Can gold become a dividend diva?

- {{x.value}}

{{ twilioFailed ? 'SMS Code Failed to Send…' : 'Enter verification code' }}

{{ completedStep1 ? 'Authentication & Security' : content.trialHeading.replace('{0}', user.FirstName) }}

{{ content.upgradeHeading.replace('{0}', user.FirstName) }}

The email address you entered is registered with InvestSMART

Please login to continue

We have sent you an email with the details of your registration.

Looks you are already a member. Please enter your password to proceed

{{ upgradeCTAText }}

Updating information

Please wait ...

Your membership to InvestSMART Group recently failed to renew.

Please make sure your payment details are up to date to continue your membership.

Having trouble renewing?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

You've recently updated your payment details.

It may take a few minutes to update your subscription details, during this time you will not be able to view locked content.

If you are still having trouble viewing content after 10 minutes, try logging out of your account and logging back in.

Still having trouble viewing content?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

Please click on the ACTIVATE button to activate your Intelligent Investor 15-day free trial

Please click on the ACTIVATE button to finalise your membership

Unsuccessful registration

Registration for this event is available only to Eureka Report members. View our membership page for more information.

Registration for this event is available only to Intelligent Investor members. View our membership page for more information.

- You are already registered for this event.

- This event is already full.

- Please select a quantity for at least one ticket.

- {{ i }}

Forgotten password

Please enter your email address below to request a new password

- Indepth analysis of ASX listed shares

- BUY, Hold and Sell Recommendations

- Ideas Lab

- Special Reports

- Alan Kohler’s Weekend Briefing

- Interviews with CEO’s & top influencers

- Money Cafe and Talking Finance

- Super Advice and Q&A with Ask Alan

Summary: Gold's price is rising but investment banks say Australian miners are overpriced, while management dividend policies are generally in flux. |

Key take-out: Multiple moving parts make gold a slippery asset for investors who might see miners of the metal as prospective yield plays. |

Key beneficiaries: General investors. Category: Commodities. |

The metal itself is obviously not paying dividends. Goldminers are, and they look like becoming, more generous partly because most other forms of investment are becoming less generous.

Gold loves trouble, which is why its price is up 20 per cent this year with Australian miners getting a double-whammy benefit because their costs have fallen sharply as surplus labour and equipment flows out of the slowing coal and iron ore industries and into gold projects.

Ultra-low interest rates – including capital-destroying negative rates in an increasing number of countries – could ensure that the gold price stays high or rises further, as investors seek the ultimate safe haven which is immune from government interference in financial markets.

Fat profits being earned by goldmining companies thanks to its near-record price in Australian dollars are starting to find their way to investors in the form of higher dividends, with a lot more to come according to a survey of analyst research papers.

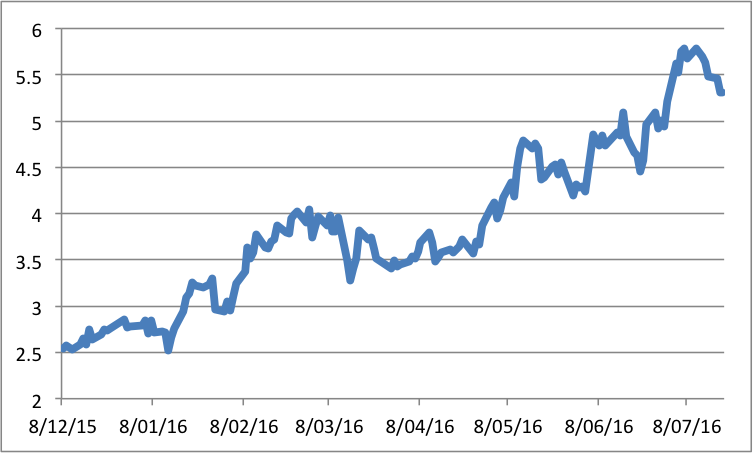

Northern Star Resources, for example, is expected to lift its dividend from 5c in the 2015 financial year to 8.45c in the year just ended, and then up to 18.35c, according to the investment bank Credit Suisse in a July 13 report.

Northern Star Resources share price, $, past 6 month:

Source: Bloomberg, Eureka Report

On the day of the Credit Suisse report Northern Star's share price was $5.70, putting it at an historic yield of 1.5 per cent, rising to 3.2 per cent if Credit Suisse's dividend tip is correct for the current financial year, and 3.8 per cent for next year – a yield which rises closer to 4 per cent since the company's share price has drifted back to $5.31.

Multiple moving parts make gold a slippery asset for investors who might see miners of the metal as prospective payers of generous future dividends.

The BHP Billiton experience, together with a savage 60 per cent dividend cut by Woodside Petroleum after the oil price crashed, should serve as warnings that all commodities are cyclical, including gold.

But if interest rates on government and corporate bonds stay low for longer, and political and economic shocks such as Britain's vote to quit the European Union continue to rock the financial world, then demand for gold could remain high, lifting the profits of goldmining companies.

Until now most of the credit for goldminers enjoying sharply higher share prices has been attributed to the gold price but there is increasing interest in four other factors. They are:

- Growing cash balances in the goldminers;

- A wide gap between high earnings per share and low current dividends per share;

- The appeal of exposure to gold in troubled times; and

- An expectation that Australian interest rates could fall further, trimming the value of the Australian dollar and boosting gold income on conversion from US dollars.

The cash factor was highlighted earlier today in the June quarter report of Northern Star which reported a 21 per cent increase in free cash flow to a record $224 million for the year to June 30, boosting cash on hand from $178m to $326m, with the company having the added bonus of no bank debt.

Northern Star, like most of the big gold miners, has been able to reduce its cost per ounce even as the price received has been rising. In the June quarter the average cost was $1041/oz which, at today's gold price of $1774/oz implies a profit per ounce of $733 (all Australian dollars).

Increasing levels of cash is evident in most goldmining companies. Newcrest, the biggest of the local miners, generating pre-tax earnings last year of $US1.38 billion from revenue of $US3.6bn, but with all of that being ploughed back into mining operations after several difficult years which saw dividends suspended.

In the year just ended, revenue and pre-tax earnings are expected to have been similar to last year but with an important addition expected in the full-year results scheduled for release on August 15 – the return to dividends with a forecast modest payout of 5c a share.

Welcome as any dividend will be, if that 5c payout is made it will be a fraction of the 44c in Newcrest's estimated earnings per share, which is hardly generous to shareholders.

In the current financial year the dividend per share is forecast to rise to 10c, an even more modest share of earnings per share which are expected to reach $1.29. Even in the following year a 40c dividend forecast by Credit Suisse will come from earnings per share of $1.37.

That tight-fisted dividend policy is likely to become an issue for Newcrest shareholders, especially those who want more cash back from their investments.

This picture of rising profits from a high gold price and lower costs has triggered a rush into goldmining stocks which has outpaced the valuations put on most goldminers by investment banks and stockbrokers.

In what looks to be a major disconnection between how professional analysts see goldminers and how private investors see the sector most gold stocks are trading at close to 20 per cent above investment bank valuations.

The consensus valuation of Newcrest by analysts from seven banks and brokerages is $16.69, a whopping 30 per cent below the stock's recent price of $24.06.

Other big goldminers, those with market value of more than $1bn, have similar valuation-to-price gaps. Evolution, according to the consensus view of six analysts is said to be 19 per cent overpriced ($2.28 versus market price of $2.81). Regis Resources is said to be 23.5 per cent overpriced ($2.88 v $3.76). Saracen is said to be 19 per cent overpriced ($1.40 v $1.70). St Barbara is said to be 19 per cent overpriced ($2.78 v $3.44), and OceanaGold is said to be 20.5 per cent overpriced ($3.85 v $4.84).

There are as many messages in those price versus valuation numbers as there are in the arguments for and against gold.

It could be that investors have rushed too enthusiastically into goldmining stocks, or it could be that the models used by analysts are failing to keep up with the high gold price, falling costs, currency movements, rising gold company profits and the widespread concern about low yields on conventional investments.

The issue which I find particularly interesting is the gap between forecast goldmining company earnings per share and forecast dividends per share.

Newcrest's expected 40c payout next year from earnings per share of $1.37 is matched by Evolution's forecast earnings of 23.7c a share and a dividend of 6c. Northern Star has earnings of 61c and a dividend of 18.35c.

There can be good reasons for companies retaining earnings, and that's certainly the case in an industry with a depleting asset base such as goldmining, which is always challenged by a depleting asset base and what can be a highly fluid price for gold.

But if some investors are buying shares in goldminers in the expectation of a rising yield (at a time when everything else seems to be falling) then the seeds are being sown for a showdown between management – which wants to retain earnings – and shareholders who want yield.

Game on!