confidence all helped by ECB monetary stimulus, the lower Euro and lower oil prices. This is important for investors. Eurozone shares are star performers this year, up 14 per cent already, and being unambiguously undervalued and likely to benefit from easy money, the lowered Euro and stronger growth are likely to see continued outperformance going forward.

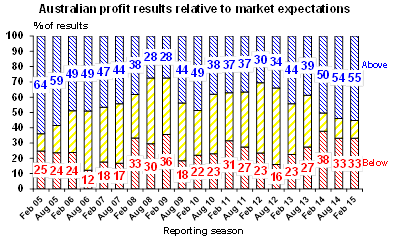

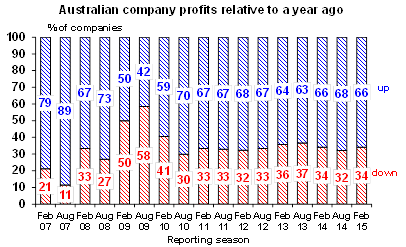

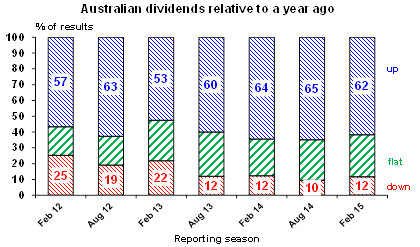

The Australian December half profit reporting season is now complete and while there have been lots of hits and misses, overall results have been better than feared. While we have seen the usual slippage in the quality of results towards the end of the reporting period, 55 per cent of results have beaten expectations against a norm of 45 per cent, 66 per cent have seen profits rise from a year ago, 52 per cent have seen their share price outperform the day results were released and 62 per cent have increased their dividends. Key themes have been ongoing tough times for resources and mining services companies, reasonable growth for the rest of the market helped by ongoing cost control, and solid growth in dividends. Earnings expectations for the current financial year are little changed. Sure resources profits are falling around 20 per cent, but this is a bit less negative than earlier expected. Meanwhile, banks are seeing profit growth around 8 per cent and industrials around 10 per cent.

Source: AMP Capital

Source: AMP Capital

Source: AMP Capital

Major global economic events and implications

US data was again a mixed bag. Housing data was messy with weaker existing home sales, but stronger than expected new home sales and a continued fall in the mortgage delinquency rates. Meanwhile consumer confidence fell but the services conditions PMI gained to strong levels and durable goods orders rose. The overall impression remains that the US economy is strong but it's not taking off. Meanwhile, Fed Chair Yellen provided a balanced view regarding monetary policy. While the Fed may be getting closer to replacing its "patient" comment regarding the first rate hike with comments to the effect that the commencement of the tightening cycle will be dependent on further improvement in the economy and specifically confidence that inflation will move back to its 2 per cent target over the medium term. In terms of inflation, January saw a slight dip into deflation but this was mainly due to lower fuel prices with core inflation unchanged at 1.6 per cent. A US rate hike is still on the way and could come in June but the risks are still skewed to a bit later - maybe September.

Japanese data for January saw weak household spending and a slight rise in unemployment but very strong industrial production.

Chinese data saw some good news with the flash February HSBC business conditions PMI rising to 50.1 from 49.7. Hard to get too excited though as it's been wiggling around the 48 to 50 level for several years now so really looks like noise.

Australian economic events and implications

Australian data was on balance a bit depressing. Sure skilled job vacancies gained nicely in January, credit growth is continuing to edge up and solidly rising residential construction is offsetting a slump in non-dwelling building and engineering activity, but the business investment outlook has deteriorated and wages growth has fallen to a new record low. In terms of capex, December quarter data showed another fall driven by the mining sector. But the really bad news was intentions data pointing to a roughly 8 per cent fall this financial year and a 12 to 16 per cent fall in 2016. While the ongoing slump is largely being driven by the mining sector where investment is falling at around 20 per cent pa as the mining investment boom continues to unwind, the disappointment next financial year is that the nascent improvement in investment by other selected industries looks to be fading. Clearly the fall back in business confidence of late has taken its toll. The weakness in the capex outlook against a backdrop of low confidence, record low wages growth, a rising trend in unemployment and a still too high Australian dollar points to the need for further RBA rate cuts.

However, there is no reason to get too depressed as there are several positives flowing through the economy including: lower rates, lower petrol prices and the lower Australian dollar. All of which should help demand in the economy and over time help turn around non-mining capex. Comments by BlueScope CEO, Paul O'Malley are instructive: “As the Aussie dollar gets into the 70s we get competitive, and with a year or two of that under your belt, you start to get the confidence to invest.” But the RBA does need to do its part and make sure the Australian dollar stays down and preferably falls further. This will need more rate cuts.

Next Week

by Craig James, Commsec

Bumper program of economic data releases

There is a strange quirk in the calendar of economic statistical releases. Every change in season is ushered in by a raft of data releases. So get set for the ‘Autumn Avalanche'. Over the next fortnight over a dozen pieces of economic data will be released together with a meeting of the Reserve Bank Board.

In Australia, the week kicks off on Monday when no fewer than five indicators are set for release. The latest gauge of manufacturing activity is released with the inflation gauge, data on home prices and new home sales as well as the Business Indicators publication from the Bureau of Statistics (ABS).

There are no standouts from these releases. The inflation data is important in determining inflation settings; data on home prices will reveal whether the Sydney home market is still ‘hot'; and the Business Indicators includes figures on profits, inventories and sales.

On Tuesday, the Reserve Bank Board meets to decide interest rate settings. Clearly another rate cut is a ‘live' option – indeed at each meeting over the next few months the Reserve Bank Board will no doubt discuss the benefits of cutting cash rates. Financial markets believe it's a 50:50 call whether rates will be cut again at the meeting.

In terms of economic statistics, data on tourism arrivals is expected with government finance, balance of payments and building approvals. The figures on government finance and the exports & imports figures will give some sense of how fast the economy grew in the December quarter.

The economic growth figures for the quarter are actually released the next day – on Wednesday. At this early stage we expect that the economy grew by around 0.5 per cent in the quarter or 2.6 per cent over the year. ‘Normal' economic growth is closer to 3 per cent and the ‘speed limit' for growth – the speed that the economy could grow without generating inflation – is probably closer to 4 per cent. So a soft economic growth outcome will keep the Reserve Bank poised to cut interest rates. The February data on new car sales will also be released on Wednesday.

On Thursday the ABS releases data on international trade (exports and imports) as well as retail trade (that is, spending at retail outlets). Retail trade is tipped to have lifted by 0.5 per cent in January.

US employment data in focus

In Australia, it is somewhat unusual to receive a rash of economic data in a short space of time – not so the US – it is commonplace. And in the coming week it is jobs data that hogs the limelight.

But it is Chinese data that kicks off the week. On Sunday, the National Bureau of Statistics releases gauges measuring activity in both manufacturing and services sectors. And HSBC releases its own versions of the data on Monday and Wednesday respectively.

In the US, the week begins with the release of data on personal income and spending on Monday while the ISM manufacturing gauge and figures on construction spending are also released. Little change in the manufacturing gauge is expected although personal incomes may have lifted 0.4 per cent in January, boosted by higher wages.

On Tuesday, data on new auto sales (cars and trucks) are released together with the usual weekly data on chain store sales. The ISM survey covering the New York area is also released on Tuesday.

On Wednesday, the Federal Reserve releases the Beige Book. This indicator is the usual ‘qualitative' survey of economic conditions released ahead of Federal Reserve interest rate decisions.

Also on Wednesday the usual weekly data on home purchase and refinancing is issued with the February figures on private sector employment from ADP. The ISM survey for the services sector is also issued. Economists tip a 211,000 rise in private sector jobs while little change is tipped in services sector activity.

On Thursday, data on factory orders is issued together with revised figures on labour costs and productivity and the usual weekly data on claims for unemployment insurance.

And on Friday, the February data on employment is released – the non-farm payrolls data. Economists expect that the good news on jobs continued in February with 243,000 new jobs created in the month. Unemployment may have eased to 5.6 per cent. Also on Friday the international trade data (exports and imports) is released with consumer credit (lending figures).

Sharemarket, interest rates, currencies & commodities

In the coming week, the profit-reporting or earnings season is transformed into the ‘economic reporting season'. And clearly the raft of figures will be important in dictating direction for interest rate and currency markets.

At present financial markets have fully priced in another rate cut to occur within four months. And financial market participants believe it's a 50:50 call whether rates fall by another quarter of a per cent (down to 1.75 per cent) by March 2016.

No one can claim it with any certainty – but the oil price does seem to be finding a base near $US50 a barrel. Whether oil holds at these levels is important for the energy sector.