Glencore-Rio: The deal of the decade?

- {{x.value}}

{{ twilioFailed ? 'SMS Code Failed to Send…' : 'Enter verification code' }}

{{ completedStep1 ? 'Authentication & Security' : content.trialHeading.replace('{0}', user.FirstName) }}

{{ content.upgradeHeading.replace('{0}', user.FirstName) }}

The email address you entered is registered with InvestSMART

Please login to continue

We have sent you an email with the details of your registration.

Looks you are already a member. Please enter your password to proceed

{{ upgradeCTAText }}

Updating information

Please wait ...

Your membership to InvestSMART Group recently failed to renew.

Please make sure your payment details are up to date to continue your membership.

Having trouble renewing?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

You've recently updated your payment details.

It may take a few minutes to update your subscription details, during this time you will not be able to view locked content.

If you are still having trouble viewing content after 10 minutes, try logging out of your account and logging back in.

Still having trouble viewing content?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

Please click on the ACTIVATE button to activate your Intelligent Investor 15-day free trial

Please click on the ACTIVATE button to finalise your membership

Unsuccessful registration

Registration for this event is available only to Eureka Report members. View our membership page for more information.

Registration for this event is available only to Intelligent Investor members. View our membership page for more information.

- You are already registered for this event.

- This event is already full.

- Please select a quantity for at least one ticket.

- {{ i }}

Forgotten password

Please enter your email address below to request a new password

- Indepth analysis of ASX listed shares

- BUY, Hold and Sell Recommendations

- Ideas Lab

- Special Reports

- Alan Kohler’s Weekend Briefing

- Interviews with CEO’s & top influencers

- Money Cafe and Talking Finance

- Super Advice and Q&A with Ask Alan

Summary: A possible merger between Rio Tinto and Glencore was the leading topic at London's biggest mining conference last week. Other dominant themes included a preference for base metals, reviving interest in Australian mining companies as the currency falls, and interest in companies with reasonable exploration prospects. |

Key take-out: Glencore could make a fresh merger bid for Rio Tinto some time after the Australian miner releases its full-year results in February. This could be a catalyst for a wider flow of deals necessary to start re-shaping the mining sector. |

Key beneficiaries: General investors. Category: Mining stocks. |

Low commodity prices will continue to depress Australian mining companies for at least the next eight weeks, but from February 12 there could be a change of sentiment as investors get a fresh whiff of what could be the deal of the decade.

The reason for selecting such a precise date is because that's when the world's second biggest mining company, Rio Tinto, releases its full-year results for calendar 2014.

And the reason Rio Tinto is so important to the rest of the mining sector is that it remains squarely in the takeover sights of the world's most aggressive commodity trading company, Glencore. February 12 is close to the time when Glencore will be legally able to re-launch its rejected bid for Rio Tinto.

Talked down in Australia, and dismissed by Rio Tinto management as a deal in which it has no interest, a potential merger with Glencore was the leading topic last week at London's biggest mining conference, Mines and Money.

While the rest of the event was predictably sombre, the attendance levels were surprisingly strong with delegate and exhibitors numbers down by around 10%, which is a reasonable roll-up given the glum state of the resources sector.

Fund managers were less obvious this year, but private equity managers were more conspicuous, which could be a sign that sidelined cash is getting ready to start hunting for bargains.

As with previous years the value in attending the conference was not in the formal talks. It came from testing the mood of the meeting and in assessing how investment banks and private investors see the year ahead, because London is the world's mining-finance capital.

This year, apart from pessimism about the outlook for iron ore and oil prices, there were five dominant themes:

- The near-certainty of a fresh approach by Glencore to Rio Tinto once a British takeover law requiring a six-month standstill between merger-proposal has passed (see Winning Rio).

- An expectation of accelerated deal flow as the mining industry restructures to cater for low metal prices.

- Increasing interest in companies with reasonable exploration prospects but in need of capital to advance their discoveries.

- A strong preference for base metals, such as copper, zinc and aluminium over the bulk minerals, such as iron ore and coal (see Morgan: Base metals to rebound first), and

- Reviving interest in Australian mining companies thanks to the falling value of the Australian dollar.

Most of those themes are known to Australian investors who are acutely aware of the collapse in the iron ore price over the past 12 months, and the collapse in the gold price in the years before iron ore was attacked by sellers.

Regular readers of Eureka Report will be particularly mindful of those past events because they were high on the list of topics at previous London conferences where delegates were first to identify both the gold price correction and then the iron ore price correction.

This year there was less talk about price corrections. This is good news in itself because it is a sign that international financiers believe that the resources sector is close to the bottom of the supply/demand cycle – though no-one was prepared to go so far as to tip an imminent recovery.

Robert Friedland, a US billionaire resource investor, was the leading optimist, as he often is, telling delegates that not all metals were depressed. Palladium, a precious metal with properties similar to platinum, was one of his preferred commodities – only don't look too hard to find an investment entry point, they're all but impossible to find.

But it was Friedland's outright rejection of negative sentiment which was a particular crowd pleaser: “Anybody who says the (mining) super-cycle is dead is an idiot – it's just been deferred for a little bit,” he said.

Outside the auditorium at London's Business Design Centre in Islington there were not many people who agreed with his ultra-optimism, but there were plenty of people who believe that the mining sector (or parts of it) are close to reaching a turning point, and that could come with a crystallising event such as a fresh move by Glencore on Rio Tinto.

A smaller case study of what corporate action can do for the share price of a mining company can be found in the “mid-tier deal of the year” awarded at the London conference to the management team of an Australian miner, Altona Mining.

In early July, Altona sold its Kylylahti copper mine in Finland to the Swedish miner, Boliden, for an eye-catching $112 million, roughly double the value placed on the project by the stock market.

Altona's chief executive, Alistair Cowden, said in his acceptance speech that the price was an example of “corporates being prepared to pay more than the market for quality assets in the current environment”.

The sale of the mine, and the cash injection into Altona, saw the stock rise by 30% from 17c to 22c immediately after the deal was announced, and continue rising to its latest price of 24c.

Small beer when compared with a possible multi-billion dollar move by Glencore on Rio Tinto but the effect on the target companies' share prices could be similar, and while it would be a brave observer to suggest that Rio Tinto's share price could rise by 30% from its current level the possibility cannot be totally discounted.

Nor could the effect of a mega-bucks deal between the two companies on the wider mining sector be ignored because of the infectious nature of mergers and acquisitions in the aftermath of a big transaction.

What was especially interesting to an Australian visitor in London was the difference in the way the Glencore/Rio situation is seen there because while Rio Tinto is treated as a local champion in Australia it is perceived as a serial failure in London.

Heavy write-offs after the disastrous acquisition of the Alcan aluminium business in 2008, followed by the equally embarrassing but less costly Mozambique coal deal write-offs – and now an excessive reliance for profits from a single division, iron ore, have tarnished Rio Tinto's reputation.

The company's management team, led by chief executive, Sam Walsh, has been busy over the past two weeks talking down past problems and promising a better financial performance in the future, but how he is going to do that while the iron ore price continues to fall is a question which worries institutional investors.

Two recent “rabbits” extracted from Walsh's hat, designed to please institutions, are forecasts that the company's aluminium division is starting to perform strongly and that Rio Tinto is extracting greater value from its portfolio of assets through an increased focus on marketing.

The problem with both of those promises is that the aluminium price remains low, despite a 10% rise over the past 12 months from US78c a pound to US86c/lb, while marketing is a specialty of Glencore and for Rio Tinto to say that it has suddenly discovered a way to create value by smarter marketing smacks of playing catch-up.

There is a third problem for Rio Tinto in convincing London fund managers that it has the best assortment of assets and best management team for the next phase of the commodity cycle – a comparison of its share price with that of Glencore.

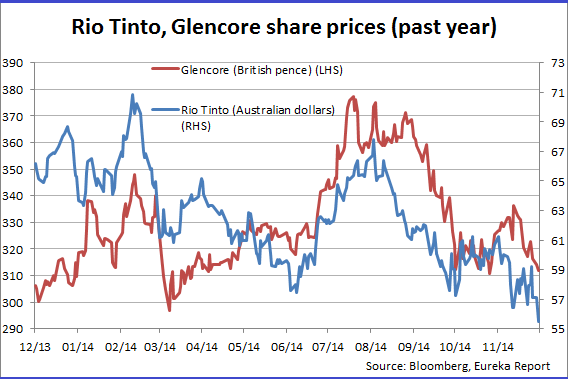

Over the past 12 months, as the iron ore price has collapsed, Rio Tinto's Australian-listed shares have fallen by 22% from a high of $71.30 to its latest price of $55.50. Glencore's share price on the London stock exchange has fallen over the same time by a less painful 17%.

As a simple measure of relative performance the respective share prices tell a story of Glencore, with its lack of exposure to iron ore and fee income from a big marketing operation, outperforming Rio Tinto – at a particular point in the commodity cycle.

Whether a merged business would deliver a better financial performance is the question being debated today with supporters of a deal claiming that up to $US1 billion in synergy benefits would be unleashed through using Glencore's bigger minerals trading division and through cost-sharing.

As a general rule Australian investors do not accept the claim of Glencore being the better manager, preferring to stick with Rio Tinto as it stands with ownership of world-class assets.

That's not the case in London where Glencore has a stronger following and has, so far, avoided making as many management mistakes as Rio Tinto.

Glencore's first approach to Rio Tinto was made in mid-July, and rejected a few weeks later. A fresh approach can be made early in the New Year, with Glencore's ultra-acquisitive Ivan Glasenberg unlikely to stir the pot until after Rio Tinto's 2014 result has been released.

That means more light will not be thrown onto the situation until early in the New Year, most probably sometime after February 12.

For Rio Tinto and Glencore it will be “game on”. For the rest of the mining sector the Glencore/Rio game could be the catalyst for a wider flow of deals necessary to start re-shaping the sector after three dreadful years.

Mining shares might be off the menu today, but expect an exciting return thanks to takeover activity in the first quarter of next year.