Kohler's Week: Greece, Rates, Commodities, Disrupted, Buffett and IAG, Shameless Brag, Aveo, Rhinomed

- {{x.value}}

{{ twilioFailed ? 'SMS Code Failed to Send…' : 'Enter verification code' }}

{{ completedStep1 ? 'Authentication & Security' : content.trialHeading.replace('{0}', user.FirstName) }}

{{ content.upgradeHeading.replace('{0}', user.FirstName) }}

The email address you entered is registered with InvestSMART

Please login to continue

We have sent you an email with the details of your registration.

Looks you are already a member. Please enter your password to proceed

{{ upgradeCTAText }}

Updating information

Please wait ...

Your membership to InvestSMART Group recently failed to renew.

Please make sure your payment details are up to date to continue your membership.

Having trouble renewing?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

You've recently updated your payment details.

It may take a few minutes to update your subscription details, during this time you will not be able to view locked content.

If you are still having trouble viewing content after 10 minutes, try logging out of your account and logging back in.

Still having trouble viewing content?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

Please click on the ACTIVATE button to activate your Intelligent Investor 15-day free trial

Please click on the ACTIVATE button to finalise your membership

Unsuccessful registration

Registration for this event is available only to Eureka Report members. View our membership page for more information.

Registration for this event is available only to Intelligent Investor members. View our membership page for more information.

- You are already registered for this event.

- This event is already full.

- Please select a quantity for at least one ticket.

- {{ i }}

Forgotten password

Please enter your email address below to request a new password

- Indepth analysis of ASX listed shares

- BUY, Hold and Sell Recommendations

- Ideas Lab

- Special Reports

- Alan Kohler’s Weekend Briefing

- Interviews with CEO’s & top influencers

- Money Cafe and Talking Finance

- Super Advice and Q&A with Ask Alan

Last Night

Dow Jones, up 0.32%

S&P 500, down 0.06%

Nasdaq, down 0.61%

Aust dollar, US77c

Greece

As I have said many times, difficult negotiations always go to the deadline. The deadline for Greece is next week, and even then it's a floppy kind of deadline – entirely up to the IMF whether to declare Greece in default a minute past the June 30 repayment date or wait a while, pursing lips and making threatening noises etc. Why would anyone expect a deal to have been done this week?

A clue is provided by what someone told me in Athens in April (imagine this being said with a heavy Greek accent): “You negotiate in the basement, not on the balcony.”

The real negotiations about Greece are taking place in private. What's happening on the balcony, and thus is being reported breathlessly in the media every day, is something else – a piece of theatre for public consumption. It's possible the negotiations going on in the basement are about the extremely difficult task of extracting Greece from the eurozone, but I doubt it. No one wants that. More likely it's about how to construct an announcement that will pass muster with the voters of both Germany and Greece, and two more opposite groups of homo sapiens it is hard to imagine, so no easy task.

Apart from anything else the money that the IMF, ECB and EU are sitting on – about €7.2 billion – is actually Greece's. The “Troika” are withholding it to humiliate the Greeks some more and to punish them for electing a bunch of lefties and commies in January. The audience for this rollicking piece of theatre is the German public.

But in the end Greece will agree to some more pension reforms – the final sticking point – and will get some money from the IMF so it can repay it straight back to the IMF, and will then get some money from the ECB that it can pay straight back to the ECB. Alexis Tsipras might actually lose his job in the process, which would probably trigger another election which, in turn, might result in a better outcome than the dog's breakfast of the January one.

On Thursday they all adjourned the meeting to today (Saturday) and Angela Merkel said a deal must be done by Monday. Unless it's not done, of course, in which case it will have to be by, err, Wednesday? Um, OK how about next Monday?

Borders

On the subject of Greece, George Friedman had a really interesting piece in Stratfor this week putting together the Greek crisis, the Muslim immigration flood and the problems in Ukraine. He says they're all about borders, and what they mean.

With Greece there are two issues – one small, the other vast. The small one concerns capital controls. Greeks have been understandably moving large amounts of money out of Greece, but what sort of responsibility do they have personally for Greece's debts. Can they just escape all responsibility by getting their money out of Greece? In the case of Cyprus, the free movement of capital across borders was halted for that reason. As this video from the Wall Street Journal explains, Greek banks have had to borrow €113 billion from the ECB to give to Greek depositors taking their money out. That effectively adds to Greece's national debt – that is, the debts of those who haven't taken their money out.

The vast issue is the movement of goods. A big part of the reason for the crisis is free trade: Germany exports more than 50 per cent of its GDP and its prosperity depends of those exports. “…the inability to control the flow of German goods into Southern Europe drove the region into economic decline. Germany's ability to control the flow of American goods into the country in the 1950s helped drive its economic recovery.

"The essential principle of the European Union is that of free trade, in the sense that the border cannot become a checkpoint to determine what goods may or may not enter a country and under what tariff rule. The theory is superb, save for its failure to address the synchronization of benefits. And it means that the right to self-determination no longer includes the right to control borders.”

The problems with immigration and Ukraine are more obvious, but no less pressing:

"The refugee crisis has forced the Europeans to face a core issue. The humanitarian principles of the European Union demand that refugees be given sanctuary. And yet, another wave of refugees into Europe has threatened to exacerbate existing social and cultural imbalances in some countries.

"Who controls Europe's external borders? Does Spain decide who enters Spain, or does the European Union decide? Whoever decides, does the idea of the free movement of labor include the principle of the free movement of refugees? If so, then EU countries have lost the ability to determine who may enter their societies and who may be excluded.”

The Ukraine crisis is not really about Ukraine, it's about one of Europe's golden rules, introduced in 1945: that borders cannot be allowed to change.

However, Europe's contention, supported by America, that Russia is trying to change inviolable borders is hard to support, says Friedman. "Since the end of the Cold War, the principle of the inviolability of borders has been violated repeatedly — through the creation of new borders, through the creation of newly freed nation-states, through peaceful divisions and through violent war."

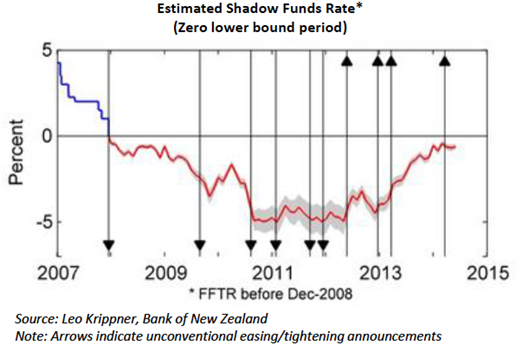

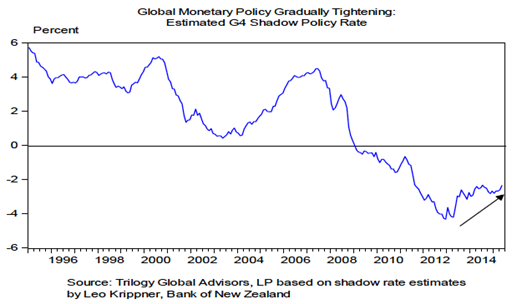

Interest rates

A Bank of New Zealand economist named Leo Krippner has developed a useful model for measuring the effect of “unconventional monetary policy” (QE, or money printing). He calls it the “shadow interest rate” – effectively he's boiling down the effect of QE into a theoretical interest rate, and then charting it over time.

Here's his chart of the US “shadow funds rate”:

And here it is for the “G4” (US, Europe, Japan, UK):

The point being that even though everyone's trying to guess when the Fed will start tightening, and markets are constantly reacting accordingly, monetary policy has effectively been getting tighter since 2012, which is the first time that's happened in a sustained way since 2004-2006 – which by the way eventually led to the crisis in 2008.

Not that I'm suggesting the current tightening cycle will lead to another crisis (although plenty of people are) but Leo Krippner's model explains why bond yields are rising.

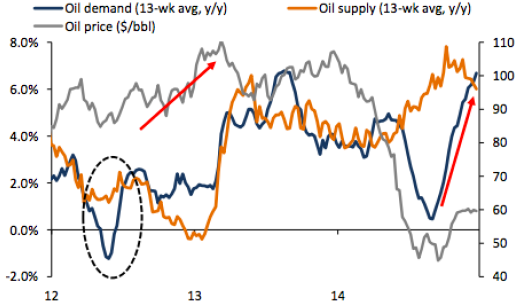

Commodities

A few brief points on some commodities.

1. Oil

The supply glut caused by US shale production and OPEC's refusal to cut back to compensate, which led to a fall last year from $US107 to $US44 in six months, has disappeared. The market is back in balance and the price has been holding at around $US60 a barrel for two months, having surged in March and April, but the risk from here is that it rises some more.

This graph from RBC Capital Markets shows what has happened: a massive surge in demand, and a small drop in supply.

Source: RBC

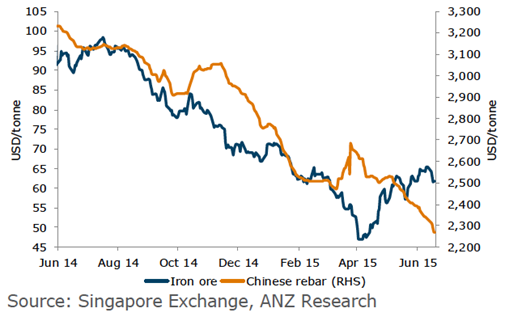

2. Iron ore

I've been watching the iron ore price and the Chinese steel price move in opposite directions – it can't last. Two weeks ago, the iron ore spot price had surged 40 per cent, before short selling took hold and brought it back to $US62, still up 32 per cent from the bottom in April. The Chinese steel price, meanwhile, has fallen 18 per cent over the same period, reflecting weakness in the construction market there.

There has been a large build-up of unsold housing inventory in China over the past few months, so the risk clearly is that the steel price will remain weak and that the iron ore price will crumble in the weeks ahead.

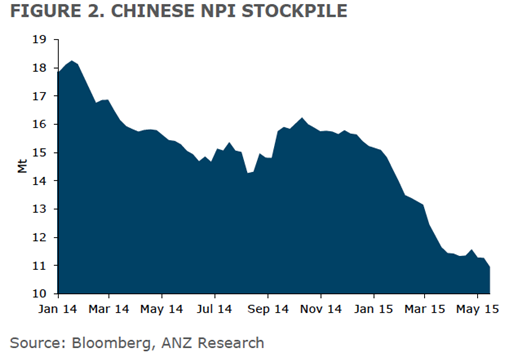

3. Nickel

Obviously the weakness in the steel market in China also applies to stainless steel, but there are other factors at work on nickel. Indonesia banned nickel exports last year and this has been gradually tightening the market. Chinese inventories of nickel feedstocks have been falling for a while and ANZ's commodities strategist, Daniel Hynes, reports that London Metals Exchange stocks are also starting to decline now. Chinese stockpiles of nickel pig iron (NPI) are down 40 per cent:

Weak Chinese steel demand generally is obviously a risk, but Hynes is bullish on the outlook for nickel in the medium term.

Disrupted

After last week's item on Uber, the ride-sharing platform, I received the following tragic email from a taxi driver. Below is my response, and then his response to my response.

Sir,

You are so misinformed regarding the Uberx platform it beggars belief! For a start the drivers are not licenced or certified to carry passengers in a commercial manner. The drivers have no background checks whatsoever or testing of knowledge of the city they operate in. All licenced taxi drivers across Australia have Police and background history checks made before they can even apply for a driver's certificate to drive a commercial passenger vehicle. The taxis they drive are commercially registered and insured as well. Uberx cars are not thus making any claim in case of accident null and void. This means (for the misinformed) that if you suffer an injury whilst traveling in an Uberx vehicle the State insurance company taking on the liability of injuries suffered can refuse payment to cover any injury sustained whilst traveling in that vehicle as it is not registered or insured for commercial use. Who would cover costs or compensation in case of serious or any injury?

Also the driver's vehicle insurance and any third party damage would definitely be refused on the ground that the vehicle were being used for gain and commercial use while not insured to do so. The owner and insured has an obligation and must notify the insurance company if the vehicle is to be used for commercial use!

How misinformed can a fool like you be! Get your facts correct before printing such a misinformed article such as I have just read! Then you have the audacity to say you would only put your family and children in a Uberx car and never a taxi, How irresponsible could a parent possibly be? You should be totally ashamed of yourself for putting in print an article such as that! Unconscionable and reprehensible behaviour by you and casting your misinformed opinion onto others. Disgusting journalism!

Dear …

Thanks for writing to me instead of slagging me off behind my back.

I'm afraid taxis have a problem, and it won't be solved by abuse, unfortunately. You may be right that insurance/injury risks will turn people back to taxis, but I don't think it's a good idea to simply hope for that. Taxis have to get better.

Hi Alan,

I agree with you that taxi drivers across Australia need to lift their game considerably in every aspect. In Victoria the regulator TSC and Government introduced a large number of reforms to the Transport Act commencing 30th June last year.

One of the most important reforms is a far more stringent manner of exam for knowledge test of Melbourne and a separate exam for customer service and courtesy expected of drivers. Believe me these examinations are tough! Of the first 274 drivers to sit these exams ONLY 4 passed! Also all drivers who have held a DC (accredited drivers certificate) for a period of less than five years must also sit these examinations on DC renewal. They have a three-month period to sit and pass the exams or their DC is suspended till they do so. I feel this is a fantastic initiative by the TSC for the future. The benefit of this new procedure will not be seen for a few years but will definitely enhance the service presented to the public. Give it time though.

Unfortunately many prospective drivers who have not had the ability to pass the new testing regime have gone to Uberx! Easy way out! Unfortunately for them they are being fined heavily when caught by the TSC or Vic Police. Uberx neglects to inform these drivers that they are in fact breaking the law of this state when they partake in this service. They also neglect to inform them of the insurance consequences if they are involved in an accident. A sad lack of information to some very gullible people often desperate for work.

I am totally disgusted with Uber in the manner they conduct their form of business in every aspect.

The bottom line is they are contravening the transport laws in every state of this country. Also if you care to check the recent press releases by the Insurance Council of Australia regarding Uberx and ride sharing it may give you an insight as to the driver's insurance status while operating that service.

If you would like any further information please do not hesitate to contact me. I have 33 years taxi driving experience in Melbourne. Regards...

As investors, we need to make sure we are not thinking like that taxi driver, who is understandably emotional because his life savings are tied up in an asset (a taxi plate) that is under threat from disruptive challengers skirting the legal frameworks that had previously protected him. People in the music business have been feeling the same way for a while.

As an investor you might have put hard-earned cash into a business that is getting disrupted now or could be in future, and it will feel unfair and your first response might be “fight" rather than “flight".

Don't. The world is changing. Get on the train; don't lie in front of it.

By the way, and a final note (for a while) on Uber – I note that the NSW Labor leader, Luke Foley, has introduced a private members bill to regulate ridesharing, including Uber, in NSW, saying: "Ridesharing has already been regulated in more than 24 jurisdictions around the world — it's time for this state to join that list''.

Buffett and IAG

My friend John Abernethy of Clime Asset Management put out an excellent note on Berkshire Hathaway's investment in IAG this week. Here's part of it:

"While Warren Buffett's recent investment in IAG Limited suggests that parts of the Australian equity market represent a growth opportunity, it also exposed how inefficient the Australian capital market has become. In this context, efficiency is not measured by price movement or price performance; rather it is measured by the ability, capacity or willingness of Australian capital to invest in or fund Australian business growth. In other words, the capacity of Australian capital to be patient and focused on the long term.

Buffett's investment in IAG created memories of his outstanding investments in Goldman Sachs and GE at the height of the GFC. Back then, he structured capital by way of high yielding redeemable, convertible notes with attaching warrants that ensured him a minimum return of 10 per cent per annum. He did not cap his upside; indeed, it was magnified by the attached warrants. His downside was protected by redemption rights and so the investments had the best of everything.

While the IAG investment may not be as good as his GFC deals, it is worth noting that his investment in IAG was not done at a time of crisis. Despite this, it looks a remarkably good deal for Berkshire Hathaway and a fairly average one for IAG. While it did raise capital for IAG, it also created the presumptions that IAG needed to supplement its capital, stabilise its underwriting risk and take the volatility out of its returns. IAG needed support and Buffett was there to provide it. That poses this question: Why didn't or couldn't the Australian capital markets, with our abundant availability of long term capital, supply the capital that IAG needed? Further, given that Buffett's great cash investment cow is the free float and cash generated by his insurance arm, then why hasn't IAG been able to do the same?

Buffett took a direct 3.5 per cent stake in IAG by way of subscription of a $500 million equity investment which secured the rights to 20 per cent of IAG's underwriting business. In doing so, Buffett secured entitlements as a minority shareholder that no other shareholder is entitled to. That is clever, because it elevated Buffett above all other IAG shareholders in terms of potential returns. However, there will be a cost to other IAG shareholders through dilution, and it is hard to see how they will improve their potential returns by doing this deal.”

You can read more at clime.com.au

Shameless brag

We're coming to the end of yet another financial year and I've been reflecting on the value that Eureka Report provides. It feels like we've done pretty well. There's been a lot of general analysis and debate, but also a lot of good calls as well.

Here are a few of them:

Stock buys

Capitol Health (CAJ), Vita Group (VTG) and AMA Group (AMA) are all up over 100 per cent. Netcomm (NTC) is up 70 per cent and Empired (EPD) is up 50 per cent.

European equities

In late 2014 the market was cautious on European equities, although we didn't concur. The European economy was on the mend, the ECB stood ready to support the market and stocks subsequently rallied 24 per cent -- easily outperforming Aussie equities.

Arista Networks

In March this year, we recommended Arista Networks (ANET US). Part of the call was that Arista, the classic smaller and nimbler disrupter, would take share from networking giant Cisco with a better product. Since then, Arista is up 27 per cent in USD on positive news flow and market share gains, while Cisco is down 3 per cent.

Amazon

At the end of 2014 we recommended subscribers buy online retail giant Amazon.

Subsequently Amazon reported a much better than expected 1Q 2015, and the stock rallied 14 per cent. In May this year, Amazon reported another great quarter but also broke out the Amazon Web Services metrics, and the stock jumped another 14 per cent. Since we recommended Amazon, it's gained 44 per cent in local currency to $US441.00. The S&P 500 in USD is up some 6 per cent during the same period. So an AUD investor purchasing the stock back then would have a 51 per cent gain. We maintain our buy opinion and target price (raised in May) of US$490.

Bank stocks

Investing isn't always about what you should be doing – sometimes it's about doing nothing while everyone else is panicking. Back in 2014 when the market was in the mood to sell off the banks, we suggested otherwise. From that time banks surged, with a peak gain of 20 per cent total return. Even allowing for the more recent sell off, banks are still 10 per cent higher from that point, outperforming the market as a whole.

NRW Holdings

NRW Holdings (NWH) has been a sell for us since late last year, from above $1.00. It recently ceased coverage at $0.18.

Each one of these calls on its own, if followed, would have paid for the subscription.

Over the last few weeks I've talked about some improvements we're making on July 1 that will add even more coverage to our recommendations – specific income stock and LICs coverage, model portfolios and interactive events.

To kick things off, we're holding a live webcast at 1pm on July 1 to talk about all the new features. James Kirby, Clay Carter and Simon Dumaresq will be joining me. Reserve your place here to find out how to get the most out of the new Eureka.

I'd encourage you to renew your subscription before that date though, because the price goes up then too.

Aveo

Last week I presented one type of retirement village business model, that of James Kelly's Lifestyle Communities; this week it's the more traditional model, being operated by, among others, Aveo Group. I interviewed its CEO, Geoff Grady, on the phone, so no video. You can listen or read the transcript of the interview here.

In simple terms, Lifestyle Communities sells the house and rents the land, taking advantage of the Government's rent subsidy for pensioners. Aveo, which used to be a Queensland based property developer named FKP, sells a lifetime lease and uses the more common model of deferred management fee and share of capital gain. Geoff came from the Malaysian property conglomerate called Mulpha, which owns 26 per cent of Aveo, as well as Hayman Island and Sanctuary Cove.

Rhinomed

This one's a video with no transcript, since I recorded it late yesterday and there hasn't been time yet to get the transcript done. It'll be available in a few days.

Rhinomed is trying to building a global business selling nasal stents – little plastic devices that go up your nose and hold it open, mainly to help stop snoring but there's also a market in helping athletes perform better and to also deliver drugs.

This is quite a funny interview, so worth watching for entertainment value I think. Is it worth investing in? Well up to you obviously, but Resmed has been a pretty good investment and Rhinomed is playing in the corners of that market (Resmed is about sleep apnea, Rhinomed is about snoring, which is a different thing), as well as opening up new markets. The little devices are cheap – $29 for a pack of three – and work out to cost about $1 a night.

As I explained in the interview, I tried one but it didn't work for me because my nostrils are different sizes, so the small one fell out and the larger one didn't fit. But CEO Michael Johnson patiently told me you can actually adjust them so you have different sized stents on each side, so I'll have another go. At the moment I use the adhesive strips called Breathe Right, which work OK, but maybe the little plastic thingies up the nose are better. I'll report back.

Watch the interview here.

Readings & Viewings

In a week when the final episode of Sarah Ferguson's fantastic doco “The Killing Season” aired, it's worth revisiting a nice piece by John Clarke and Bryan Dawe on a similar subject – Bob Hawke and Paul Keating. The points Clarke makes are just as relevant – more so – today.

This is wonderful – Walter Lewin's final physics lecture. It's long but worth it.

Mohamed El-Erian: 10 things you should know about the Greek crisis.

They're all blundering towards disaster, says Jeffery Sachs.

Here we go again – deficit spending versus austerity.

Michael Pettis: What can they be thinking? Remove Alexander Hamilton from the $10 note? Please Mr Lew don't do it!

Was the Trowbridge report on life insurance commissions a stitch up?

Here's Assistant Treasurer Josh Frydenberg's media release on the subject, detailing the proposed reforms, if you're interested.

The IMF recommendations on Australia are dumb and should be ignored – Adam Carr.

A Bloomberg report on the energy outlook – the five shifts that will shake the power industry (thanks to Vince M).

My mate Jonathan Green wrote this piece on the Zaky Mallah, Q&A hoo-ha this week. I thought it was pretty good.

These seven and eight-year-old sisters set up a lemonade stand and were shut down by the cops – not complying with Texas law. Then they found a loophole and re-opened (they have to give it away).

"Finally, property bubble proof", as if more were needed. It seems to be buyer's advocate, David Morrell, who says there is a bubble – “it just depends who is caught with the parcel”.

Uber's radical plan for driverless taxis.

A high level presentation on the future of energy, and Tesla, from the CFO of Tesla. Really interesting.

Building permits reveal meteoric rise of solar.

China's grand plan to harness the internet.

The white supremacist group that helped motivate Dylann Roof to kill people in North Carolina is tax exempt.

Answers to all the unresolved Game of Thrones questions (I'm a big GoT fan).

Zen and the art of money making (in China).

Mark Scott under siege (wrong Mark).

Denis Muller argues that in the argument about Q&A, free speech issues have become tangled.

The old Tony Abbott is back, and on top of his game.

America's corporations argued in favour of gay marriage, but last night's majority decision by the US Supreme Court legalising it was not based on the practical workplace problems raised by the companies, but on the fundamental principle of constitutional liberty.

Nice piece by Annabel Crabb on Magna Carta.

Paul Krugman on the Greek crisis: what do the creditors, and in particular the IMF, think they are doing?

A forensic examination of what happened to Greece.

Lately I've been enjoying the music of a Swedish duo (sisters) called First Aid Kit. Here they are performing their song “Emmylou” – not a dry eye in the house (I seem to get something in my eye whenever I listen to this too).

Last Week

By Shane Oliver, AMP Capital Markets

Investment markets and key developments over the past week

Shares had another volatile week with optimism about a Greek deal early in the week giving way to renewed concern as the saga continued. Eurozone shares held on to their gains from earlier in the week and Japanese shares rose to their highest since 1996 but US shares slipped and Australian shares fell after two weeks of gains. Chinese shares also saw continued volatility. Bond yields generally rose, except in peripheral Eurozone countries where yields fell on hopes of a Greek breakthrough. Commodity prices were mixed but the $A fell slightly as the $US rose.

The Greek saga continues. Despite numerous meetings Greece and its creditors failed to close a “reform for funding” deal. There are still grounds for optimism though: the war of words between the two sides seems to have been replaced with a more constructive dialog; the two sides have moved closer together with Greece giving a lot away with its most recent proposal and the creditors easing some of their demands regarding pension reform and offering a review of valued added tax hikes; and Greek PM Tsipras is taking it seriously in leading the discussions from the Greek side, but wanting to be seen as fighting for the best possible deal to the bitter end. And reaching a deal is in the interest of both sides. So our base case remains that a last minute deal will be reached. The timetable is very tight though as Greece and its creditors will need to reach agreement by the end of the weekend to leave time for the Greek parliament to vote on any deal ahead of the June 30 IMF payment and expiry of Greece's bailout program. If it's not all signed and sealed by June 30 but still on the way then it's understood there's various ways Greece could still make the payment, eg with the help of the ECB.

But if there's no deal, Greek banks will come under immense pressure, Greece will default on its payment to the IMF and others through July and talk of a Grexit will intensify. While a Grexit is not our base case, it's worth reiterating the rest of Europe is in far better shape now to withstand such an event than was the case through the 2010-12 Eurozone crisis so the fall out in financial markets should be limited. A note looking at the main issues around Greece, including what would happen if there is no deal is also attached.

What's driving low business investment and is it a threat? Recent research from both the OECD and the RBA has highlighted concerns about low levels of business investment both globally and in Australia. Clearly investment is essential for long term growth in per capita living standards. There are a range of reasons why it's currently depressed: hurdle rates to invest may be too high for a world of low nominal returns; the desire of more cautious shareholders post the GFC for capital return/dividends; the growth of capital light industries like IT; corporate caution after the biggest global recession since the 1930s; and in Australia the end of the mining boom at a time when non-mining companies are still shell shocked from the strong $A. Of these the desire of shareholders for capital return and dividends is not necessarily a bad thing as it guards against corporate hubris. But more importantly some of these factors are likely temporary so it's premature to get too alarmed. But if capex does not pick up in the years ahead it will be a concern.

Major global economic events and implications

US data was mostly good, but the growth rebound after the March quarter soft patch is still looking slower than that seen last year. Housing indicators remain solid, unemployment claims and weekly mortgage applications are continuing to improve and consumer spending was strong in May. But against this, the Markit business conditions PMIs for June fell to still ok levels but are well down from a year ago and underlying capital goods orders are rising but only modestly. While March quarter GDP growth was revised up to -0.2 per cent annualised from -0.7 per cent this is largely irrelevant because a seasonal reanalysis next month to remove chronic seasonal softness seen in March quarters will likely see it revised up to around 1 per cent. The basic message is that the Fed is on track to hike later this year, probably in September, but the trajectory of rate hikes is likely to be very gradual. This is not 2004, let alone 1994, when the Fed last embarked on rate hikes after significant easing cycles.

Eurozone business conditions PMI's for June were impressive. Despite all the noise around Greece the composite PMI rose to 54.1 its highest in three years, driven by gains in both manufacturing and services. This is consistent with a further step up in the pace of Eurozone GDP growth this quarter to 0.5 per cent quarter on quarter, compared to 0.4 per cent last quarter.

Japan's manufacturing PMI for June was disappointing, but other Japanese data was more positive with the unemployment rate remaining at its lowest since 1997, the jobs to applicants ratio rising to its highest since 1992 and household spending up strongly from its tax hike driven low a year ago. Core inflation remains too low though at 0.4 per cent year on year indicating pressure remains on the BoJ for more easing.

China saw some good economic news with the flash Markit manufacturing PMI up a bit more than expected to 49.6 in June and consumer confidence up 1 per cent in June. That said it's hard to get too excited as the PMI is still wallowing around in the same 48-52 range it's been in for four years now.

The overall picture from the global manufacturing PMIs released so far for June is that global growth remains uneven (with falls in the US and Japan, but gains in Europe and China) and still modest, but is okay. In some ways this is good, too weak and we worry about recession but too strong and the risks swing to inflation and aggressive central bank tightening.

Australian economic events and implications

Official home price data for the March quarter confirmed that growth is mainly being driven by Sydney. While home prices in Sydney rose 13 per cent over the year to the March quarter, the average pace across the other capital cities is just 2.2 per cent. All Australian cities suffer from poor affordability, but after a couple of years of double digit gains the Sydney market is looking a bit bubbly with buyers seemingly getting attracted by the pace of gains. It clearly needs to slow. Moves by the NSW Government to speed up land release and channel some of its stamp duty windfall into infrastructure for public housing projects are positive moves. The pressure also remains on APRA and hence the banks to slow lending for property investors particularly into the Sydney property market. Assuming this is successful, the benign home price growth being seen outside of Sydney is certainly no barrier to another RBA rate cut.

Job vacancy reports provided contradictory messages, but we are still looking for more constrained jobs growth ahead than seen over the last year. Population growth also appears to be slowing providing another pointer to constrained economic growth. My view remains that another rate cut is a 50/50 proposition. July is out but watch the August RBA meeting.

Next Week

By Craig James, Commsec

The financial year draws to a close

The 2014/15 financial year ends on Tuesday and there will be the usual navel-gazing on the year's results. There is also a healthy schedule of economic data over the week.

In Australia, the week begins on Tuesday when the Bureau of Statistics (ABS) releases two ‘big picture' publications. The first ‘Australian Industry (2013/14)' provides insights into industry performance and structure. And the second, ‘National Regional Profile (2009-13) includes regional economic data.

On Tuesday the Reserve Bank releases the financial aggregates publication that includes data on lending (private sector credit) and the money supply. And Reserve Bank Governor Glenn Stevens delivers a speech.

On Wednesday, the ABS releases building approvals data for May. While volatile, building approvals is a forward-looking measure of building activity. On the same day, CoreLogic RP Data releases data on home prices for June – the timeliest and most accurate estimates of home prices. Based on daily observations, home prices probably rose by 0.7 per cent in June with Sydney prices up 1.3 per cent.

Data on engineering construction is also issued on Wednesday and will show that activity continues to ease back to ‘normal' levels after the mining construction boom.

On Thursday, the ABS continues to ‘catch-up' with tourism and migration figures, releasing estimates for April. The data for May will be released less than a week later on July 7, and by that time the ABS will largely be up-to-date in the provision of these key statistics that impact consumer spending and the job market.

Also on Thursday the monthly trade figures for May are issued. While the data on exports and imports don't generally move financial markets nowadays like they did in the past, the record trade deficit of $3,888 million in April did cause investors and traders to take notice.

And on Friday the ABS releases the May data on retail spending. This data covers the period when the Reserve Bank cut interest rates to record lows and the federal government delivered a stimulatory budget. So policymakers would hope a solid sales result for the month.

International: US employment in focus

US investors have a holiday-shortened week to look forward to with non-farm payrolls (employment) the highlight.

The week kicks off on Monday in the US with data on pending home sales and the Dallas Federal Reserve manufacturing index.

On Tuesday, the CaseShiller data on home prices is released with consumer confidence, the Chicago purchasing managers index (PMI) and measures of services sector activity in Dallas, and more broadly, Texas. Home prices are up 5 per cent on a year earlier while confidence may have edged higher from 95.4 to 97.3.

On Wednesday the ADP estimate on private sector payrolls is released, a precursor to Thursday's official data. The ISM and Markit measures of manufacturing activity are also released on Tuesday together with auto sales, construction spending and the Challenger survey of job layoffs together with the usual weekly data on housing finance activity.

On Thursday the official employment data for June is released – the non-farm payrolls figures. Job growth has been consistently strong and is tipped to have lifted by 225,000 in June after a 280,000 increase in May. The unemployment rate is also expected to have eased from 5.5 per cent to 5.4 per cent. If the data is any stronger, investors and economists will need to bring-forward estimates that the first rate hike won't be delivered until late in the year.

Also on Thursday data on durable goods orders is released together with the ISM New York index. The Independence Day holiday is taken on Friday.

In China, the official statistician (National Bureau of Statistics) releases the purchasing managers' indexes for both the manufacturing and services sector on Wednesday. The HSBC variant of the manufacturing index is also issued on Wednesday with the services gauge released on Friday.

Sharemarket, interest rates, currencies & commodities

The Australian sharemarket started 2014/15 with the All Ordinaries at 5,382.0 and the ASX200 at 5,395.7. Currently the All Ords is near 5,672.7 points (up 5.4 per cent) with the ASX200 at 5,686.8 (up 5.4 per cent).

Of the 21 current industry sub-sectors, 15 sectors are currently higher over 2014/15. The key under-performer has been Energy, down by 19.0 per cent, followed by Capital Goods (down 18.6 per cent) and Media (down 15.7 per cent). Strongest growth has been by the Consumer Durable & Apparel sector (up 47.1 per cent) followed by Pharmaceutical & Biotechnology (up 34.9 per cent) and Transportation (up 32.9 per cent). The large Banks sector has lifted just 3.8 per cent with the Resources sector down 15.2 per cent (largely Materials & Energy) but the A-REIT sector (Property Trusts) has lifted by 21.3 per cent.