Flake news, flakey products

- {{x.value}}

{{ twilioFailed ? 'SMS Code Failed to Send…' : 'Enter verification code' }}

{{ completedStep1 ? 'Authentication & Security' : content.trialHeading.replace('{0}', user.FirstName) }}

{{ content.upgradeHeading.replace('{0}', user.FirstName) }}

The email address you entered is registered with InvestSMART

Please login to continue

We have sent you an email with the details of your registration.

Looks you are already a member. Please enter your password to proceed

{{ upgradeCTAText }}

Updating information

Please wait ...

Your membership to InvestSMART Group recently failed to renew.

Please make sure your payment details are up to date to continue your membership.

Having trouble renewing?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

You've recently updated your payment details.

It may take a few minutes to update your subscription details, during this time you will not be able to view locked content.

If you are still having trouble viewing content after 10 minutes, try logging out of your account and logging back in.

Still having trouble viewing content?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

Please click on the ACTIVATE button to activate your Intelligent Investor 15-day free trial

Please click on the ACTIVATE button to finalise your membership

Unsuccessful registration

Registration for this event is available only to Eureka Report members. View our membership page for more information.

Registration for this event is available only to Intelligent Investor members. View our membership page for more information.

- You are already registered for this event.

- This event is already full.

- Please select a quantity for at least one ticket.

- {{ i }}

Forgotten password

Please enter your email address below to request a new password

- Indepth analysis of ASX listed shares

- BUY, Hold and Sell Recommendations

- Ideas Lab

- Special Reports

- Alan Kohler’s Weekend Briefing

- Interviews with CEO’s & top influencers

- Money Cafe and Talking Finance

- Super Advice and Q&A with Ask Alan

Let's get the obligatory lyrical diversion out of the way first. Ukulele-hop band Twenty One Pilots believe that, “When you write music expressing doubt or concern, people come out of the woodwork to listen.”

Not so in finance, where the absence of doubt is a career-enhancing benefit. You can understand the compulsion from two perspectives. With an audience all ears and anxious for explanation, journos need answers; not necessarily the right ones, just something plausibile to fill the airwaves and column inches. The experts, meanwhile, have careers to forge and bonuses to make.

And so, after the S&P 500 had fallen 10.2 per cent over nine trading days since 26 January, our screens were taken over by those with a brief; to make the unknowable certain and to offer the appearance that someone, somewhere knows what the hell just happened and what will happen next.

Twenty One Pilots-style doubt doesn't last long under such conditions. If it did, we'd have a more honest, reflective financial culture. One where Bernie Madoff would be singing like a bird from his cell and Goldman Sachs wasn't a bank but a misogynistic glam rapper that got a taxpayer bailout each time he crashed his Lambo (kinda true, if you think about it). Instead, we get a cavalcade of finance bots excelling in ex-post rationalisation.

I'll freely admit that periods like this drive me crazy. Billy Bragg once sang that, “No one knows anything anymore”. In finance, where not many knew much to begin with, those that do know something also understand how much cannot be known. Such people, if they get a chance to speak, are not listened to. This is how foolish wars begin and fortunes are lost.

No one knows the precise causes of the recent sell-off. Individual investors have not been asked their reasons for bailing out. And they themselves might not know. Many people sell because it “feels right”. [If that sounds odd, ask yourself why you got married.] Nevertheless, we are overwhelmed by explanations for it.

Investing should be a fact-based exercise, so let's start there. What do we actually know?

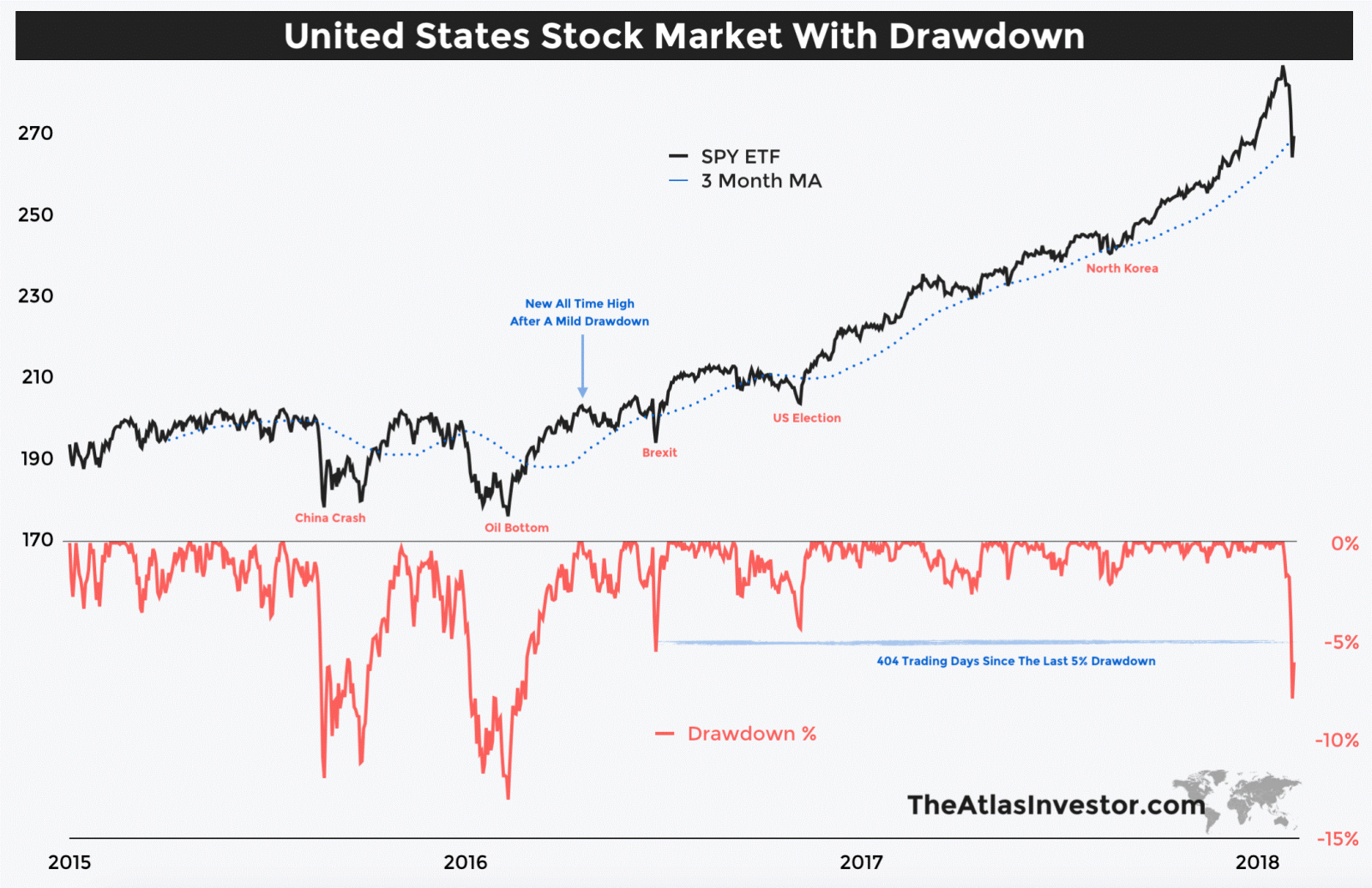

First, we know that US sharemarket volatility has been extremely low for a while. The red line on the chart below shows the percentage falls in US markets compared to the US SPY exchange traded fund, a proxy for the S&P 500.

Source: TheAtlasInvestor.com

Not since mid-2016 have we seen a fall in US stocks of more than 5 per cent. Look at the black line on the same chart from that point. We all (supposedly) know that stocks don't go up in a straight line, but since the election of Trump that's pretty much what they've done.

Now look at the (supposed) reasons for recent and substantial market falls – the crash in Chinese stocks in 2015 and a bottom in the oil price a few months later. Both saw the S&P 500 fall by more than 10 per cent.

The recent ‘correction' – a wonderful expression that implies the events preceding it were somehow a mistake – has been followed by a rebound, leaving the S&P 500 about 5 per cent below its all-time high on 26 January this year and the ASX 200 down 3.3 per cent since the yearly high on 9 January this year. It looks like a big fuss over nothing. So what's going on?

My guess is that herd psychology plays a part. We've all done well over the past few years and we don't like to see our portfolios retreat. Having made the gains, our brains lock them in. The shrinks call this loss aversion, and it plays a big role in market psychology. Falls make investors panic.

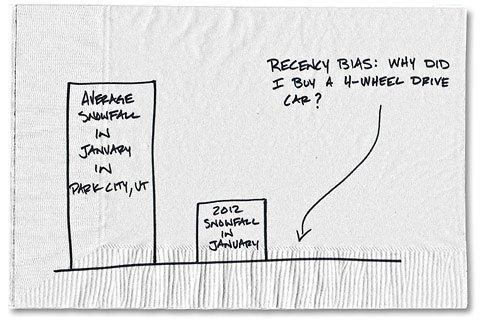

Recency bias amplifies the effect. Did low volatility cause investors to forget that substantial market falls are part and parcel of investing? Possibly. Having enjoyed over a year of big rises, punctuated by only minor falls, a big correction comes as a shock.

Source: Carl Richards

Second order recency bias is now in play. Instead of assuming low volatility, the correction is being extrapolated out into the future.

On Tuesday, I received an email from BetaShares with the subject line ‘Preparing for the next risk-off event'. It would have been more useful prior to the sell-off but no one would have read it. Now, when our brains are most alert to another fall, no one can stop talking about the next one.

The industry understands this flawed psychology perfectly and uses it to flog products. Take the Credit Suisse-sponsored – take a deep breath – VelocityShares Daily Inverse VIX Short-Term exchange-traded note – and relax (unless you bought it).

This product is a bet on calm market conditions, exercised through shorting volatility. Here's what the five year chart looks like:

Source: Bloomberg

Eek! When the US market plunged and volatility skyrocketed, the fund lost 92 per cent of its value, forcing Credit Suisse (Nassau branch, naturally) to close it.

Company CEO Tidjane Thiam, commenting on the collapse, said that, “It worked well for a long time until it didn't. Which is generally what happens in markets.” You're right there Tidjane. This was a momentum sell, alright. It wouldn't surprise me if a similar ETF product was soon released, with the word “inverse” removed. Oops, my bad. There are already 14 of them.

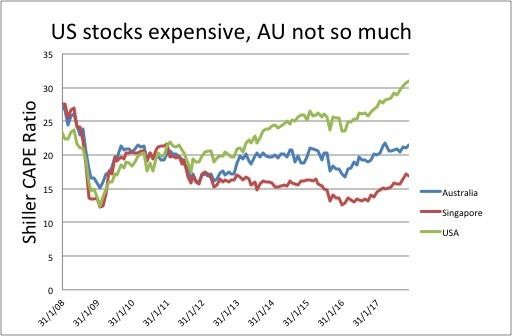

Whilst market psychology offers a way to rationalise an industry that pushes out products with in-built obsolescence, it doesn't entirely explain the pull back. Another fact gets in the way of doing so – US stocks are expensive.

On 23 January Robert Shiller published The world's priciest stock market. The timing was serendipitous, the title precise. I've featured this chart before but it's worth another look.

Data source: shiller.barclays.com

The CAPE ratio is the inflation-adjusted price of a share divided by a 10-year average of real earnings per share. It's useful for long-term investors because a lot can happen in a decade (see Fairfax, Kodak, John McGrath etc).

Shiller and Campbell studied US earnings growth back to 1881, reflecting the timeframes long-term investors should be thinking in. They found that there is “zero correlation between the CAPE ratio and the next 10 years' real earnings growth.” That's a worry for people paying 30 times earnings for US stocks right now.

But it gets worse. “Good news about earnings growth in the past decade is (slightly) bad news about earnings growth in the future”. This, as Shiller says, is “the opposite of momentum”. I suspect Tidjane Thiam gets this, and runs a business predicated on his clients not getting it.

Momentum is what the past few years have been all about. Earnings growth is increasing, but to assume it will continue to increase in perpetuity is dangerous.

Is this a concern for Australian investors? Not yet. Iron ore price rises have boosted the resources sector and some technology stocks have a whole lot of promise built into their prices. But, in general, our market has stood still while US stocks have boomed.

The ASX may well fall in line with US markets but that would only increase the value on offer, which isn't great right now but it's enough to keep us happy. Prices are a little over their long term averages, but not scarily so.

Which brings us to a lovely quote from Fifty Years in Wall Street by Henry Clews (via Andrew Macaulay at Veritas Equities), recounting how old hands deal with market tumbles:

“It is at these times that wealthy old veterans of the street emerge from the repose of their comfortable homes, & in times of panic, which recur sometimes oftener than once a year, these old fellows will be seen in Wall Street, hobbling down on their canes to their brokers' offices. Then they always buy good stocks to the extent of their bank balances. When the panic has spent its force, these old fellows, who have been resting judiciously on their oars in expectation of the inevitable event, which usually returns with the regularity of the seasons, quickly realize, deposit their profits with their bankers, or the overplus thereof, after purchasing more real estate that is on the upgrade & retire for another season to the quietude of their splendid homes and the bosoms of their happy families.”

Not sure about the happy families bit but I have no qualms with the rest. May you rest judiciously on your oars this weekend.