Bright prospects for the UK despite Europe's gloom

- {{x.value}}

{{ twilioFailed ? 'SMS Code Failed to Send…' : 'Enter verification code' }}

{{ completedStep1 ? 'Authentication & Security' : content.trialHeading.replace('{0}', user.FirstName) }}

{{ content.upgradeHeading.replace('{0}', user.FirstName) }}

The email address you entered is registered with InvestSMART

Please login to continue

We have sent you an email with the details of your registration.

Looks you are already a member. Please enter your password to proceed

{{ upgradeCTAText }}

Updating information

Please wait ...

Your membership to InvestSMART Group recently failed to renew.

Please make sure your payment details are up to date to continue your membership.

Having trouble renewing?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

You've recently updated your payment details.

It may take a few minutes to update your subscription details, during this time you will not be able to view locked content.

If you are still having trouble viewing content after 10 minutes, try logging out of your account and logging back in.

Still having trouble viewing content?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

Please click on the ACTIVATE button to activate your Intelligent Investor 15-day free trial

Please click on the ACTIVATE button to finalise your membership

Unsuccessful registration

Registration for this event is available only to Eureka Report members. View our membership page for more information.

Registration for this event is available only to Intelligent Investor members. View our membership page for more information.

- You are already registered for this event.

- This event is already full.

- Please select a quantity for at least one ticket.

- {{ i }}

Forgotten password

Please enter your email address below to request a new password

- Verify your email address by clicking on the link we sent to {{user.Email}}

- You now have free access, we look forward to helping you on your financial journey.

The economic outlook for the UK has eased a little since August but otherwise remains quite bright. However, with inflation moderating -- and potentially dropping below a 1 per cent annual pace in the months ahead -- the Bank of England has poured cold water on any thoughts of a rate rise in the near future.

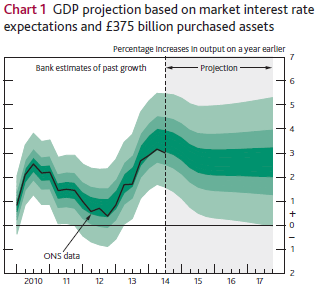

In its quarterly inflation report, the BoE sees the UK growing at a pace of 3.5 per cent in 2014 before easing to 2.9 per cent next year and 2.6 per cent in the following two years. These are solid numbers, even in the latter years, and indicate that policy normalisation remains on the agenda.

The fan chart below indicates that there is a 30 per cent chance that real GDP will fall within the darkest green area and a 90 per cent chance that GDP growth will fall within the widest of the three confidence intervals.

But recent developments have pushed out interest rate expectations. As recently as June, BoE governor Mark Carney had warned markets of the potential for an early rate rise. In August, I suggested that the bank may look to make a move before the end of the year -- I was off the mark.

Nevertheless, the UK economy continues to show signs of improvement and has thus far proven resilient to the latest round of economic dysfunction in Europe.

“A spectre is now haunting Europe,” Carney said.

“The spectre of economic stagnation, with growth disappointing again and confidence falling back.”

I don't think anyone would argue about that, which makes the UK's resilience all the more impressive.

Carney sees three factors which explain why the UK can continue to grow at an above-trend pace despite subdued demand in Europe and increasingly the global economy.

Firstly, the labour market continues to improve. The UK economy has created 700,000 new jobs over the past year and real wages have recently ticked up for the first time in five years.

Labour market developments have been supported by a sharp decline in oil prices and food prices. A stronger sterling has increased the purchasing power of UK household incomes and combined with the recent pick-up in wages could signal an improved period for the household sector.

Secondly, consumer confidence has proved to be quite resilient in the face of European weakness and a “larger-than-expected slowing in the housing market”. So far, higher employment and improving wage conditions are more than offsetting these other factors and that's a good sign moving forward.

Thirdly, investment activity remains elevated and is likely to remain that way over the forecast horizon. Investment is paramount for productivity growth -- an ongoing problem within the UK -- and if it can turn that around, it really can set itself up for a few strong years.

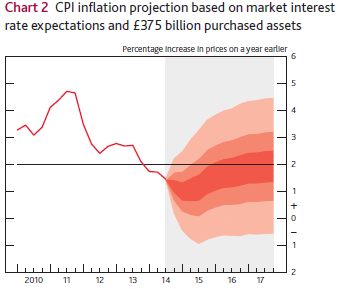

Nevertheless, there is little pressure on the BoE to act, with some of the factors supporting the economic recovery also putting downward pressure on inflation and inflation expectations.

Chief among them is the sharp fall in oil and food prices and the appreciation of the sterling. Weaker inflation among its major trading partners also hasn't helped. Carney considers it more likely than not that annual inflation will drop below 1 per cent over the next six months (currently at 1.2 per cent).

But with the economic outlook reasonably strong, inflation should return gradually towards the banks' 2 per cent target. The factors driving inflation towards 1 per cent are largely temporary and that should ease or potentially reverse in the years ahead.

“We do not expect a rapid return of inflation to the target,” Carney said. “Although they are not permanent, the forces subduing inflation today are likely to persist for some time. In today's projections, inflation returns to 2 per cent only by the very end of the forecasting period.”

But, given the nature of those factors, there must be significant uncertainty surrounding the inflation outlook. Foreign exchange markets and oil prices are unpredictable at the best of times and interest rate normalisation should be viewed within that context. The first rate hike will be data dependent and could occur much earlier or later than the bank currently expects.

Despite the outlook for the UK economy suffering a modest downgrade, the recovery remains on track. Naturally, the economy faces some significant challenges -- wage and productivity growth remain two important ones -- but has so far proved to be fairly resilient and that bodes well for the years ahead.

Given the combination of elevated growth and low inflation, the BoE can take it easy over the next six months and reposition itself for a rate hike later next year. But the shift in the banks' communications over the past six months highlights that interest rates remain data dependent and could shift quite suddenly.