Kohler's Week: Draghi Does Dallas, Volatility, Deflation, Australian dollar, CEO Interviews

- {{x.value}}

{{ twilioFailed ? 'SMS Code Failed to Send…' : 'Enter verification code' }}

{{ completedStep1 ? 'Authentication & Security' : content.trialHeading.replace('{0}', user.FirstName) }}

{{ content.upgradeHeading.replace('{0}', user.FirstName) }}

The email address you entered is registered with InvestSMART

Please login to continue

We have sent you an email with the details of your registration.

Looks you are already a member. Please enter your password to proceed

{{ upgradeCTAText }}

Updating information

Please wait ...

Your membership to InvestSMART Group recently failed to renew.

Please make sure your payment details are up to date to continue your membership.

Having trouble renewing?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

You've recently updated your payment details.

It may take a few minutes to update your subscription details, during this time you will not be able to view locked content.

If you are still having trouble viewing content after 10 minutes, try logging out of your account and logging back in.

Still having trouble viewing content?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

Please click on the ACTIVATE button to activate your Intelligent Investor 15-day free trial

Please click on the ACTIVATE button to finalise your membership

Unsuccessful registration

Registration for this event is available only to Eureka Report members. View our membership page for more information.

Registration for this event is available only to Intelligent Investor members. View our membership page for more information.

- You are already registered for this event.

- This event is already full.

- Please select a quantity for at least one ticket.

- {{ i }}

Forgotten password

Please enter your email address below to request a new password

- Indepth analysis of ASX listed shares

- BUY, Hold and Sell Recommendations

- Ideas Lab

- Special Reports

- Alan Kohler’s Weekend Briefing

- Interviews with CEO’s & top influencers

- Money Cafe and Talking Finance

- Super Advice and Q&A with Ask Alan

Last Night

Dow Jones, down ~0.6%

S&P 500, down ~0.4%

Nasdaq, up ~0.2%

Aust dollar, US79.2c

Draghi Does Dallas

Yesterday's least surprising news was that the European Central Bank will follow the Federal Reserve down the path of 'printing' money and buying bonds – at the rate of about €60 billion a month until at least September 2016, or "until we see a sustained adjustment in the path of inflation which is consistent with our aim of achieving inflation rates below, but close to, 2% over the medium term". (And yes I know the Fed is not based in Dallas).

It was not a surprise because the plan to do QE had been carefully leaked but not the amount, which was held back so there could be a bit of a surprise to get a spurt from the markets. Also there was the surprise that Draghi said the ECB could, and probably would, buy at negative yields. The Dow Jones and the European Stoxx 50 both duly rose 1.5% because the amount will be at the upper end of the (manipulated) expectations. The local market gapped 1% higher on the opening yesterday, with a 3% fall in the crude oil price overnight holding it back a bit, and then it closed 1.4% higher.

The Dow has slipped back slightly this morning but European markets have had another huge session. The Stoxx 50 is up 2%, with Athens the biggest mover – up 6%. The euro hit an 11-year low of $US1.11 and bond yields also tumbled. German 10-year bunds now idle at just 0.35%. European markets are celebrating mainly because the commitment is open-ended. The ECB has basically promised to keep buying bonds forever if necessary, just as the Fed did in its third and final ‘QE Infinity'.

The Fed announced QE3 on November 16, 2012. Wall Street corrected for two months while markets worked out that it was real, and then started rallying and didn't stop. The S&P 500 has increased 51% since in more or less a straight line. The German market has actually outperformed it but only because in the past few months it's been rallying in anticipation of European QE. The Australian market has risen 25% since November 2012, including a 20% fall by the resources index.

There's no reason to think European stocks won't keep going for a while, although a lot of Mario Draghi's ‘QE Infinity' is priced in already. However it might not be a great place for Australians to invest because the euro is clearly heading south, so any gains for foreigners may be wiped out by currency moves.

The aim of QE, as I understand the topic, is to reduce the bond yield so that otherwise timorous risk-free investors are forced out along the risk curve – into riskier credit, equities and property. This, it is hoped, will drive up asset prices and drive down the currency, and thus improve confidence, and then lead to investment and activity, and therefore, at the end of this long chain, to higher inflation. Everyone is now doing some form of it, following the lead of the United States, which got stuck into the zero rate/money printing business six years ago and it has worked tolerably well. Or rather, the US is not in the same kind of poo that Europe is. As a result we have a global currency war, with multiple countries trying to bomb Pearl Harbor.

How much of Thursday's ECB announcement was priced in by the markets is hard to tell, but I suspect the euphoria evident yesterday will fade. Apart from anything else, the QE proposed won't be enough, according to experts who know these things. Societe Generale's economists have studied the matter and report that the ECB's QE will be five times less efficient than the US' one. That's because the US economy is more flexible, the US tackled the banking sector's problems in a much more determined and effective way, it has an effective bankruptcy regime and a clear single institutional framework for monetary policy. SG reckons that to work, Europe's QE would need to be €2 trillion-€3 trillion; the ECB is planning not much more than €1 trillion.

Beyond that, I'm not sure that any amount of QE, either in Europe or the US, will produce the desired consumer price inflation of 2%. It's certainly doing wonders for asset price inflation, although that probably has a time limit as well, but the CPI is the outcome of many more things than the volume of money. Central banks don't seem to have caught up with the news that Milton Friedman was wrong when he said that inflation is "always and everywhere a monetary phenomenon”.

Disinflation, and outright deflation, are the consequences not of a shortage of money, but of debt and productivity. Debt is deflationary because it encourages production, as firms increase output to keep the bankers at bay, and it discourages consumption as debt-laden consumers save their pennies. Demand is low and supply is high for products such as oil and transport services partly because there is still an excess of debt in the world. Meanwhile the central bankers' only means of increasing demand, and therefore inflation, is to encourage more borrowing by keeping interest rates at zero. This, to put it mildly, is counterproductive.

As for productivity and input costs, I have been writing for a while that automation, robotics, 3D printing and cloud computing - what are collectively called the Digital Revolution – are very powerful cost and price reduction forces. This is deflation that is not only good, it is right, and the attempts by central banks to stop it are not only doomed to fail, they are harmful.

In his latest newsletter, the inestimable Jim Grant of Grant's Interest Rate Observer, has joined this chorus in his usual droll way: “Progress has the full editorial support of these pages,” he writes.

“The trouble we see lies in the friction between human ingenuity and the … Federal Reserve Act. General computing power is doubling every 18 months or so, as Gordon Moore foretold. Yet, commands Congress, the Fed shall resist both rising prices and falling ones. The monetary mandarins have written their own codicil to the Act: They define ‘stability' as something other than stability, namely a 2% per annum rate of rise.”

He's referring to the Fed's dual mandate of price stability and full employment, adopted by most, if not all, central banks around the world, including the ECB and the RBA. What's more, they are all going for 2% inflation rather than actual price stability. It is, says Jim Grant, “doubly dated”.

“Moore's Law operates regardless of the size of the Fed's balance sheet. Baxter the robot goes to work regardless of the funds rate. The worldwide burden of debt, to which the dollar's rally against lesser brands of government scrip has measurably added, continues to climb."

So while the ECB's QE plan has galvanised markets temporarily, which is required because they need to be galvanised regularly in order to function, like the servicing of a car, it is doomed eventually to disappoint. Markets will rally for a time and the euro will depreciate, as it has already done by 20% in less than a year, but inflation will resist rising to the desired 2%.

And that's the main reason I'm optimistic about our investments: the deflation shouldn't hurt too much, and central banks will continue to fight it with liquidity and low interest rates, because that's what they do.

Bank dividend yields might even have to fall some more, which means more price rises for those stocks. We've already seen Telstra – a retail proxy for the government bond – surge by a dollar, or 20%, in three months as the actual Aussie bond yield has fallen from 3.7% to 2.6% in anticipation of lower inflation.

Volatility

Meanwhile volatility is rising because it is becoming clear that central banks don't actually know what to do. A year ago markets were calm in the knowledge that the Fed, the BoJ, the RBA and the ECB were all in the ‘whatever it takes' business and had the tools to do what it took.

Now we are not so sure. Their forecasts of economic growth, employment and inflation have all turned out to be wrong. They are torn between responding to lower unemployment (rates up!) and lower inflation (rates down!). And specifically markets can see that they are not getting inflation up yet.

So the question arises: if a central bank that we regard as infallible in a papal sort of way is doing ‘whatever it takes' to prevent something happening (deflation) then that something must be very bad. So what if they fail? That is bound, you would think, to create uncertainty and volatility, and so it is. Will it also lead to a major correction, and even a bear market? Possibly a correction, indeed corrections are an inevitable part of markets, but I doubt a new bear market. Mind you these are interesting times, and anything seems possible.

The problem is that while economic fundamentals seem supportive, the way they are being experienced by companies is far from uniform. Interest rates are low and falling, which is good for yield stocks; commodity prices are also low and falling, which bad for resources stocks; consumer prices are likewise low and falling, which makes life tough for firms in the business of supplying consumers. Meanwhile billions are being made by those at the forefront of technology – as the Wall Street Journal reported recently, the number of billion-dollar start-ups is currently twice the number during the boom years of 1999 and 2000. “2014 is the year the tech sector went into hyper-drive,” it explained.

Deflation

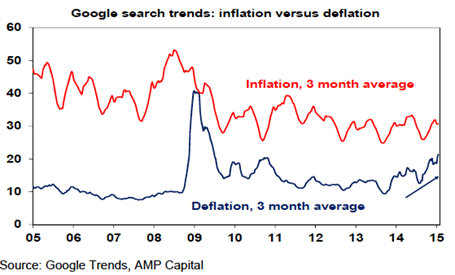

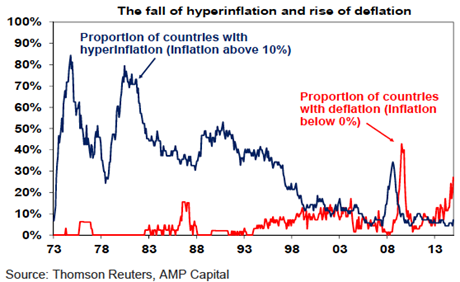

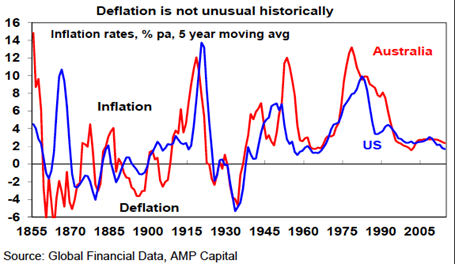

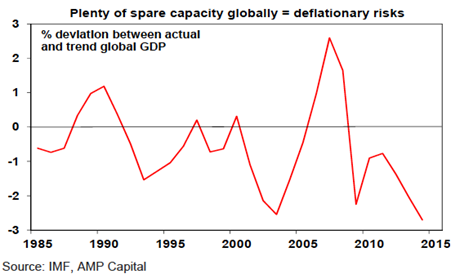

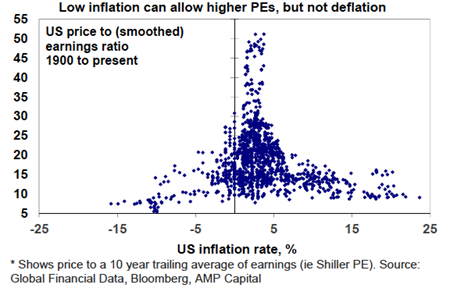

Our friend Shane Oliver of AMP put out a note during the week titled “The threat of global deflation”, which contained the following charts:

In other words: more people are getting interested in deflation, more countries have it, it was unusual in the 20th century but not unusual in the 19th century, the problem is the “output gap” – between actual and trend GDP, and history suggests it will result in lower PE ratios for shares.

As an aside, I'm not so sure about the relevance of the last chart: deflation, or low inflation, usually happens because the economy is in recession, which is when PEs are at their lowest. Global growth is a bit weaker than expected because of Europe and China, but recession? Maybe in Europe and possibly even Australia and Canada because of the fall in commodity prices, but not in the US. But as I said, these are interesting times, and anything at all is possible.

Australian dollar

The Aussie currency just spent its last week above US80c. It has now slipped quietly below US80c and will stay there until it eventually flirts with US70c – perhaps towards the end of 2015.

Why do I think that? Because it has only been held aloft by the last breaths of our AAA rating, which will soon have to be declared immaterial to the wellbeing of the nation, and the last dregs of resistance to an RBA rate cut, which won't be too far off now. The terms of trade are down for the count, so we have the double whammy of weak commodities and rate cuts expected. Even if the market starts to price in no rate hike in the US, as I expect, the Aussie is heading into the 70s.

My CEO Interviews

I received this letter from a member during the week:

"During the past year I have enjoyed watching your interviews with various CEOs of small companies. The CEOs got their messages across brilliantly. However I was rather foolish to follow up with significant investments in several of those companies and they have all tanked.

It would be worthwhile if you could get some of them back and ask them to explain their woeful performance since the interviews, in particular why they have tanked and more importantly what can shareholders expect as far as earnings go for y/e 2015 and 2016.

The companies are:

HIL, NNW, AZV and to a lesser extent BIT which has recovered somewhat recently.

I should have known better with HIL considering Pretty's rather woeful performance at Telstra.

Thanks & cheers, Peter.”

Hmm, that's not good. To be honest I haven't been following up the price performance of the companies I have interviewed, so wasn't aware that HIL (Hills Group) and NNW (99 Wuxian) had tanked, although I own some shares in AZV (Azure Healthcare) so I knew what was going on there. And I don't remember interviewing BIT (Biotron) at all.

Anyway, that letter prompted me to go back over the companies I interviewed in 2014 and see what happened to them. Patchy would be putting it kindly. Of the 46 companies I interviewed for Eureka Report last year, 24, or 52%, went down after the interview and 22 – 48% – went up. Eleven fell more than 10% and 15 went up more than 10%.

In other words, companies that I choose to interview can be taken as absolutely no guide whatsoever to whether it's a company worth investing in. It could just as easily be a stinker as a future CSL. As Peter indicated, CEOs are almost all very good salesmen and get their messages across brilliantly. Their spin should not be used as a basis for investing in any company. Almost all of those I have spoken to, including 99 Wuxian (down 45%), Newsat (down 70%) and Mint Payments (down 67%) talked up a storm, and I usually come away from every interview very impressed and thinking: “I really should buy some of those”. And then usually I think better of it (but not always).

So having done this exercise, I'm feeling a bit depressed and wondering whether I should keep inviting this motley crew of small cap CEOs into the studio to spruik their companies. I suppose I will, largely because I enjoy it and I hope you do too, and occasionally we all find a great business that makes it all worthwhile – like Slater and Gordon, or Sirtex, or Ardent Leisure, or Qube, and Godfrey's. I could go on.

The point is: this is why we have analysts. Simon Dumaresq, who joined us at the end of 2013, has an almost unblemished record of excellent stock picks in 2014 … because he does the work. He doesn't just talk to the CEO, he talks to lots of people and then sits down and prepares a model of the business, and forecasts the earnings independently of management. (You can see Simon's stock recommendations here). The same goes for Clay Carter and our new analyst James Hannam, formerly with JB Were.

Talking to the CEO can be entertaining, and informative, but it can never be the only basis for investing in a company – only the start of getting to know the company.

Sorry Peter. If you'd picked some of the other companies I'd interviewed, for example LNG or Capitol Health (one of Simon Dumaresq's picks as well) you would have done better. Thank goodness you didn't buy Newsat as well. And yes, I'll revisit the stinkers during 2015 and give them a pull-through, as we say at the ABC. I'll put them on the rotisserie and barbecue them till they're cooked.

Here are the performances of the companies I interviewed in 2014, from the date of the interview to yesterday:

OZ Minerals, January 25 – down 6.7%

Mesoblast, February 1 – down 33%

Mayne Pharma, February 15 – down 31%

Slater & Gordon, February 22 – up 28%

Sirtex, February 22 – up 74%

Ridley, February 29– up 17.7%

Newsat, March 8 – down 70%

NIB Holdings, March 22 – up 13.6%

Capitol Health, March 29 – up 30.9%

Xero, April 5 – down 54%

Bentham IMF, April 12 – up 15%

Orocobre, May 3 – up 22.3%

Hills, May 10 – down 36%

Mint Payments, May 17 – down 67%

Ardent Leisure, May 24 – up 4.9%

Xtek, May 31 – down 8%

LNG, June 7 – up 78%

Invocare, June 21 – up 10.5%

Monash IVF, June 28 – down 23%

99 Wuxian, July 5 – down 45%

Karoon Gas, July 12 – down 35%

Emerchants, July 19 – down 11%

Servcorp, July 19 – up 6.6%

Global Health, July 26 – down 54%

Thorn Group, August 2 – up 16.2%

AMA Group, August 9 – up 15.6%

Atlas Pearls and Perfumes, August 16 – down 51%

Azure Healthcare, August 23 – down 35%

Electro Optic Systems, August 30 – up 4.1%

Ingenia Communities, August 30 – down 14%

Ramsay Healthcare, September 13 – up 12.8%

RCG Corporation, September 20 – up 14.5%

Sirius Resources, September 27 – down 11.5%

Paragon Care, October 4 – up 21.4%

Infigen Energy, October 11 – down 14%

Medibank Private, October 11 – up 17%

Compumedics, October 18 – down 15%

BPS Technology, October 25 – down 10%

Bulletproof, November 1 – up 3.7%

Codan, November 8 – down 8.6%

Genera Biosystems, November 29 – down 4.2%

Billabong, November 29 – down 3.8%

Kip McGrath, December 6 – down 5.2%

Qube, December 6 –up 6.5%

Godfrey's, December 13 – up 3.1%

TFS Corporation, December 20 – down 4%

This week's interviews

1. John Sharman, Medical Developments International (MDV).

This company produces an analgesic inhaler for use in ambulances and emergency departments, called Penthrox. The active ingredient is a drug called methoxyflurane, which used to be used as an anaesthetic but was dropped in the 1970s. But although it's not so good as an anaesthetic, it's fine as an analgesic. It is a high margin, $30 product, prescription only, that John says is in every ambulance in Australia because it eliminates pain with six puffs (happily I have never come across it but apparently it works a treat and ambos love it).

The story John tells in the interview is that UK authorities have given “positive feedback” for the drug to be used in the UK, which would then lead to Europe. There is nothing like it in the UK and Europe, so he is optimistic about its prospects once the drug is fully approved, which he says it now will be. The share price jumped 6% after the announcement and stayed there.

I liked the story, and John, but as for whether we should buy shares in the company … see above. Anyway, you can watch the interview and read a transcript here.

2. Kim Lindsay, Lindsay Australia.

This is a more boring, but much more solid business – a rural transport and logistics operator based in Brisbane, with an interesting rural distribution and retailing business attached. It started as a family company 60 years ago, and the Lindsay family now owns just 17%. Rob Millner's group is the largest shareholder, with 36% split between Washington H Soul Pattinson and Brickworks. It has a PE of 15, a dividend yield of 6%, fully franked, and Kim is forecasting steady growth of 10%.

See the interview here.

Readings & Viewings

Er, last week I showed a video of this thing called a Cicret bracelet, which apparently projects a little screen on someone's forearm and acts like a smartphone, and I said “wow, this is incredible”. Well, it was incredible in the true sense of the word: turns out it doesn't exist. It's a fraud, a hoax, and I got taken in. Thanks for all those who wrote, chortling, to tell me.

I don't think this one's a hoax.

Good piece by Ambrose Evans-Pritchard on the currency wars, quoting a guy who predicted the Lehman crash with “uncanny accuracy”.

Excellent primer in the New Yorker magazine about quantitative easing: "Quantitative easing is basically Christmas for the financial markets…”

Albert Edwards, the chief strategist for Societe Generale, says deflation will overwhelm the west in 2015 and “markets will riot”. He's been wrong before.

When will the oil market find a bottom?

My piece during the week on the great superannuation lottery.

Venezuela should be rich, but its government has destroyed its economy.

Petrol prices go up like a rocket and fall like a feather. Get used to it.

A positive view about the future of work – maybe it'll make us happier.

Five years ago this week, the US Supreme Court decided to allow unlimited amounts of corporate spending in political campaigns. It was a devastating mistake.

How can we not mark George Orwell's death in this week in 1950 by remembering Knopf's priceless rejection of Animal Farm?

GDP is a very imperfect guide to a good society. Here are a few other measures.

Through the ages, inequality has moved in cycles. Crises seem to help to reduce it.

How low can oil go (those betting a lower price are starting to get nervous).

This is pretty funny - a columnist in the Daily Mail on what he got wrong, and right, about the invasion of Iraq. ("I still shudder to recall how close I came to supporting the Iraq war.”)

In Florida, a teenager impersonated a doctor for a whole month.

The “Doomsday Clock” is now three minutes to midnight, according to the Bulletin of the Atomic Scientists. What bollocks. This is the guy walking around with a sandwich board saying “The end is nigh”. It never is. Mind you, it's hard to argue with this statement: "international leaders are failing to perform their most important duty -- ensuring and preserving the health and vitality of human civilisation.”

The India story is finally taking off.

Zero Hedge's look at the impact of Saudi succession on oil, markets and politics.

Reign of the robots: how to live in the machine age.

Tony Abbott's trust deficit disaster.

Why has British politics turned into stand-up comedy?

Happy Birthday John Belushi, who died long ago, in 1982. Here's the “Somebody to Love” scene from The Blues Brothers.

Happy Birthday too, to Warren Zevon, who died in 2003. Here's Lawyers, Guns and Money.

Last Week

By Shane Oliver, AMP

Investment markets and key developments over the past week

Share markets had a good week driven by a strong quantitative easing (QE) program from the ECB along with good US data. This saw most share markets push higher. Chinese shares were the exception being hit earlier by a regulatory crackdown on margin trading. Bond yields fell sharply in peripheral Europe on the back of the ECB's bond buying program which also pushed the Euro sharply lower. The $A fell briefly below $US0.80 for the first time since 2009 on increased expectations for an RBA rate cut.

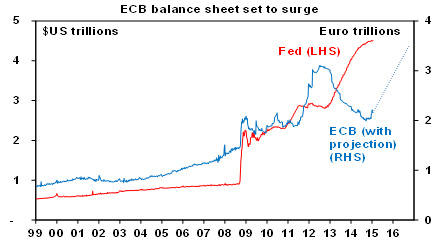

The QE announcement from the ECB was well above expectations. Key elements of the ECB's QE program are: €60bn/month in debt purchases involving both public and private debt out to September 2016 or until inflation is back on track; 80% of sovereign debt buying to be by national central banks but the remainder by the ECB resulting in partial loss sharing across Europe; and the TLTRO cheap lending program sweetened by removal of a fee. While the low level of loss sharing on public bond purchases is a dampener this was necessary to get German support and in any case is more than offset by the sheer size of the program. The ECB is now set to expand its balance sheet well beyond the 2012 level or €1trillion of QE that President Draghi last year implied was the objective.

Source: Bloomberg, AMP Capital

With public debt now included there is little doubt that this can be achieved. And the open ended nature of the program, ie until inflation gets back closer to target, puts it on a par with the Fed's successful QE3 program. As in the US, it is expected to work by boosting inflation expectations, displacing investors from low risk assets into higher risk assets and so boosting the availability of capital and asset values, helping support bank lending and via a lower than otherwise euro.

In short, the ECB's move gets the thumbs up. The scale and open ended nature of the announced QE program provides significant confidence that deflation in Europe will not be sustained and that its growth rate will get back to a firmer footing. This is good news for the global economy. So it's no surprise that shares rallied and it makes sense to continue overweighting Eurozone shares.

For Australia, the ECB's move is good news as it should help global economic growth and particularly China given that the Eurozone is its largest export market. While it is likely to reinforce demand for Australia's higher yielding and highly rated government bonds, coming on the back of a surprise interest rate cut by Canada it highlights that global deflationary forces remain intense and require further monetary easing and so RBA rate cut expectations have been given a further boost.

As expected the IMF followed the World Bank in revising down it global growth forecasts, but this tells us nothing new. The IMF's 3.5% growth forecast for 2015 is now in line with our own expectation. What is perhaps most interesting in the IMF's outlook is that in 2016 it sees growth in India exceeding that in China. Such a cross over underlines that India will become increasingly important for investors.

Finally, the passing of Saudi Arabia's King Abdullah is unlikely to change the outlook for oil prices with new King Salman likely to maintain current production levels as the country seeks to retain its long term market share.

Major global economic events and implications

US economic data was mostly favourable with solid housing data. US December quarter earnings are okay with 79% beating on earnings and 52% beating on sales but it's still early days and there have been some high profile disappointments.

In Japan there were no surprises from the BoJ which opted to continue with its massive quantitative easing program as is for now. However, further BOJ easing is likely to be required if it is to meet its 2% inflation target. The BoJ is effectively in an easing battle with the ECB – probably a good thing overall given the poor growth and deflation risks facing both countries.

China has slowed, but in a controlled manner and only to a more sustainable pace. December quarter GDP growth was in fact a little bit better than expected and resulted in 2014 growth of 7.4% which is in line with the Government's target. Growth in industrial production also perked up and retail sales growth remained robust. The January flash PMI also suggests that growth remains reasonable. But given the risks flowing from the property downturn and falling inflation, further interest rate cuts are likely from the PBOC and this should help ensure that growth this year comes in around 7%.

China's move to slow margin trading for shares was understandable as it has been growing too rapidly. But with Chinese shares remaining relatively cheap and the economy stabilising it's unlikely to mean the end of the bull market.

Australian economic events and implications

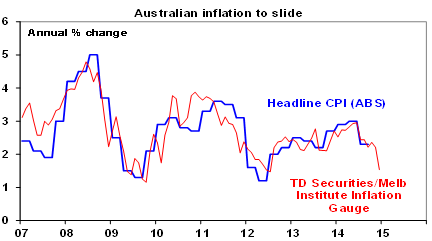

In Australia, the decline in inflationary pressures was highlighted by weakness in the TD Securities/MI Inflation Gauge. This is pointing to a sharp fall in official inflation.

Source: ABS, TD Securities/MI, AMP Capital

Meanwhile, consumer sentiment rose in January but given the sharp fall in petrol prices and better news on jobs the gain was modest leaving confidence well below its long term average.

While a February rate cut is unlikely, soft consumer confidence and weakening inflation support our view that the RBA will cut rates again. Canada's move to cut interest rates in the face of the oil price slump arguably adds to the case for an RBA cut because Australia has had a similar hit to its national income from lower commodity prices.

What to watch over the next week?

In the US, the Fed (Wednesday) is expected to reaffirm that it will remain patient in terms of when it will first start to raise interest rates and that it will be data dependent. While recent US economic and labour market data has been favourable it will be interesting to see how the Fed interprets the recent fall in core inflation. Our base case remains that the first hike will be in June, but with the risk of a delay.

Meanwhile, on the data front in the US expect gains in December durable goods orders, new home sales, house prices and consumer confidence (all due Tuesday) and pending home sales (Thursday). December quarter GDP (Friday) is expected to rise at a solid 3% annualised pace and the December quarter Employment Cost Index (also Friday) will likely also show continued modest growth.

In Europe, the main focus will be on the outcome of the Greek election (due January 25). Polls point to a win by left wing Syriza, but if wins it will be weeks or months before the outcome in terms of a Grexit from the Euro will be known. First, a Government will need to be formed (in 2012 this required two elections). Second, a period of negotiation with the Troika of the IMF, EU and ECB will then commence. Syriza is no longer seeking to leave the Euro as it knows that 70% of Greeks want to stay. But to stay it will have to reach agreement with the Troika on its budget and reform program and to do this it will have to compromise. The pressure to do this will be immense because to not compromise will see Trioka funding withdrawn resulting in even worse austerity and ECB support for Greek banks removed. So I expect a deal to be struck. And finally, if there is no agreement and Greece does leave the Euro, the threat of contagion to peripheral countries is far less than it was in 2012 as Portugal, Ireland and Spain are now in much better shape and the defence mechanisms in Europe are now far stronger with a strong bailout fund, a banking union and a more aggressive ECB.

Meanwhile, in Europe economic confidence indicators will be watched for further signs of stabilisation (Thursday) and the January CPI (Friday) is likely to show further modest deflation. Japanese economic activity data is expected to show further signs of improvement but inflation is likely to have slowed reflecting lower fuel prices (all due Friday).

In Australia, expect the December quarter inflation rate (Wednesday) to have fallen below target leaving plenty of scope for another RBA rate cut. A 7% slump in petrol prices is likely to have resulted in inflation of just 0.1% quarter on quarter or 1.6% year on year. Underlying inflation is also expected to be relatively weak at just 0.5% quarter on quarter or 2.1% year on year. Both headline and underlying inflation are expected to come in below RBA expectations.

Meanwhile the NAB business survey (Tuesday), trade prices (Thursday), producer prices & credit (Friday) will be released.

Next Week

By Craig James, Commsec

Spotlight on inflation

“Official” inflation data only comes around once a quarter in Australia. There is private sector monthly survey on inflation from TD Securities and Melbourne Institute but the Bureau of Statistics (ABS) only publishes its inflation measures once a quarter.

The Consumer Price Index for the December quarter is released on Monday. The authors of the monthly inflation gauge are tipping that prices rose 0.3% in the quarter and 1.8% for the year. The CBA Group is tipping a similar result ( 0.2%/1.8%).

Over the quarter, the price of petrol plunged by 6.3% and that alone will cut around 0.2 percentage points off the quarterly CPI change.

More importantly, investors will need to focus on the “underlying” measures that exclude petrol as well as the non-tradable price measures that focus on domestic price pressures.

We expect that underlying inflation grew 0.4-0.5% in the December quarter and around 2.1-2.2% over the year. Only if inflation threatened to undershoot the 2-3% target band would the Reserve Bank elect to deliver more stimulus.

The other readings on inflation are trade prices – export & import prices – released on Thursday, and producer prices, released on Friday. Both these measures are heavily influenced by changes in iron ore, oil and coal prices and the Aussie dollar.

The other indicator to watch in the coming week is private sector credit (or loans outstanding) to be released on Friday. We expect that credit grew by 0.5% in December, keeping the annual rate at 5.9%. This should be close to the peak for annual loan growth with Aussies still reluctant to take on new debt.

The US Federal Reserve hogs the limelight

The flow of Chinese economic data has dried up so the US takes centre stage. And not only is there a hefty schedule of data releases, the Federal Reserve meets to decide interest rate settings.

The week begins on Monday when the Dallas Federal Reserve releases a survey on manufacturing.

On Tuesday, more than half a dozen readings will be released in the US: “Super Tuesday”. Amongst the data are durable goods orders, a ‘flash' (current) reading on the services sector, home prices, consumer confidence, new home sales, weekly chain store sales and an influential survey from the Richmond Federal Reserve. Consumer confidence should be strong while home prices have lifted by 4.5% over the year and durable goods orders are tipped to have lifted by 0.5%.

Over Tuesday and Wednesday the US Federal Reserve meets and the decision is announced at 6am Sydney time on Thursday morning. Financial markets expect the Federal Reserve to lift rates around mid-year. And each meeting over the next six months we will gather clues on when that rate hike will occur.

On Wednesday, housing starts data is due in the US with annualised starts tipped to lift from 1.028 million to 1.04 million in December. New building permits are also expected to have edged higher in the month. The usual weekly data on mortgage finance is also released.

On Thursday in the US, data on pending home sales is released with the usual weekly data on claims for unemployment insurance.

And on Friday, the final January estimate for consumer sentiment is issued (currently at an 11-year high) together with data on employment costs, the Chicago purchasing managers index and the “advance” reading of economic growth for the December quarter. The current 5% annualised economic growth was never sustainable and the likely 3.3% annualised growth rate in the December quarter will be closer to the mark.

Sharemarket, interest rates, currencies & commodities

Across the Tasman, many were preparing ‘parity parties' – parties to celebrate the Aussie dollar going one-for-one with the NZ dollar. Well after reaching the strongest levels of NZ$1.035 per Australian dollar, the Kiwi has softened to levels above NZ$1.07. A low inflation result has reduced the imperative for Reserve Bank New Zealand to lift rates.

The US earnings season (release of quarterly earnings) continues in the coming week. Amongst companies reporting on Monday including tech giant Microsoft. On Tuesday earnings are tipped from Apple, Caterpillar, Yahoo, AT&T, 3M, Pfizer, Proctor & Gamble and DuPont.

On Wednesday earnings are expected from Boeing, Facebook and Qualcomm.

On Thursday, profit results are slated from Amazon, Ford Motor, Google, Time Warner, Viacom, Dow Chemical, and ConocoPhillips.

And on Friday, Chevron and Altria are amongst those expected to report earnings data.